MD Global Macro @TS_Lombard, macro themes/research/risks, central-bank specialist, started career at HM Treasury in late 90s, ex ABN AMRO, AC Milan fan

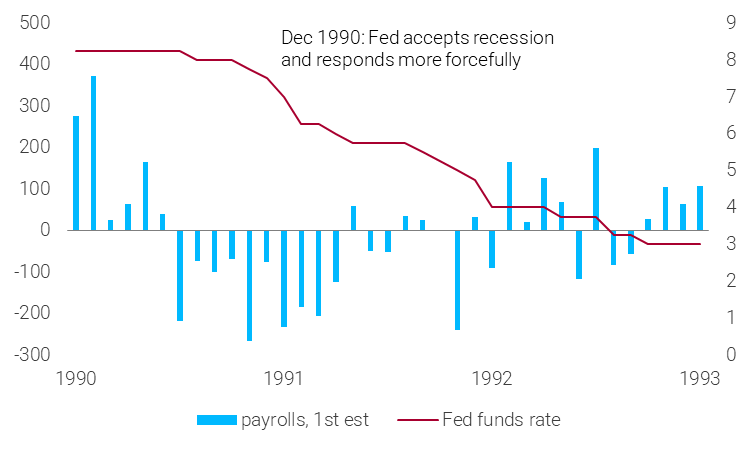

2) The Fed’s inaction continued in the following months. By October, most officials still believed they were in a soft patch rather than a recession. Energy prices had squeezed consumers' real incomes, but the staff thought this would be a 1-2 quarter problem – then growth would promptly rebound. By November, the mood was turning more negative. In December, Greenspan finally realizes the economy is in recession – because the deterioration in the data had gone non-linear . (That’s 5 months after the NBER start date.)

2) The Fed’s inaction continued in the following months. By October, most officials still believed they were in a soft patch rather than a recession. Energy prices had squeezed consumers' real incomes, but the staff thought this would be a 1-2 quarter problem – then growth would promptly rebound. By November, the mood was turning more negative. In December, Greenspan finally realizes the economy is in recession – because the deterioration in the data had gone non-linear . (That’s 5 months after the NBER start date.)

1) PROTECTION MONEY

1) PROTECTION MONEY

Rule 2 of central banking: Sometimes and selectively a monetary phenomenon

Rule 2 of central banking: Sometimes and selectively a monetary phenomenon

2)

2)

2) This is usual. Investors cant remember the last time CBs made f'casts like this. CBs used to be cheerleaders, who always talked up their economies (H/T ECB 😉). Is this a sign of just how inevitable recession has become? Or is it policy INTENT - maybe officials WANT recession

2) This is usual. Investors cant remember the last time CBs made f'casts like this. CBs used to be cheerleaders, who always talked up their economies (H/T ECB 😉). Is this a sign of just how inevitable recession has become? Or is it policy INTENT - maybe officials WANT recession

yikes

yikes