1/ A quick thread on our new paper

Rebalance Timing Luck: The (Dumb) Luck of Smart Beta

Available at:

- epsilontheory.com/rebalance-timi…

- papers.ssrn.com/sol3/papers.cf…

Rebalance Timing Luck: The (Dumb) Luck of Smart Beta

Available at:

- epsilontheory.com/rebalance-timi…

- papers.ssrn.com/sol3/papers.cf…

3/ Okay, so what's the core problem we're trying to tackle here?

Lots of systematic equity strategies (such as "smart beta" ETFs) rebalance on a fixed schedule (e.g. every June and December).

Does the choice of "when" matter?

Lots of systematic equity strategies (such as "smart beta" ETFs) rebalance on a fixed schedule (e.g. every June and December).

Does the choice of "when" matter?

4/ This work builds off our prior published research Rebalance Timing Luck: The Difference Between Hired and Fired (jii.pm-research.com/content/10/1/2…), which studies this effect on a fixed-mix 60/40 portfolio and derives a formula for estimating the impact.

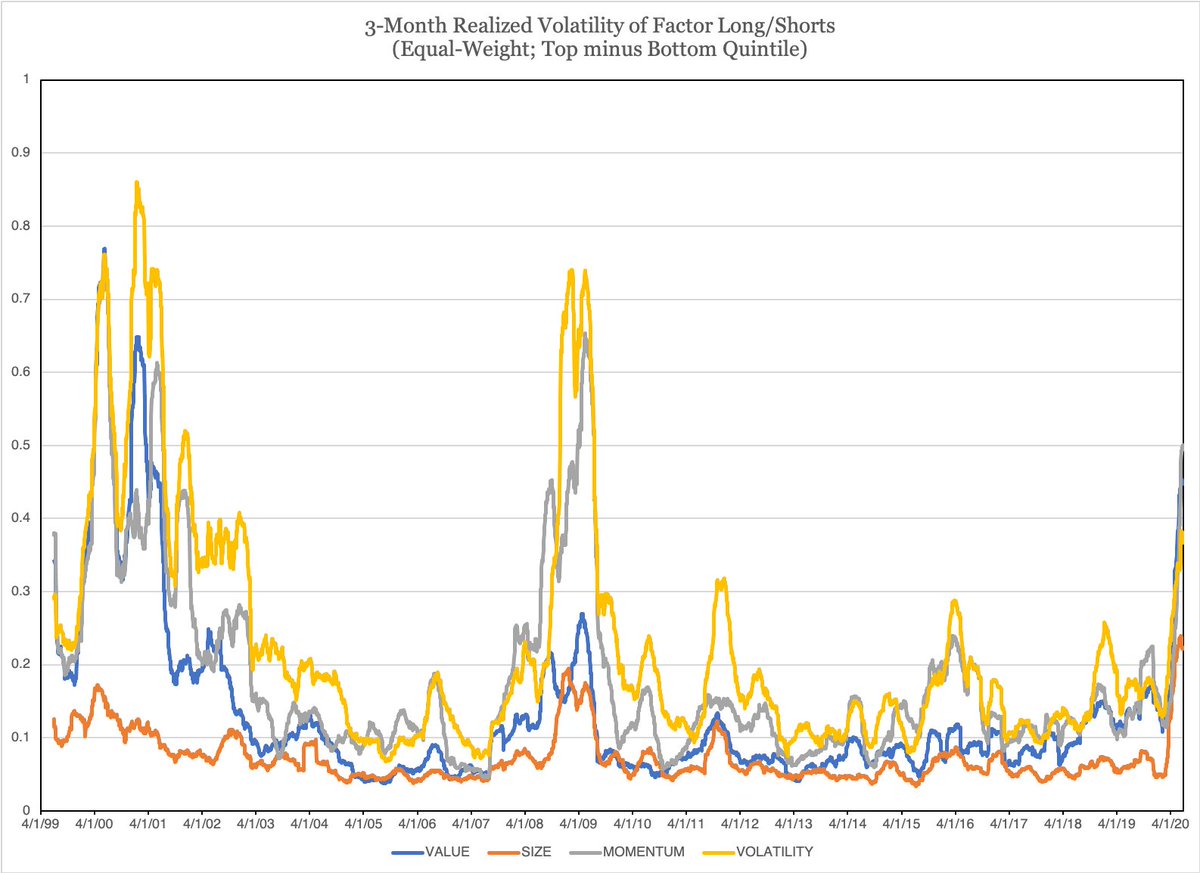

5/ In this paper we explore simple value, momentum, quality, and low vol strategies applied within large-cap U.S. equities.

To measure the impact of rebalance timing luck ("RTL"), we construct the same strategy, rebalanced at the same frequency, but on different schedules.

To measure the impact of rebalance timing luck ("RTL"), we construct the same strategy, rebalanced at the same frequency, but on different schedules.

6/ So, for example, we might sort stocks sorted on prior 12-1 month returns and rebalance the portfolio every three months (the frequency), but construct 3 variations:

1. JAN-APR-JUL-OCT

2. FEB-MAY-AUG-NOV

3. MAR-JUN-SEP-DEC

1. JAN-APR-JUL-OCT

2. FEB-MAY-AUG-NOV

3. MAR-JUN-SEP-DEC

7/ The difference in returns of those three variations can be attributed entirely to *when* they rebalanced.

We find that increasing concentration and decreasing rebalance frequency coincide with larger performance dispersion.

We find that increasing concentration and decreasing rebalance frequency coincide with larger performance dispersion.

8/ This aligns with our prior research which suggests three primary drivers of RTL:

1. How frequently the portfolio is rebalanced

2. How much turnover the strategy exhibits

3. How constrained the implementation is

1. How frequently the portfolio is rebalanced

2. How much turnover the strategy exhibits

3. How constrained the implementation is

9/ More broadly: rebalance timing luck captures the difference between what a strategy is invested in today versus what it COULD be invested in HAD it actually rebalanced.

10/ Higher turnover (e.g. momentum vs value), slower rebalancing frequency (e.g. annual vs monthly), and fewer constraints (e.g. unconstrained vs industry neutral) all lead to greater implicit differences, and therefore INCREASE the impact of rebalance timing luck.

11/ So why does this matter?

Not only does this research suggest that RTL may be a substantial driver of return differences in the short-term (e.g. hundreds of basis points per year between identical strategies), but can lead to permanent impacts on realized wealth levels.

Not only does this research suggest that RTL may be a substantial driver of return differences in the short-term (e.g. hundreds of basis points per year between identical strategies), but can lead to permanent impacts on realized wealth levels.

12/ "These results call into question one’s ability to draw meaningful relative performance conclusions between two strategies, or a strategy and its benchmark, even if other variables such as factor definition and portfolio constructions methods are controlled."

13/ I'd like to acknowledge that @paradoxinvestor, Blitz, and van der Grient wrote about this issue back in 2010 and even suggested what I believe is the optimal solution (overlapping portfolios). Alas, their work has gone largely overlooked.

papers.ssrn.com/sol3/papers.cf…

papers.ssrn.com/sol3/papers.cf…

14/ If you invest in smart beta ETFs, I urge you to read this paper.

Or, at the very least, skim the pictures and read the conclusion like the rest of us usually do.

Feedback (very) welcome.

FIN.

Or, at the very least, skim the pictures and read the conclusion like the rest of us usually do.

Feedback (very) welcome.

FIN.