senior fellow - energy & climate policy - @bruegel_org

Scientific Lead - GreenDealUkraїna - @HZBde

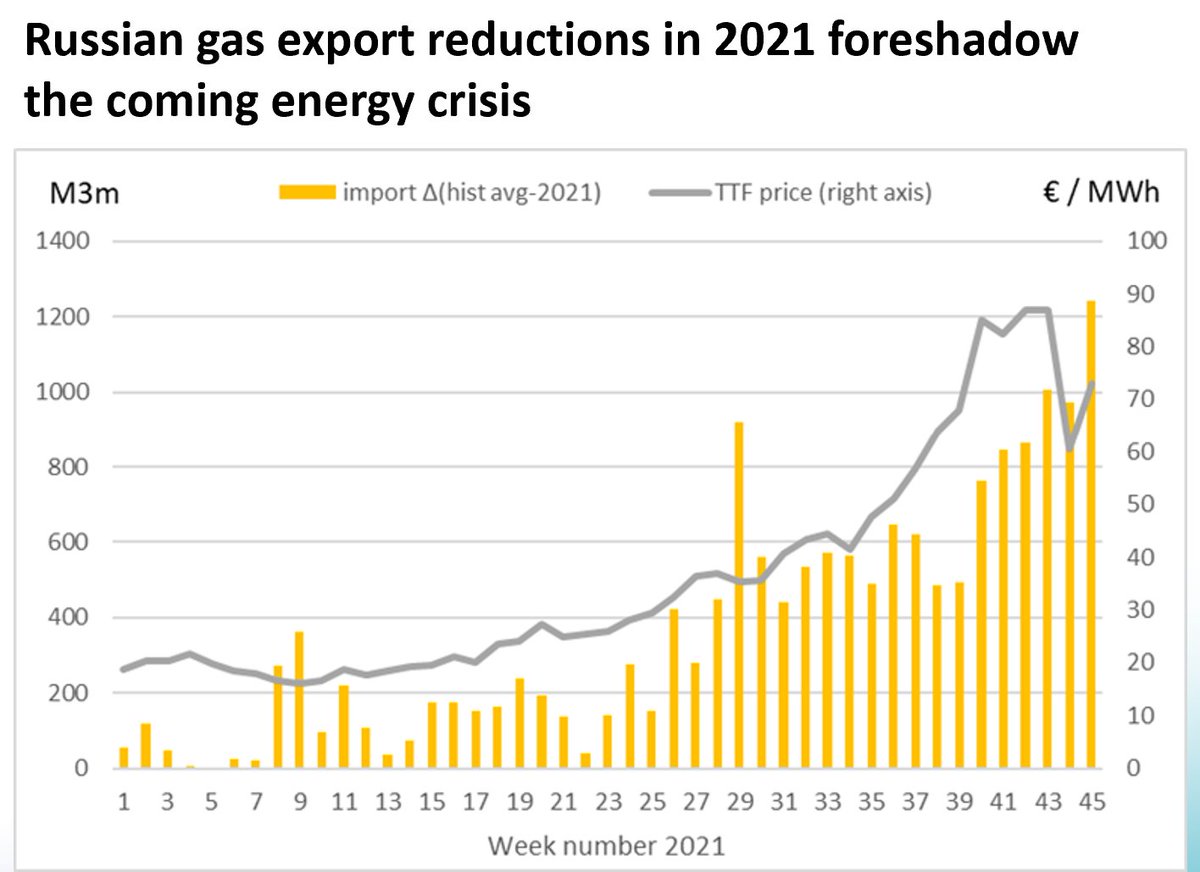

PRELUDE - SUMMER 2021

PRELUDE - SUMMER 2021

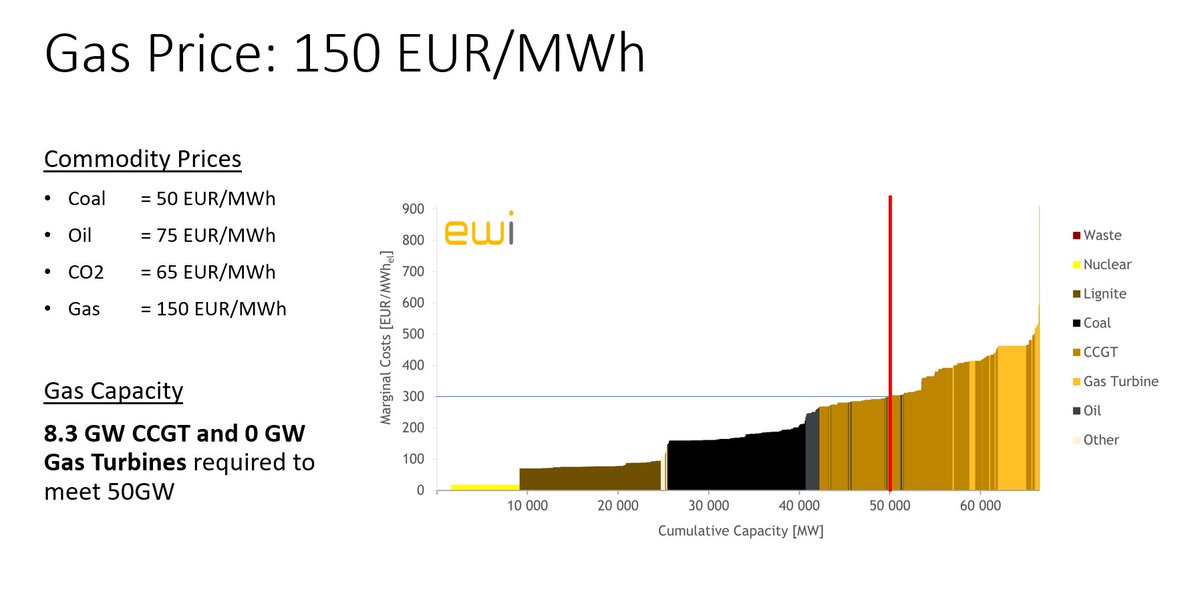

We use @ewi_koeln's cool merit order tool, adjust the fuel cost assumptions to be roughly in line with current numbers and assume a situation with a residual demand of 50 GW.

We use @ewi_koeln's cool merit order tool, adjust the fuel cost assumptions to be roughly in line with current numbers and assume a situation with a residual demand of 50 GW.

only diversification will not be enough

only diversification will not be enough

Gazprom already reneged on most EU countries' gas supply contracts partially or fully.

Gazprom already reneged on most EU countries' gas supply contracts partially or fully.

1. Focus : 2022/23

1. Focus : 2022/23

2/4 The weaknesses I

2/4 The weaknesses I

Drop in electricity consumption (that is observable in real-time) correlates rather strongly with drop in industrial production (that is observable ~2 month later).

Drop in electricity consumption (that is observable in real-time) correlates rather strongly with drop in industrial production (that is observable ~2 month later).