Tech/Autos analyst at Global Energy Transition L/S fund; Ex-HSBC analyst; IIT-B+ Nanyang MBA; In the long term, we're all dead!

Magna (MGA) is the closest peer to Motherson Sumi - offers the same products to same customers. No wonder their margins track each other.

Magna (MGA) is the closest peer to Motherson Sumi - offers the same products to same customers. No wonder their margins track each other.

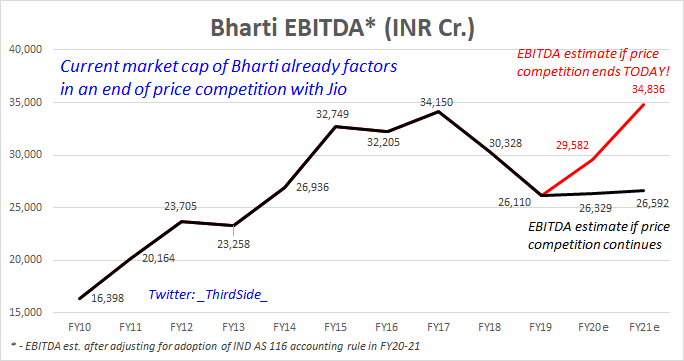

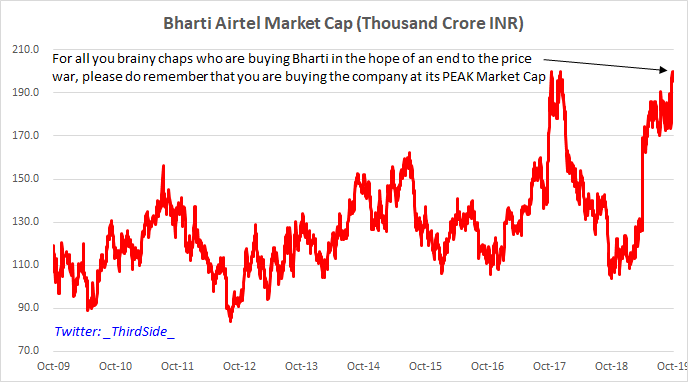

Oh! did I mention that the current PEAK market cap of Bharti Airtel already factors in an end of price competition with Jio (as if it ended today) BUT has the competition ended? And, what's the Jio management repeatedly saying? #Nifty #BigShort?

Oh! did I mention that the current PEAK market cap of Bharti Airtel already factors in an end of price competition with Jio (as if it ended today) BUT has the competition ended? And, what's the Jio management repeatedly saying? #Nifty #BigShort?