Sorry to repeat this, but since @DavidLammy has waded in, I thought it was worth an update to the “Brexit was about tax avoidance!” conspiracy theory. You know, “The referendum date was announced just after the EU announced the Anti Tax Avoidance Directive.” And…

“…article 50 was invoked so that the UK would avoid the implementation of the Anti Tax Avoidance Directive in April 2019! You Brexiteers have all been conned!” Well, let’s leave aside the fact that the effective date was January 1st 2019 and see who’s being conned by…

…who. Here’s a timeline. The issue of “base erosion” (eroding your tax base) was first discussed at the OECD summit in Mexico in June 2012, and again at the G20 Finance Minister summit in November of the same year. At this summit the UK and Germany agreed to combat Base…

…Erosion and corporate tax avoidance, issuing a joint statement. Later, France also agreed to push for action. The EU, not surprisingly since its 3 dominant economies had all already become involved, made its own statement in December 2012, after the UK. Clearly, a policy..

…which was initiated by the UK and Germany, was not the reason behind the UK wanting to hold a referendum. The UK happened to be President of the G8 in 2013 and so included cross-border tax on the agenda for the May 2013 G8 meeting. Immediately following that…

…meeting the OECD BEPS (Base Erosion and Profit Shifting) Project was launched at the G20 in July 2013. Since the UK was pretty instrumental in starting the BEPS project, it is clearly not something we’re going to jump through hoops to avoid happening, and indeed, as…

…an OECD member in our own right and a leading advocate of BEPS, the UK is literally years ahead of the EU in implementing BEPS. “Ah”, say the conspiracy theorists having not seen the ATAD, “the EU rules didn't come in until 2019 so the UK didn't have these rules…

…and anyway they go much further”. Do they? Well, let’s have a look – here’s the Directive.

eur-lex.europa.eu/legal-content/…

eur-lex.europa.eu/legal-content/…

It’s worth nothing from the outset why the EU implemented this directive – it is quite clear from the ATAD preamble that it is implementing BEPS across the EU – you know the thing the UK helped kick off?

Anyway, whizz down, ignore all of Chapter 1, the measures themselves start with Ch II, Article 4 – Interest Limitation rule. This was in UK legislation already TIOPA 2010, Part 10, but was amended in 2017 and is now the “Corporate Interest Restriction”. Having debts means…

…you have interest deductions which you can then use against your tax liability so very basically these rules limit the deductions to 30% of your profits - or “EBITDA” if you want to be technical. It’s not illegal to have more than 30%, but it’s just beyond this level the...

…deductions are disallowed. Next is Article 5, “Exit taxation”. This is in UK law in TCGA 1992 s185-187. This is to do with ensuring companies don’t just move assets outside the UK taking a chargeable gain with them – so you pay an Exit Charge. Now, there was an inconsistency…

…here. In separate UK legislation, TMA 1970 Sch3ZB, there is a deferral period of 10 years, whereas in ATAD Art 5(2) it specifically states it should be 5 years. Since the UK has already implemented these measures, it won’t be surprising that some EU rules are different, and…

…where they go beyond UK rules the UK would need to amend the rules to be fully compliant with the ATAD. So, an amendment in the Finance Act 2019 includes a change to the deferral period – HMRC states the impact is “negligible” (which means under £5million).

Still awake? Don’t care…moving on. Article 6 is the General Anti Abuse Rule (GAAR). A GAAR means if an authority finds a scheme is designed to avoid tax, but is not contained in a specific or “targeted” rule, it can nevertheless seek to disallow the deduction under the GAAR.

The GAAR, in the Finance Act 2013 s206, was announced by George Osborne in the 2012 budget, before the EU announced anything. The GAAR isn’t in my view something that we should seek to use very often, since it would indicate our targeted rules were rubbish. It’s just a backstop.

ATAD Articles 7 and 8 are about CFC rules – “Controlled Foreign Companies”. We’ve had CFC rules in the UK since 1984, and can be found in TIOPA 2010 Part 9A. They are pretty complex, with a number of different gateways your income flows through and if it doesn’t meet one of the…

…exemptions it will suffer a CFC charge. “What?” I know. Essentially, the idea is if a UK company controls a foreign company, then the profits of that foreign company can flow through a gateway and be charged to the UK company, provided it doesn’t meet an exemption. “Ah, you…

…mean a loophole!.” Not really, the idea is that these rules are only ever used to be used where the arrangement is being used to avoid tax. So a French subsidiary of a UK company would have an entity level exemption since the company is unlikely to be artificially shifting…

… profits to its French subsidiary so it can suffer 33.33% corporation tax! Again, there were a couple of amendments necessary to UK legislation in the Finance Bill 2019, to do with the definition of control including non-UK associated enterprises, but again HMRC determined…

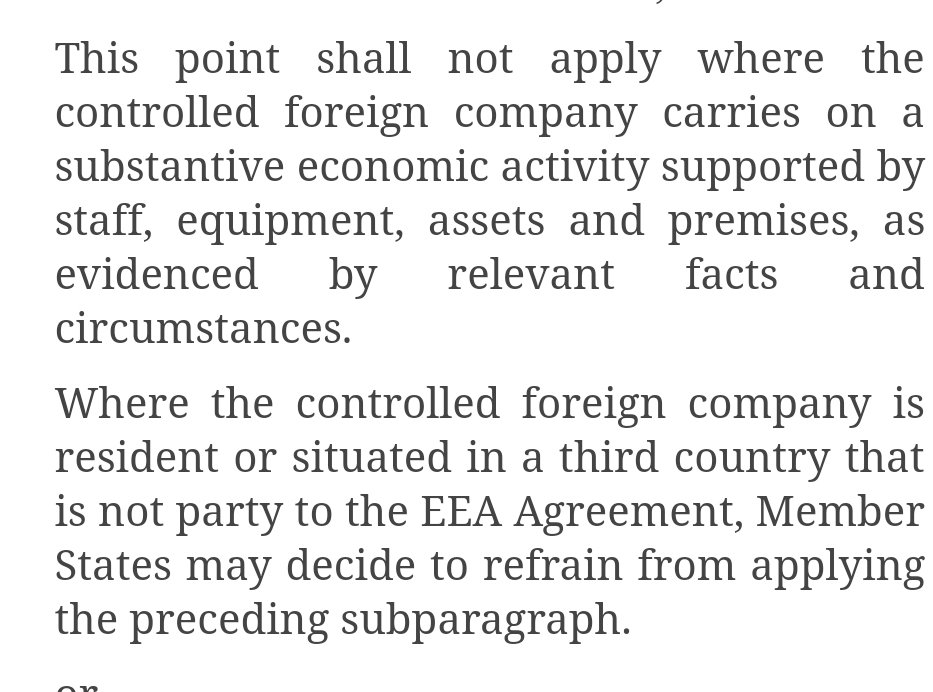

…the impact to the exchequer to be “negligible”. CFC rules are a great example of membership of the EU being detrimental to our tax avoidance rules. If you still have the Directive open, find Article 7, para 2. The godsend for tax avoiding companies everywhere is…

…this statement, “This point shall not apply where the controlled foreign company carries on a substantive economic activity supported by staff, equipment, assets and premises, as evidenced by relevant facts and circumstances.” What does that mean? Well, as long as you have…

…staff sat indoors at computers in your Luxembourg subsidiary it does not matter that the purpose of that subsidiary is to avoid UK tax, the CFC rules shall not apply. So, I want to book some very lucrative, profitable, taxable, contracts then that business can be directed…

…to my Luxembourg/Irish subsidiary. RT if you’re still awake! You’re doing very well if you’ve got this far. Lastly, we have the Hybrid Mismatch rules, which are in UK law TIOPA 2010 Part 6A, and appear briefly in Article 9 of 2016/1164 EU, but substantively these…

…are in “ATAD II” 2017/952 EU. These are to prevent the use entity classification arbitrage between jurisdictions. Some people may have heard of a “Double Irish with a Dutch sandwich” where you basically use a combination of domestic rules and treaty rules…

…to create “stateless income” which doesn’t get taxed anywhere. These rules are designed to ensure that if an entity isn’t taxed in one jurisdiction, it will be taxed in the other regardless of whether it is considered opaque/transparent etc. Again, the UK…

…is going to amend the rules we have had since 2016 to accommodate the EU variances, and again this is allowed for in the Finance Bill 2019 and again HMRC have deemed the impact negligible. If you’re interested the minor amendments can be found in the Finance…

..Act 2019 attached. This should take you to ‘international matters’, the amendments are in sections 19-23, and further in sch. 7 and 8.

legislation.gov.uk/ukpga/2019/1/p…

legislation.gov.uk/ukpga/2019/1/p…

There will still be some die-hard conspiracy theorists who will state, “OK, but I bet they’ll get rid of these rules as soon as we leave”. Well, as I say, this is an OECD initiative, so as an OECD member in our own right we would have implemented any measures we didn’t…

…have anyway. Annex 4 of the Withdrawal Agreement contains a specific commitment to continue to implement these rules beyond transition. “Ah, what about no deal. This is what is intended, then we could just repeal the legislation?” Sure, the UK could repeal all…

…our tax legislation, leave the OECD, JITSIC and the rest of our international commitments and become an international pariah. Is that what is intended? If it is the intention then surely the Government would’ve repealed our current legislation and transposed the ATAD…

…in full as an EU directive, bringing it into scope of the Henry VIII clause in the EU Withdrawal Act? If it is the intention why did the Government introduce, without EU prompt, the Profit Diversion Compliance Facility in January?

gov.uk/government/pub…

gov.uk/government/pub…

Bit of a waste of effort? If the Government is intending on repealing tax avoidance legislation, why is it bringing in new Profit Fragmentation laws from April this year? This one piece of legislation will, by some distance, raise more tax than all the amendments we had to make…

…to comply with ATAD combined! In truth, the UK has some of the most advanced anti-tax avoidance legislation in the World. We are thought-leaders in the field, and it comes as no surprise that the rules the OECD, and the EU, have introduced are closely aligned with much…

…of what we already do anyway. In summary, was Brexit about avoiding the Anti-Tax Avoidance Directive? No it wasn’t – it’s just a conspiracy theory. The rules were already UK law in every material sense, and the ATAD is not primarily an EU initiative…

…but an OECD driven Project which the UK itself was instrumental in launching. Brexit had nothing whatsoever to do with avoiding the Anti Tax Avoidance Directive and any conspiracy theorists who repeat such nonsense should be forced to sit and read this…

…thread repeatedly until they learn a more sensible argument. Google anything I have just said and if you find anything to doubt the veracity of this thread I would be very interested. Congratulations to anyone who got this far (again).

• • •

Missing some Tweet in this thread? You can try to

force a refresh