Rarely in doubt, Frequently wrong. Stock & REIT ideas. #FinTwit DJ. Mainly followed by TwitterX ladybots

2 subscribers

Mar 16, 2023 • 9 tweets • 3 min read

1/n Higher/rising rates $TLT & 2023/24 unit deliveries have weighed on #multifamily#REITs $AVB $CPT $EQR $ESS $MAA $UDR over the past year. I see the credit events $SIVB $FRC $SBNY $KBE of the past week being a positive for the sector as:

2/n Small/Med banks are a key lender to developers. Last week (prior to bank crisis), at Citi conf $MAA CEO said that new MF permitting had come to a halt due to rising rates/spreads/const costs. Bank crisis will further curtail development. LOWER SUPPLY

What's the opposite of $SIVB $BAC $WFC $FRC large MTM losses on HTM securities? Long-term, low fixed rate debt $ARE #REITs

Mar 10, 2023 • 5 tweets • 2 min read

Ugly week for #REITs. Bought the CA heavy stuff hard today:

$KRC -10.7% overall cap. Office is 13+% stripping out MF/LifeSci @ 6.

$ARE -6.5%

$ESS -5.9%; 370k/door

$EQR -6.1%; $372k/d

I $SIVB $FRC $SBNY $PACW doesn't sink the SF Bay/CA economy

non CA:

$MAA -5.9%; $218k/d

I'm implicitly betting the the troubled banks don't F up the golden goose of the SF Bay /LA VC ecosystem. Yes many wannabe unicorns had deposits there but I believe recoveries will be 80%+ of funds. Might lead to some incremental job losses but not the end of the world

Aug 8, 2021 • 6 tweets • 3 min read

1/n So I posted this in reply to another thread but wanted to see if I can find more pushback. Clearly people have been disappointed with $ATUS 1Q net adds, particularly versus $CHTR and $CMCSA. However, I think there is plenty of evidence which... @FrancoOlivera@AndrewRangeley2/ A) 1-3Q20: People flee NYC in droves, many end up (temporarily) in $ATUS footprint and register as net adds in 2020. Slide below is from a Nov2020 presentation by $UDR, an apartment REIT with exposure to NYC area:

Mar 8, 2021 • 9 tweets • 3 min read

$KRC CEO John Kilroy says he believes the stock is trading at a 1/3 discount to NAV on $C Citi Property CEO conference. Kilroy Oyster Point Ph 2 (Life sciences $ARE) to start this summer. Will also start development of new life sciences project in San Diego. KRC has plenty of $

for development. May also repurchase shares/pay special dividend. #reits#dividends#dividendstocks Great track record of value creation via development - should trade at a premium to NAV. I think this is worth $100-120 per share.

Mar 7, 2021 • 5 tweets • 3 min read

The RATE-ARDs at $MCO Moody's and S&P $SPGI have too much influence over companies - case in point is $INVH which owns 80k single family homes with a loan-to-value (LTV) of just 32%. Somehow this company is NOT 'investment grade' and they are de-levering...

2/ to appease these idiot rating agencies. Consider that people typically put down only 5-10% of the purchase price of a home (the rest is financed with a mortgage at an LTV of 80%+). Of course there is one recent example of a situation where the US housing market blew up -caused

Mar 5, 2021 • 11 tweets • 4 min read

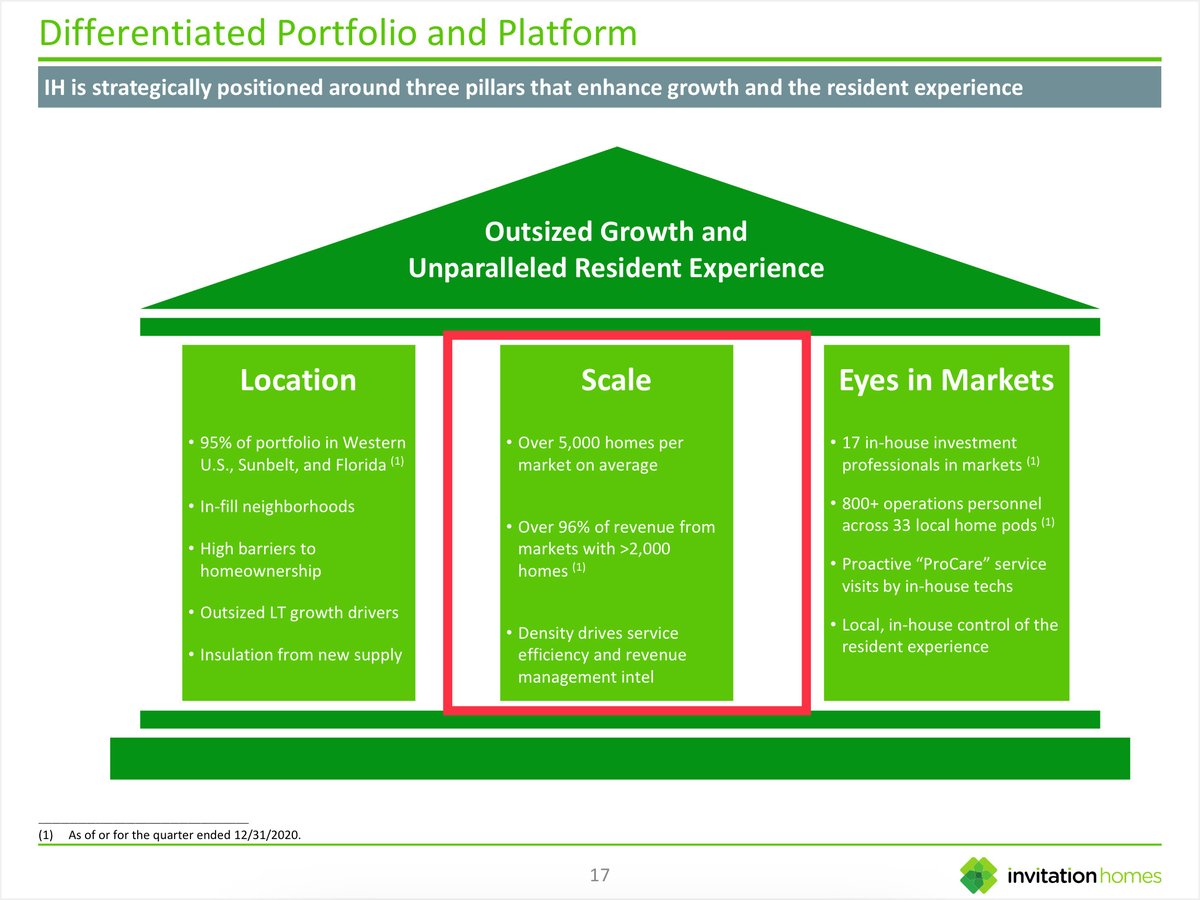

Inflation $TLT worries=opportunity to invest in single family rental leader Invitation Homes $INVH. At $28/sh implies 4.8% 2021 cap rate. Trades at ~5-10% discount to NAV.

$AVB $EQR $CPT $MAA $ESS $VNQ $AMH $XLRE #reits#dividends

SHOULD trade at premium to NAV->Platform value:

2/While anyone can buy a home and become a landlord, this is a scale/density business. To effectively manage single family homes bigger is MUCH better. Scale allows for in-house provision of services (hire a plumber full time for $200/day rather than pay $150 for each visit).

Feb 9, 2021 • 4 tweets • 2 min read

$CPT -Private market sells us that NAV here is ~$125. Good mgmt track record; should trade at a premium. Baird & $BAC putting out usual sellside nonsense today (how is it worth 10% less than yesterday $BAC?). $BAC thinks it knows better than $billions in private mkt skin in game

participants. Haha. Notes from call: There is a strong bid for Class B value add (apartment classes explained here) apartments in the private market. The cap rate spread between Class B 'value add' apartments and Class A apartments has narrowed considerably over the last couple

Feb 5, 2021 • 5 tweets • 2 min read

$ESS Love the way they describe capital market activities on the call - I'm paraphrasing "Selling properties at pre COVID pricing and buying back stock at a significant discount to NAV". While volumes have declined in the private market mgmt believes suburban properties would

fetch pre-COVID pricing or better (vast majority of ESS is suburban) whereas urban property values are estimated to be -5% vs. preCOVID w/ cap rates of 4% or lower. Mike Schall & co are the best in the biz $UDR $EQR $AVB $VNQ

Feb 5, 2021 • 5 tweets • 3 min read

$MAA (2/4) call highlights: 1)demand is strong -now getting ‘normal’ 5-6% renewal rates (2)see supply moderating in 2H (I always take this with a grain of salt in the sunbelt!) #reits $CPT $VNQ $NXRT #multihousing#apartmentinvesting#dividends#cre (3)Valuations are high/cap....

3)Cap rates at all time lows in key markets (mid 3s/low 4s). This makes it impossible for MAA to acquire assets accretively. Instead they will do some opportunistic divestitures and (4)develop new apartment buildings (2,600 underway)- development yields are expected to be around