1/ Strategic and Tactical Roles of Enhanced-Commodity Indices (Rallis, Miffre, Fuertes)

* Enhanced long-only commodity indices based on contract maturity, momentum, and carry

* Longer-maturity contracts have higher returns with less volatility

papers.ssrn.com/sol3/papers.cf…

* Enhanced long-only commodity indices based on contract maturity, momentum, and carry

* Longer-maturity contracts have higher returns with less volatility

papers.ssrn.com/sol3/papers.cf…

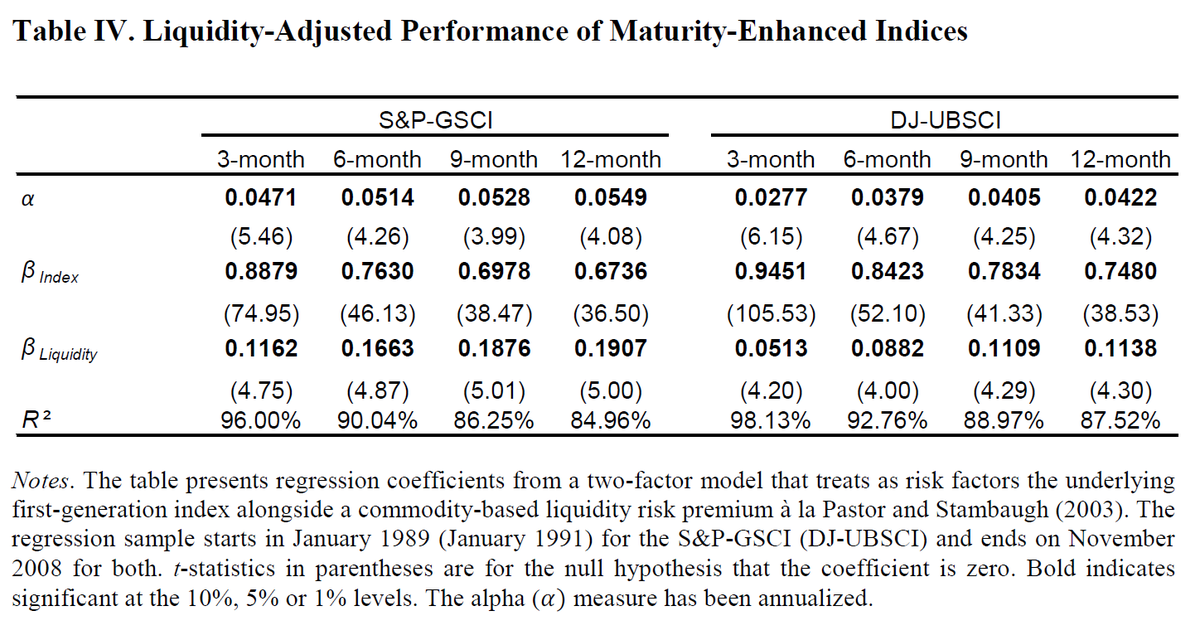

2/ Enhanced-maturity indices roll into specific contracts in the term structure to provide average maturities of 3, 6, 9, or 12 months.

Each commodity's weight in the enhanced index is identical to its weight in the (long-only) traditional index.

Each commodity's weight in the enhanced index is identical to its weight in the (long-only) traditional index.

3/ As contract maturities increase, returns increase and volatilities decrease. Skewness and kurtosis get worse.

The authors don't control for carry, which could conceivably be responsible.

Negative commodity skewness is from the 2008 crash (skewness is positive otherwise).

The authors don't control for carry, which could conceivably be responsible.

Negative commodity skewness is from the 2008 crash (skewness is positive otherwise).

4/ Liquidity (as measured by average open interest) decreases as we move from the front month to the far end of the term structure.

Statistically significant alphas remain after controlling for contract illiquidity; the alphas rise monotonically with maturity.

Statistically significant alphas remain after controlling for contract illiquidity; the alphas rise monotonically with maturity.

5/ The authors build long-only factor indices by starting with the modifying the original index weights based on factor ranks.

Carry is calculated between the two nearest contracts.

These strategies buy *front*-month contracts. (The methodology is on pp. 13-19 of the paper.)

Carry is calculated between the two nearest contracts.

These strategies buy *front*-month contracts. (The methodology is on pp. 13-19 of the paper.)

6/ The momentum- and carry-enhanced indices may have moderately higher turnover (though transaction costs are not explicitly accounted for).

Long-only indices, including maturity-enhanced and trend/carry-enhanced versions, don't perform as well as L/S portfolios in other papers.

Long-only indices, including maturity-enhanced and trend/carry-enhanced versions, don't perform as well as L/S portfolios in other papers.

7/ "The outperformance of the enhanced indices does not come at the expense of inferior risk diversification.

"The enhanced indices are as good a hedge against inflation as the first-generation indices are."

(The authors don't study carry+momentum in longer-maturity contracts.)

"The enhanced indices are as good a hedge against inflation as the first-generation indices are."

(The authors don't study carry+momentum in longer-maturity contracts.)

8/ Skewness gets worse with increasing contract maturity, so here are the skewness-adjusted Sharpes (Wayne Himelsein's Skill Metric):

GSCI index: 0.173 Sharpe → 0.08 Skill Metric

3-month: 0.4531 → 0.29

6-month: 0.5172 → 0.31

9-month: 0.5508 → 0.32

12-month: 0.5753 → 0.34

GSCI index: 0.173 Sharpe → 0.08 Skill Metric

3-month: 0.4531 → 0.29

6-month: 0.5172 → 0.31

9-month: 0.5508 → 0.32

12-month: 0.5753 → 0.34

9/ De Groot, Karstanje, and Zhou examine momentum strategies that take advantage of varying roll yields and lagged returns along the futures curve (1 to 12 months).

They control for cross-sectional momentum and carry and also include transaction costs:

They control for cross-sectional momentum and carry and also include transaction costs: