We learned last week that core #goods #prices continue to remain weak, and indeed over the longer run they’ve witnessed #disinflation.

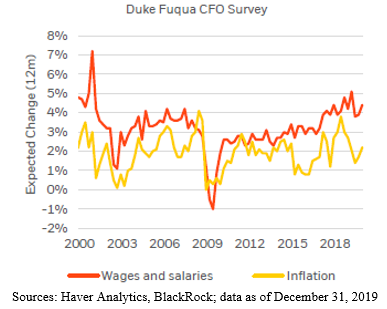

Meanwhile, while #inflation could see some support alongside a pickup in #wage growth, we think this linkage is much weaker than many suggest: higher wages don’t create meaningfully higher inflation in this era, and corporate #CFOs are beginning to recognize it.

Indeed, we think #inflation is more likely to be driven a bit higher by the weaker #USD, and perhaps a higher monetary base (potential velocity gains) and not so much from #wage increases.

• • •

Missing some Tweet in this thread? You can try to

force a refresh