.@noyesclt had a good blog post where he called @Square a potential loser due to @Apple's purchase of @mobeewave

I respectfully disagree with Tom. Square will remain the leader for next gen POS and SMB services. But Fiserv, and Visa and MC may have a new threat. Thread below.

I respectfully disagree with Tom. Square will remain the leader for next gen POS and SMB services. But Fiserv, and Visa and MC may have a new threat. Thread below.

First a story. I saw a demo two years ago where a large online acquirer (think Adyen-like) had someone take a tap payment via their cell phone. No extra hardware.

As a Square shareholder, I almost shit my pants.

As a Square shareholder, I almost shit my pants.

I texted a few other folks in payments about what I saw (they had the chance, but missed the demo). We agreed Square would be toast.

Two years later, and Square is still chugging along and growing. So what gives?

Two years later, and Square is still chugging along and growing. So what gives?

I think three things give: (1) vaporware is easy, (2) POS acceptance is more than just the credential handshake and (3) market leader halos are hard to steal.

1st - Vaporware is easy. Apparently the card networks have had tools that developers could have used for a while to turn a phone into a POS. But the tools don’t really support a business offering at scale. And apparently haven’t gotten better, otherwise everyone would do it.

As my friends @ohad and @ohadsamet both know - risk stuff is hard!

Square has market-leading risk tooling, based on years of losses and near losses, and years more of heavy investment to make “Risk” a first-class product within Square.

Square has market-leading risk tooling, based on years of losses and near losses, and years more of heavy investment to make “Risk” a first-class product within Square.

Why? Square was doing well pre-IPO, but leading up to that the company fell prey to a travel-voucher based ponzi scheme. $5M gone. There was a big internal effort to post-mortem it internally and close gaps.

wowt.com/content/news/P…

wowt.com/content/news/P…

The next year, Risk became one of the four 2016 focus areas. Square would exit 2016 with market-leading risk tools, teams and practices. Jack and the exec team committed to never letting this happen again.

Apple would have to spend heavily and take time to build the same kind of app, teams, tools, practices and dataset that Square has. They have the cash, but do their business teams know the roadmap and do they have the stomach for the ups and downs before the finish line?

This is where .@noyesclt raises a good point in his blog.

Apple doesn’t have to compete with Square head on - maybe they just enable the banks to do it.

Apple doesn’t have to compete with Square head on - maybe they just enable the banks to do it.

I think this is where Apple is going. They took the phone, watch and browser and erected toll roads for commerce. Banks had fomo and took Apple’s terms without much negotiation.

Apple now makes a few cents on each ApplePay transaction thanks to tokenization and processing fees.

Apple now makes a few cents on each ApplePay transaction thanks to tokenization and processing fees.

.@noyesclt hints that maybe Apple will build a similar experience for merchant acceptance.

Onboard your bank to Apple’s card acceptance wallet. Bank uses Apple to auth/capture with the networks. Bank holds all the funds and manages SMB customer experience.

Onboard your bank to Apple’s card acceptance wallet. Bank uses Apple to auth/capture with the networks. Bank holds all the funds and manages SMB customer experience.

This is Apple as First Data.

In case those last six words were jargon - here’s some unpacking.

Large banks have payment processing arms. The dirty industry secret is that most of these arms run on top of joint ventures between the bank and First Data.

Wells Fargo Merchant Services? Actually First Data.

Bank of America Merchant Services? Actually First Data.

Wells Fargo Merchant Services? Actually First Data.

Bank of America Merchant Services? Actually First Data.

So when Square, PayPal and others build on top of Wells Fargo, they’re actually serving as an ISO on top of the First Data processing platform. Chase has Paymentech. Fifth/Third (shout out @john_piazzaIV) had Vantiv.

Banks and Fintech cos (no FinTechs here @iankar_) are basically just apps on top of First Data infra.

Why is First Data special? Because they help banks directly connect to, and manage data with, Visa and MC. FD also sells this as its own acquiring business. Now part of Fiserv.

Why is First Data special? Because they help banks directly connect to, and manage data with, Visa and MC. FD also sells this as its own acquiring business. Now part of Fiserv.

So why can’t this be Apple?

Both would help banks process card transactions on behalf of customers. If Apple can do this for SMBs via phones, why not for enterprise and completely disrupt First Data/Fiserv and other acquiring technology arms?

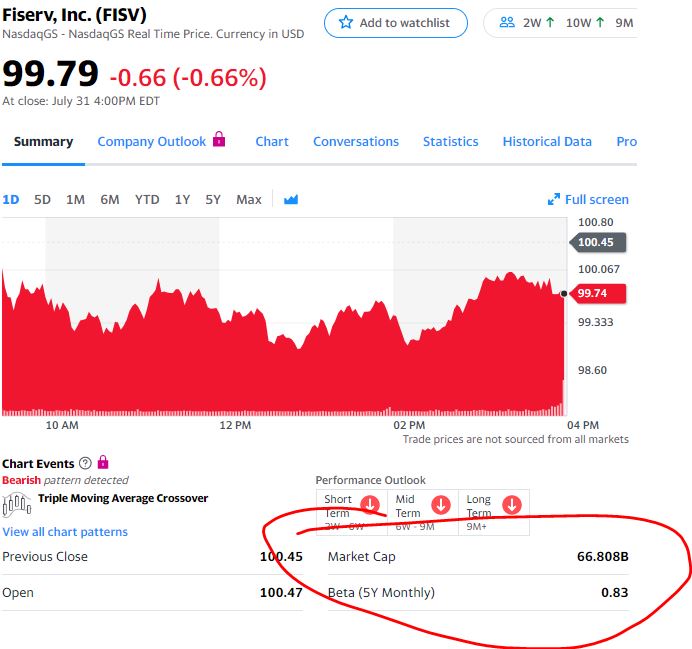

(Fiserv Market Cap pictured below)

Both would help banks process card transactions on behalf of customers. If Apple can do this for SMBs via phones, why not for enterprise and completely disrupt First Data/Fiserv and other acquiring technology arms?

(Fiserv Market Cap pictured below)

Back to Square and Apple, I think this actually helps Square.

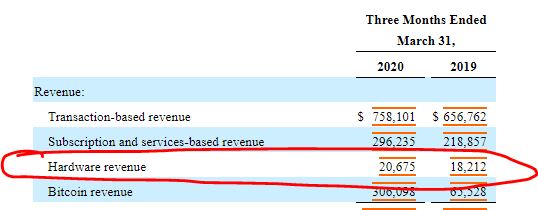

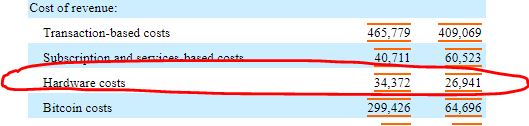

First, Square spends more on hardware each quarter than it makes in hardware revenue. This is likely due to the costs involved in Square’s hockey puck NFC and chip reader.

Q1 2020 Rev of $20.6M

Q1 2020 Costs of $34.3M

Q1 2020 Rev of $20.6M

Q1 2020 Costs of $34.3M

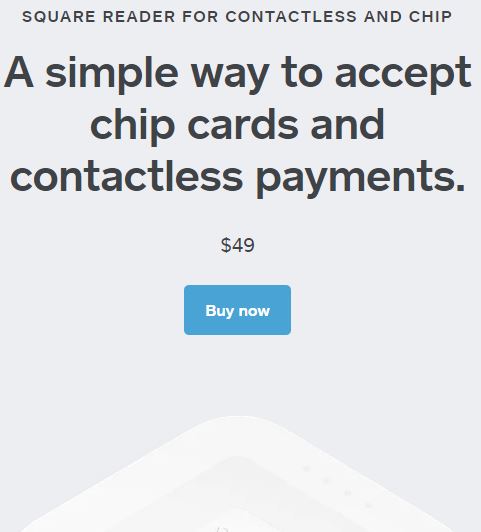

The reader is priced ~$50. SQ invested heavily in getting the networks and PCI to accept its pin on glass standard, which means SQ can cut the legacy costs of having a tamper-proof PIN pad locked to the reader.

These old PIN pad readers with EMV secure elements used to cost well over $200. SQ has been able to bring the price down by cutting it out, but likely still loses money with each $50 sale of the reader.

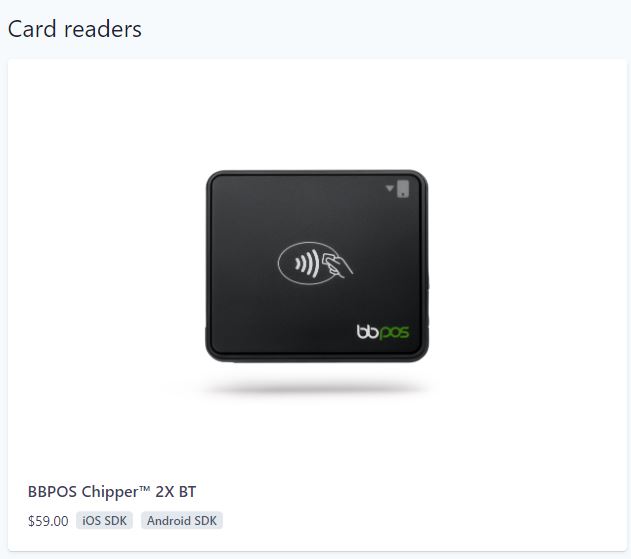

How much? Well BBPOS has a comparable model in market. The Chipper 2X BT.

BBPOS deftly does not disclose rack rate pricing on its Website, but some sleuthing shows a range of costs.

BBPOS deftly does not disclose rack rate pricing on its Website, but some sleuthing shows a range of costs.

Xola sells the Chipper for $99.

Authorize.net (owned by Visa) and Commerce Technologies both sell it for $85. Visa usually does a lot to drive network adoption, so I’m guessing this is ~ the wholesale cost. Let’s say a possible markup of $5 to $15 due to mid-level mgmt at Authorize trying to profit.

.@stripe sells the Chipper for $59. If you don't know about their hardware expansion, check out their terminal offering. Very slick.

So then there’s Square, selling their version for $50. Square isn’t Apple when it comes to hardware numbers, so they’re unlikely getting a great pricing discount from their Asian manufacturing partners. Ergo, Square is selling at some kind of loss.

Assuming Stripe is selling at cost ($59 -lowest price I found), Square is losing at least $10 on each NFC/EMV reader. Apple turning its phone into a tap-n-go terminal makes this Square product obsolete. Also removing a cost (and loss) from Square’s quarterly numbers.

But Matt, you say, you teased us with something on V and MC, too.

And I didn’t forget.

And I didn’t forget.

If you’re reading this, you either have insomnia or know payments is two sided. With Apple Pay as big as it is, bringing merchant acquiring to the fold gives Apple a data play on both sides of the networks.

Today and in the future, those transactions will run over the traditional payment networks.

But in the future, what’s stopping Apple from cutting out V or MC? Why can’t this turn into a Chasenet-like offering?

But in the future, what’s stopping Apple from cutting out V or MC? Why can’t this turn into a Chasenet-like offering?

Now I don’t think Apple will do that. It's a ton of work, outside their core expertise, and why bother when you can use the threat of building a network to extract fee revenue concessions from current incumbents?

But it’s why I don’t think Apple’s purchase makes Square a loser.

But it’s why I don’t think Apple’s purchase makes Square a loser.

Apple should be pushing to make banks -- not SMBs -- customers. Some banks may bring SMBs over to Apple, but Square’s core should remain intact.

Remember, banks have been ignoring SMBs for a while. That’s why Square, PayPal, Stripe, Kabbage, BlueVine and others exist.

Remember, banks have been ignoring SMBs for a while. That’s why Square, PayPal, Stripe, Kabbage, BlueVine and others exist.

If you’re an SMB that couldn’t get a small business loan from your bank, are you really going to run skipping when they roll out Apple’s payment acceptance solution? What about when they hit you with monthly fees for your business checking account?

That’s where @square will keep chugging along. Payments, payroll, CRM, inventory, loans and (soon) banking all under one roof. Easy to use. Easy to understand. Fair pricing.

My thread broke midway, so reconnecting it all here.

(Yes - I know - cue the DMs about needing a blog)

(Yes - I know - cue the DMs about needing a blog)