Here’s a new thread on the dollar, swap lines, and the treasury market. With lots of charts.🧐

AKA “Why the global dollar shortage is not insurmountable.”

AKA “Why the global dollar shortage is not insurmountable.”

There is $250+ trillion of debt in the world.

Of this, over $50T is USD debt by American households, nonfinancial corporations, and the govt.

Much of the rest is debts for other countries in other currencies.

Of this, over $50T is USD debt by American households, nonfinancial corporations, and the govt.

Much of the rest is debts for other countries in other currencies.

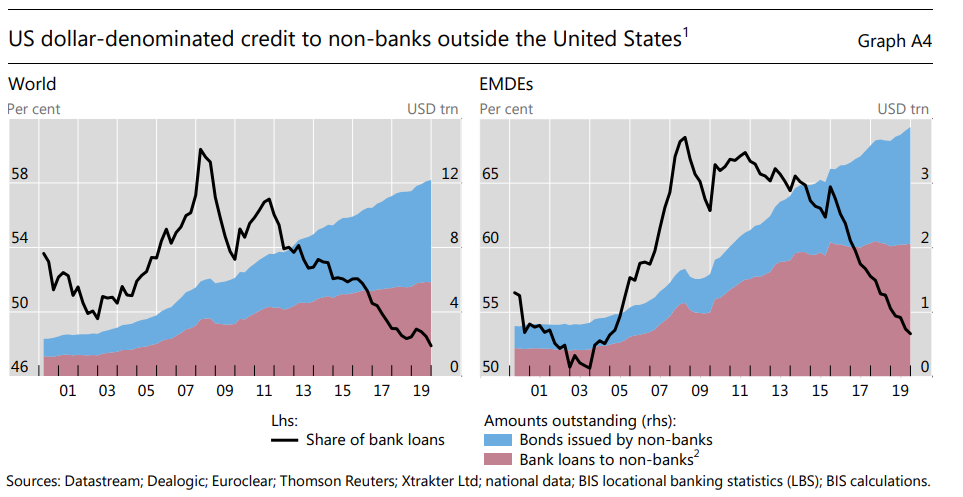

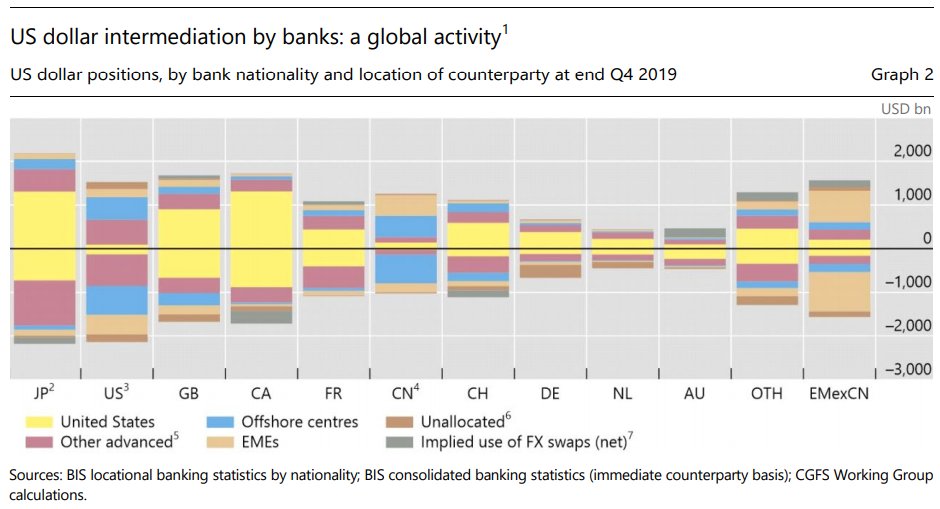

However, governments and nonfinancial corporations outside of the U.S. also hold $12+ trillion in USD-denominated debt, since it’s the most-used global currency.

And they rely on USD-based global trade to get dollars to service those debts.

And they rely on USD-based global trade to get dollars to service those debts.

Many people are rightly concerned about offshore USD debt, because govts and corporations that have USD-denominated debt but exist outside of the US have less access to the Fed as a funding backstop.

About $8T of that $12T is in advanced nations, and $4T is in EM.

About $8T of that $12T is in advanced nations, and $4T is in EM.

However, most of that $12T offshore USD debt is not owed to US institutions.

It is mostly owed to other non-US institutions. (ie Chinese or European firms lend to other countries in USD), so it mostly nets out for assets and liabilities. (Someone’s liab is someone else’s asset.)

It is mostly owed to other non-US institutions. (ie Chinese or European firms lend to other countries in USD), so it mostly nets out for assets and liabilities. (Someone’s liab is someone else’s asset.)

In other words, the collective ex-US world is not “short USD”. They are collectively “leveraged USD”, having both long and short USD positions among themselves. That is a key distinction.

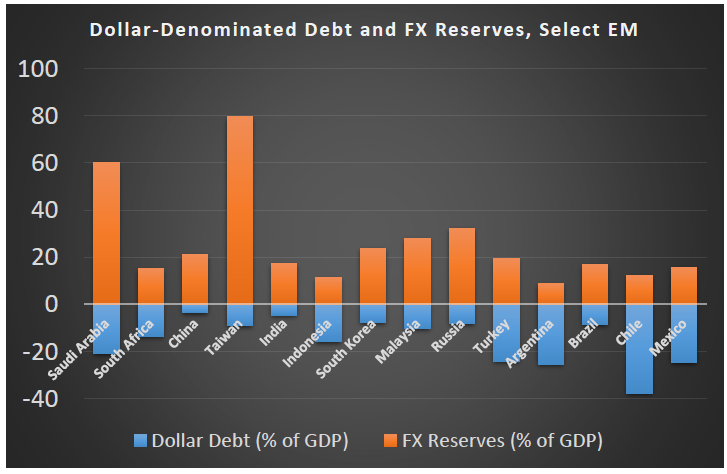

There are individual places that are very net short USD (ie Chile, Argentina…).

There are individual places that are very net short USD (ie Chile, Argentina…).

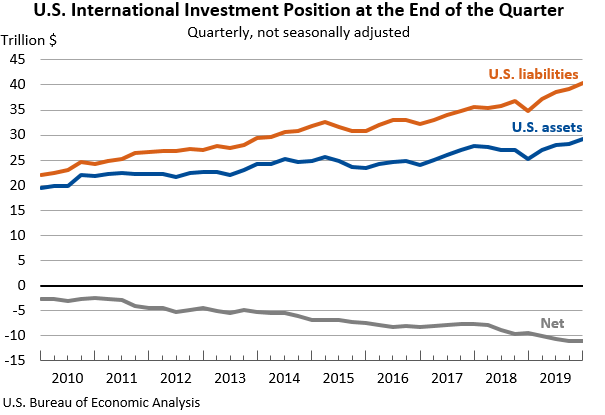

In addition to that rather balanced USD position overall (on both asset & liab sides of the $12T USD debt), the collective ex-US world owns $40T in gross US assets (treasuries, stocks, real estate, corp bonds) on top of that, built from decades of accumulated U.S. trade deficits.

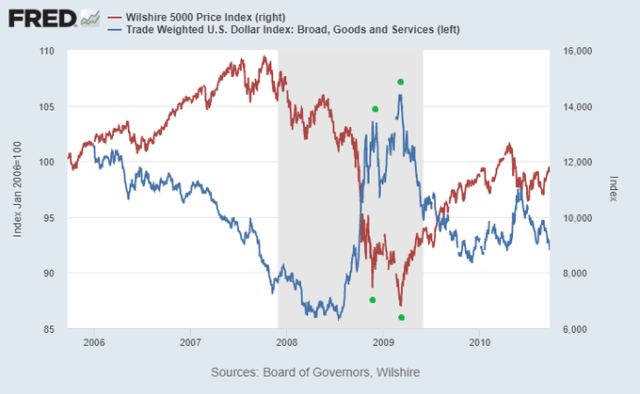

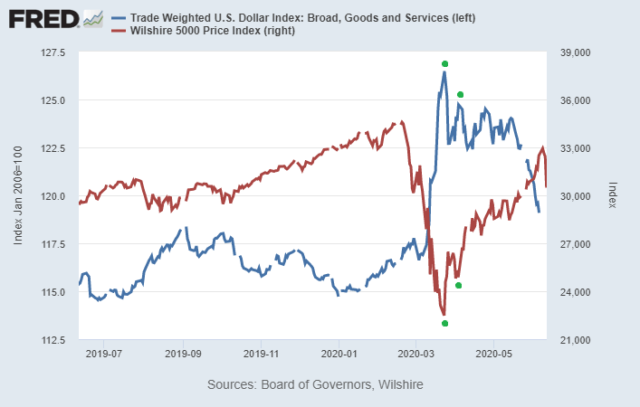

When trade diminishes and it becomes harder for the foreign sector to get dollars, it can cause a squeeze in the dollar to high levels. This is bad for liquidity, and can force some countries to sell U.S. assets to get dollars.

Sharp dollar spikes tend to coincide with sharp US market sell-offs.

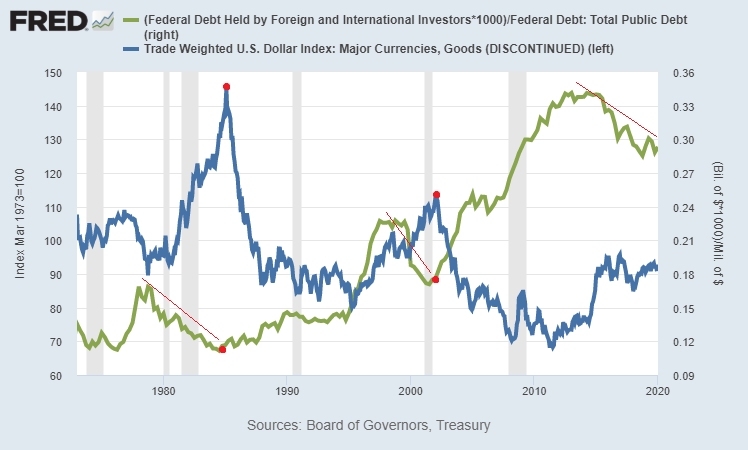

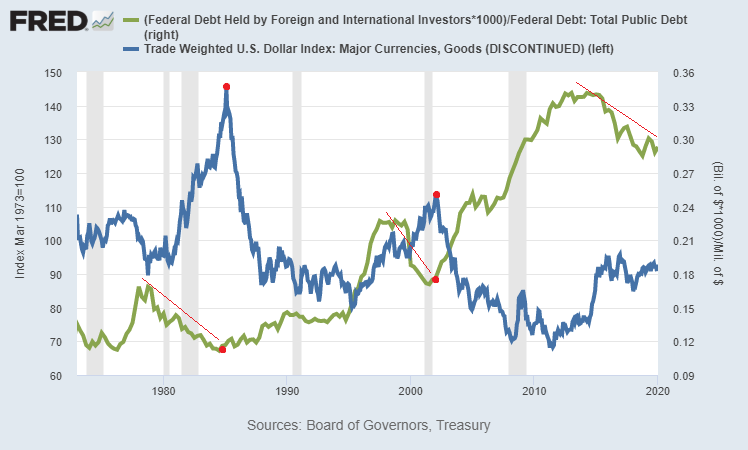

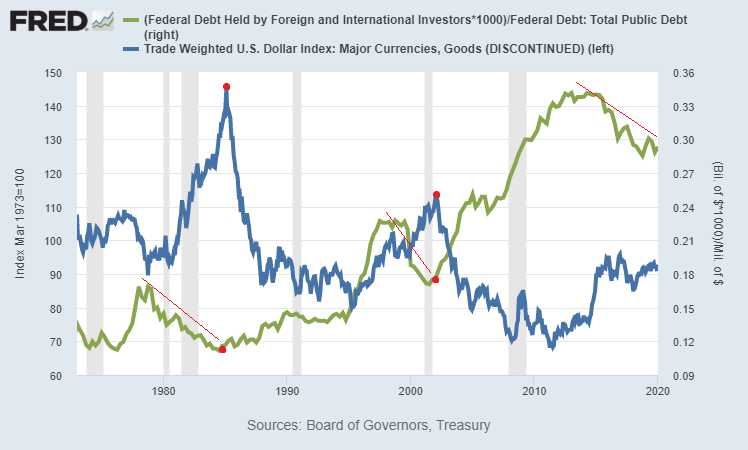

During the three major USD bull cycles since 1971, when the USD gets very strong, foreigners buy fewer Treasuries, forcing the US domestic sector (“crowding out” effect) or the Fed (“debt monetization”) to buy most new Treasury supply.

This chart shows the % of US Treasuries held by foreigners compared to the trade-weighted dollar. When USD gets strong, foreigners don’t really buy much Treasuries, even though Treasury supply keeps increasing due to fiscal deficits. Foreign % of US funding diminishes.

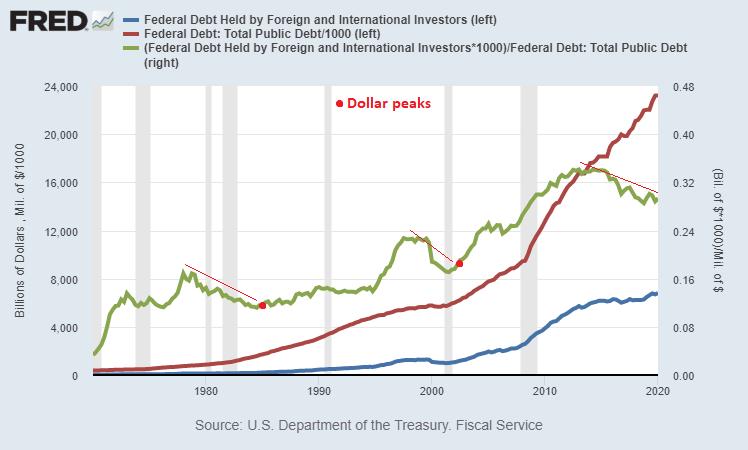

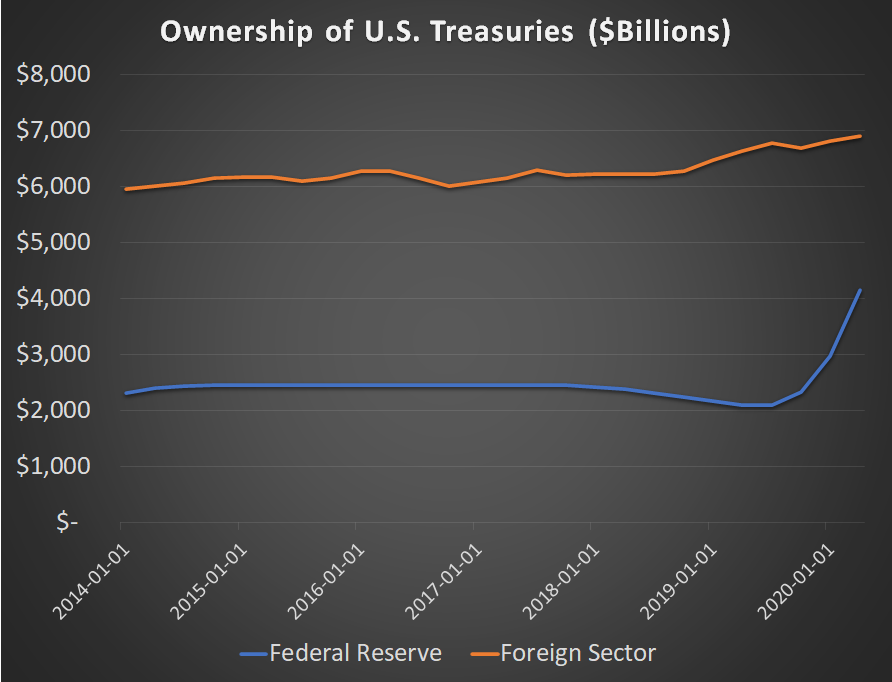

This chart shows total US federal debt (red), the foreign-held portion of those Treasuries (blue), and the percentage of US debt held by foreigners (green).

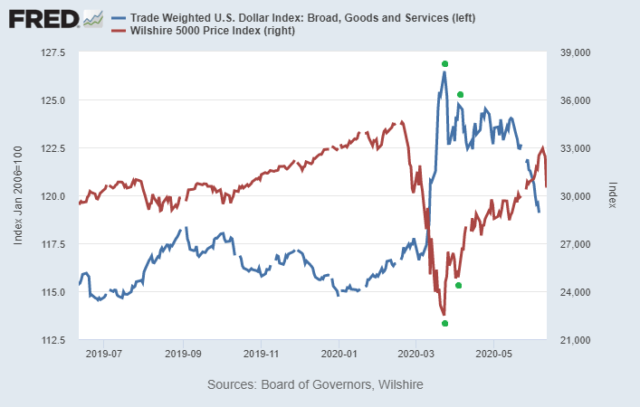

In March and April, the foreign sector sold $300B in US Treasuries at a time when the Treasury was about to do record Treasury issuance, and the Treasury market became illiquid. The Fed cited this repeatedly, and started buying Treasuries and lending USD swap lines.

In fact, the Fed accumulated more US Treasuries in March and April by printing new dollars, than the entire foreign sector accumulated in the past 6-7 years.

In other words, debt monetization quickly outpaced foreign lending.

In other words, debt monetization quickly outpaced foreign lending.

The Fed provided USD liquidity swaps (blue line below) with at least 15 foreign central banks to relieve global USD shortage and stop forced-selling of US assets (red line). So far, that worked, with the TED spread down, and foreign sector no longer selling Treasuries.

Some people think the US will weaponize swap lines among those 15+ foreign CBs. However, almost all of the swap line funding went to ECB, BOJ, and BOE. Most other countries barely used the swap lines.

So, the idea that we should avoid investing in jurisdictions without swap lines, or that the US will pressure a variety of individual countries with swap line threats, doesn’t add up. Swap lines mainly went to places that are not USD insolvent, but USD illiquid (ECB + BOJ).

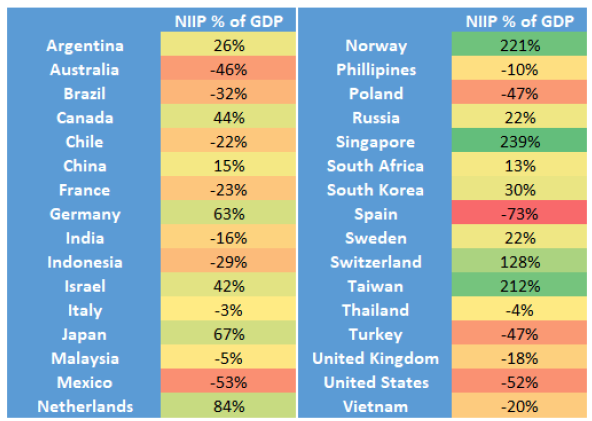

For big economic areas (Europe, Japan, China, and some major EM), a strong dollar is a liquidity issue, not a solvency issue. They have more USD assets than liabilities. Europe and Japan in particular together have $115T in net worth, including a lot of USD assets.

For weak EM and a large portion of frontier markets, a strong dollar is a solvency issue for them (not just liquidity), because they have USD debts but not really much USD assets.

Many of them are still in danger. Most of them don't have swap lines anyway. Localized problems.

Many of them are still in danger. Most of them don't have swap lines anyway. Localized problems.

But as described, a strong dollar also creates a liquidity issue for the US, especially during an acute USD spike causing stronger foreign markets to sell some of their US assets to get USD. So, the US really doesn’t have much leverage against other big countries.

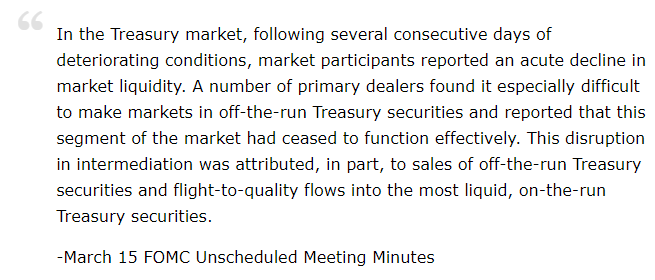

Here is the Fed describing the US Treasury market ceasing to function effectively in March, resulting in the Fed doing up to $75B/day in peak QE, extending swap lines, and launching an alphabet soup of programs.

This is why the dollar tends to trade in big cycles. Periods of extreme tightness end up negatively affecting the US (asset prices, corporate profits), and forcing the Fed to shift to more dovish policy, which eventually relieves the dollar.

In other words, this chart again:

In other words, this chart again:

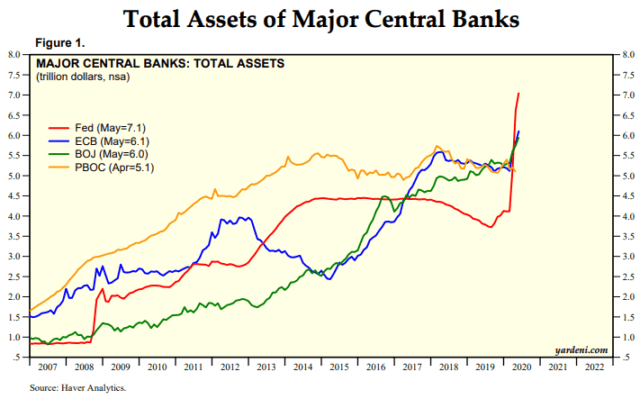

Since September 2019 (repo spike) and especially since March 2020, the Fed has grown its balance sheet faster than ECB or BOJ in absolute terms and as a percentage of GDP.

Others might play catch-up in 2H2020, but US is also likely to do more fiscal then as well.

Others might play catch-up in 2H2020, but US is also likely to do more fiscal then as well.

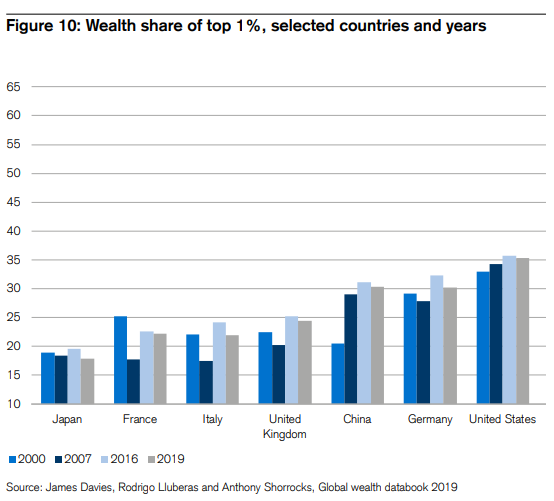

The median American has less wealth than the median Japanese or European citizen. The US has more wealth concentration, more reliance on the service sector, more people on the brink of insolvency.

Probably tons of fiscal coming over the next 3-5 years.

Probably tons of fiscal coming over the next 3-5 years.

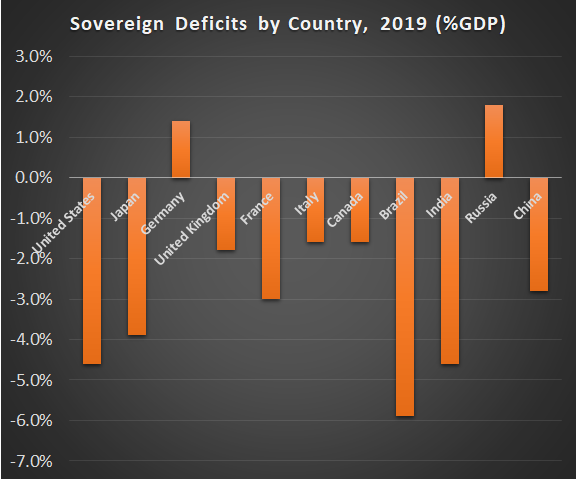

The US went into this pandemic with the biggest fiscal deficit as a % of GDP among major developed countries, and have been the biggest spender/printer as a % of GDP in this pandemic as well. The US also has a structural trade deficit.

This is why, although there can be more USD tightness or perhaps even another brief spike, I consider a strong probability of being near the end of this current dollar bull cycle, ever since the Fed was forced to shift to QE in Sep 2019.