Central bank swap lines were instrumental in quelling #DollarFunding stresses back in March

The latest #BIS_Bulletin provides a bird's eye perspective, showcasing the use of BIS banking statistics at its best bis.org/publ/bisbull27…

A thread follows

The latest #BIS_Bulletin provides a bird's eye perspective, showcasing the use of BIS banking statistics at its best bis.org/publ/bisbull27…

A thread follows

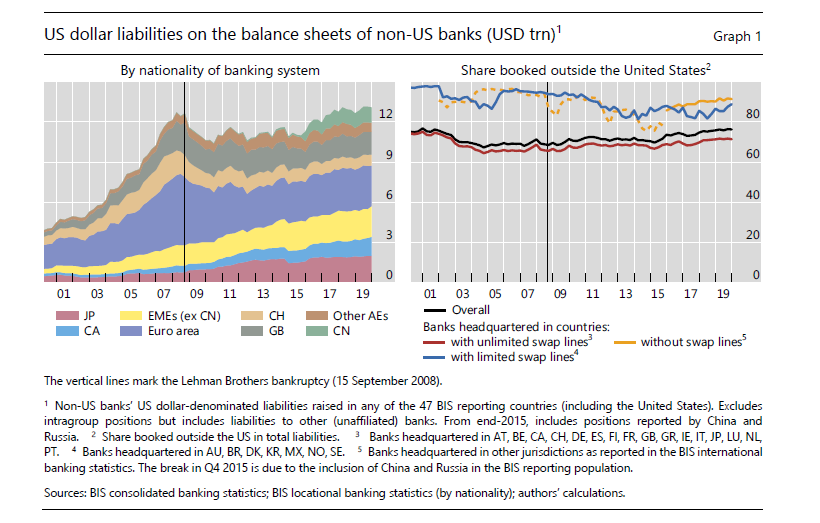

First thing to say is that #DollarFunding need outside the Unites States is big; dollar liabilities of non-US banks comes in at 13 trillion dollars - this is the same figure as just before the GFC

But notice the shift in the composition; the GFC was essentially a transatlantic crisis, with European banks at the eye of the storm.

European banks have retrenched, but others have taken their place; Asian EMEs are especially notable

European banks have retrenched, but others have taken their place; Asian EMEs are especially notable

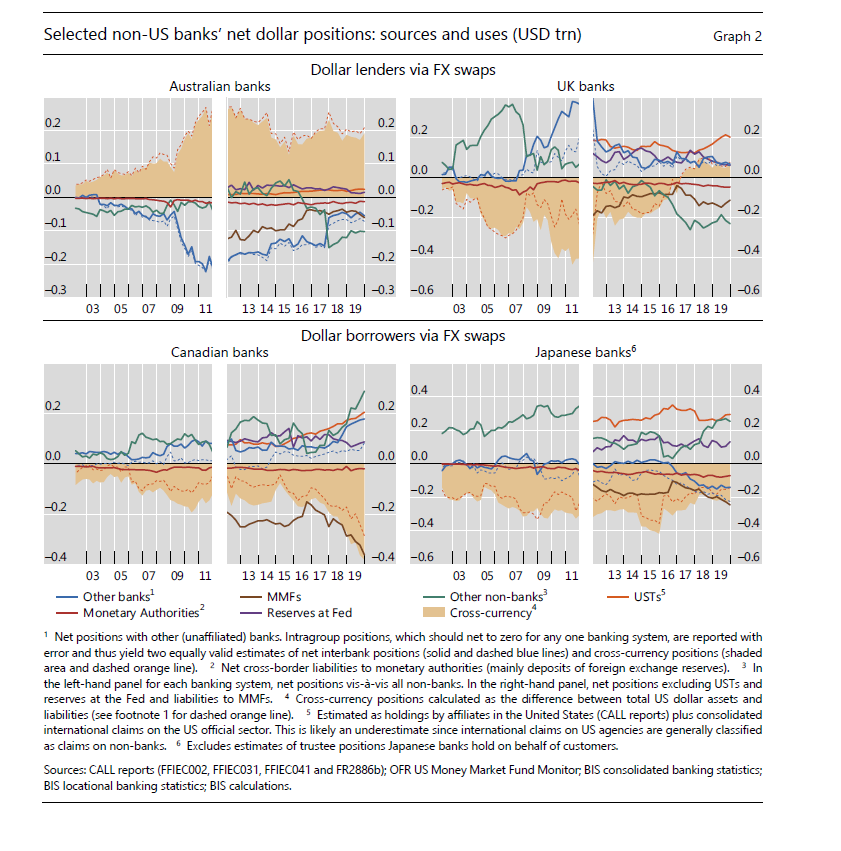

But the bald figures don't tell the whole story; while the banks were at the epicentre of the crisis last time round in 2008, the banks have played a different role this time

Banks accommodate FX hedging demand from fixed income investors who have obligations to domestic investors in euros or yen, but hold a portfolio heavy in dollar-denominated instruments; see, eg, bis.org/publ/bisbull01…

This is why #DollarFunding pressures are mostly an advanced economy phenomenon; this elegant piece by @senoj_erialc spells it out well ftalphaville.ft.com/2020/03/24/158…

But not everyone is the same; banking jurisdictions can be sorted into "dollar borrowers" and "dollar lenders"; it's the dollar borrowers who feel the brunt of the #DollarFunding stresses when they materialise

Here is the technical appendix that takes you through how the sausage is made bis.org/publ/bisbull27…

We can say more.

The gross #DollarFunding amounts tell only part of the story; short-term liabilities can be more telling, and we also need to factor in how much short-term assets banks have

The gross #DollarFunding amounts tell only part of the story; short-term liabilities can be more telling, and we also need to factor in how much short-term assets banks have

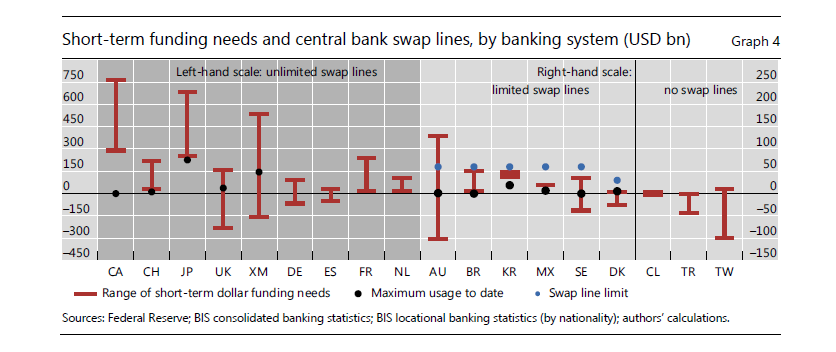

When bringing all the pieces together, we can get a pretty good picture of the lower and upper bounds of the *net* #DollarFunding gaps

So, here is the punchline of today's #BIS_Bulletin in one chart

So, here is the punchline of today's #BIS_Bulletin in one chart

It turns out that the estimate of net #DollarFunding gaps are pretty well matched by the size central bank swap lines announced by the Fed in March

But as the authors note, their analysis only gets at the net #DollarFunding gap for banks; corporates borrow in dollars and potential stresses will only show up when the next flare up happens

But most importantly, measuring funding gaps for the *borrowers* is missing a big chunk of the #DollarFunding stresses

Emerging market sovereigns borrow almost exclusively in domestic currency: around 89 percent of the total, in the latest BIS Quarterly Review bis.org/publ/qtrpdf/r_…

But the currency mismatch has migrated from the borrowers (who borrow in domestic currency) to the lenders (the asset managers) who hold EME sovereign bonds without FX hedging

Agustin Carstens and I have dubbed this "Original Sin Redux" in homage to the classic "Original Sin" literature started by Eichengreen, Hausmann and Panizza

This earlier #BIS_Bulletin piece discusses how Original Sin Redux played out this time round bis.org/publ/bisbull05…

One final word:

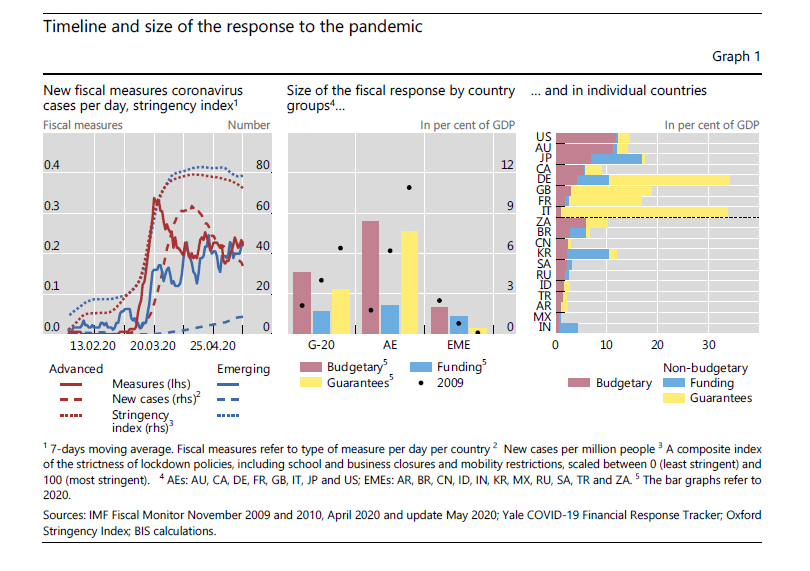

The fiscal response to the Covid-19 pandemic has been substantial and swift; it was one of the defining moments in the policy response...

The fiscal response to the Covid-19 pandemic has been substantial and swift; it was one of the defining moments in the policy response...

...but fiscal space is key, and for emerging market economies, this means being able to overcome Original Sin Redux

#DollarFunding matters here, even though you've borrowed in domestic currency, because stabilising the exchange rate helps to quell the capital flow reversals and help to deepen the domestic currency bond market

In short, dollar swap lines and other ways to maintain dollar liquidity are pretty important... to say the least