SushiSwap, the AMM that's attracted over $750M in TVL in under 70 hours, is trying to dethrone @UniswapProtocol.

But will it work?

But will it work?

1/ Think of @SushiSwap as a Uniswap clone with 1 major difference.

Trading fees are split between liquidity providers (LPs) and holders of $SUSHI, instead of between LPs & equity holders.

Trading fees are split between liquidity providers (LPs) and holders of $SUSHI, instead of between LPs & equity holders.

2/ To earn $SUSHI, you provide liquidity to Uniswap for one of the select assets, then stake your LP tokens from Uniswap into Sushi.

The plan is after 2 weeks, Sushiswap will then migrate your Uniswap liquidity into their own dex, essentially forking Uniswap.

The plan is after 2 weeks, Sushiswap will then migrate your Uniswap liquidity into their own dex, essentially forking Uniswap.

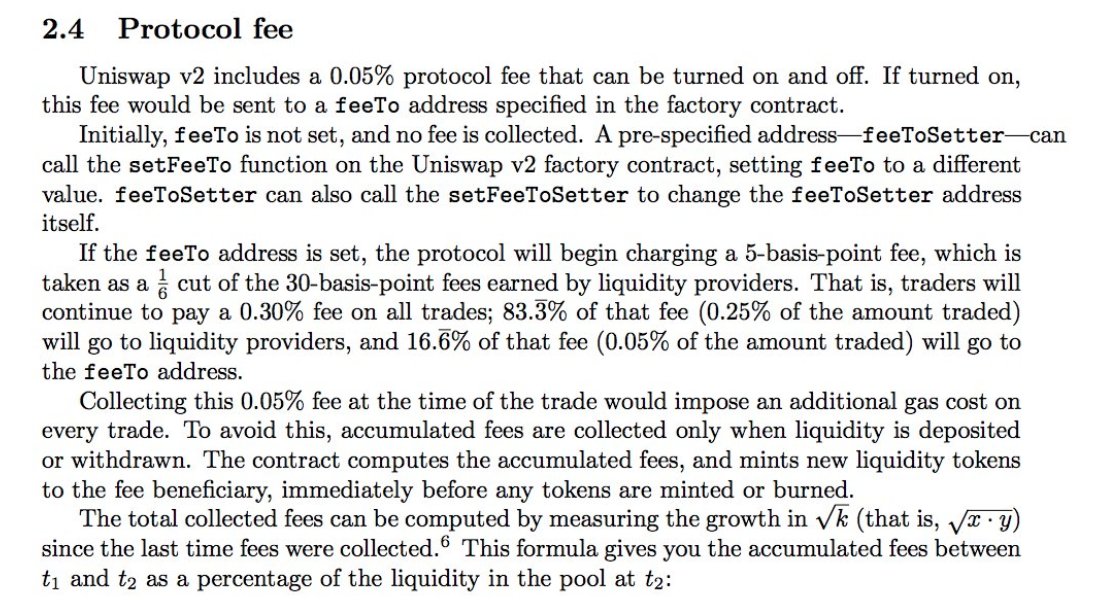

3/ Meanwhile, stakers earn $SUSHI tokens, which entitle them to a 0.05% tx fee for trades on Sushiswap.

The remaining 0.25% goes to liquidity providers.

This means @UniswapProtocol traders essentially pay the same fee (0.3%) on Sushi as they would on Uni.

The remaining 0.25% goes to liquidity providers.

This means @UniswapProtocol traders essentially pay the same fee (0.3%) on Sushi as they would on Uni.

4/ Say $SUSHI actually succeeds in forking at least part of Uniswap.

What does that look like?

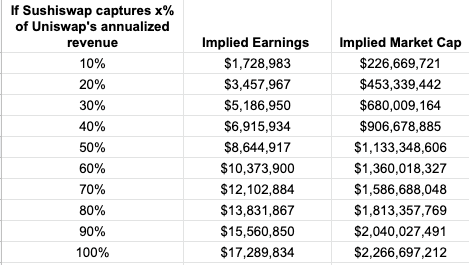

Taking into consideration the fee split to $SUSHI holders, assuming the median P/S from @tokenterminal for the 6 major dex protocols, the following scenarios are possible.

What does that look like?

Taking into consideration the fee split to $SUSHI holders, assuming the median P/S from @tokenterminal for the 6 major dex protocols, the following scenarios are possible.

5/ Obviously no one's *really* trading based on P/S today (just look at the range lol), but this is a starting point.

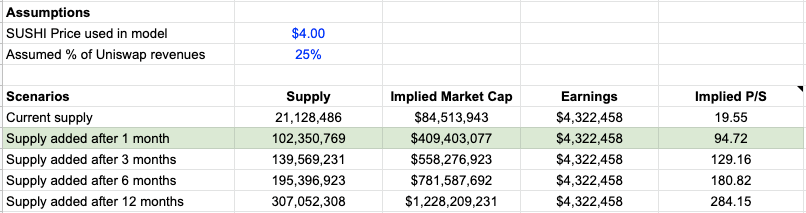

Token price is also highly sensitive to inflation. Feel free to play with the quick & dirty model below and lmk if anything's off.

docs.google.com/spreadsheets/d…

Token price is also highly sensitive to inflation. Feel free to play with the quick & dirty model below and lmk if anything's off.

docs.google.com/spreadsheets/d…

6/ Setting price and $SUSHI aside, the core idea of a liquidity migration is pretty interesting.

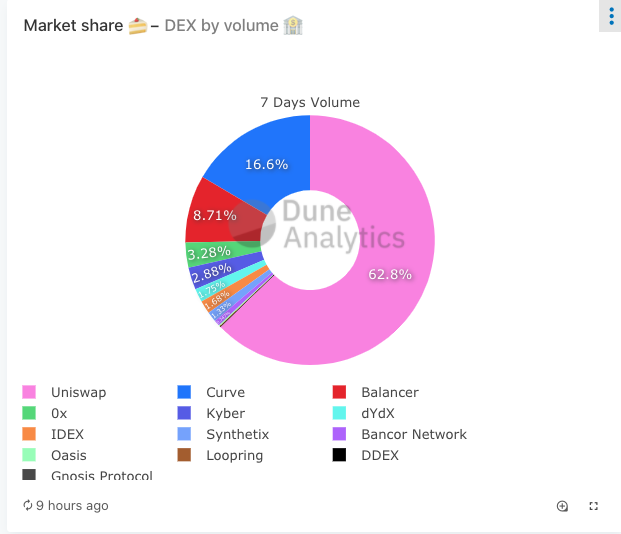

It reinforces my thesis that liquidity is a transient moat; the real moat is mindshare. Here, @UniswapProtocol is by *far* the strongest.

It reinforces my thesis that liquidity is a transient moat; the real moat is mindshare. Here, @UniswapProtocol is by *far* the strongest.

7/ But that also means this won't be the last token migration attempt.

Competitors see the fees Uniswap is generating and want a piece of the action.

Reminds me of Ethereum killers in 2017, but this time competitors are employing incentivized subversion.

Competitors see the fees Uniswap is generating and want a piece of the action.

Reminds me of Ethereum killers in 2017, but this time competitors are employing incentivized subversion.

8/ Key date to watch will be ~2 weeks from now, when $SUSHI incentives ratchet down.

My guess is that a lot of the capital will leave to greener pastures for farming, unless @SushiSwap can drastically differentiate its platform (besides token).

Why?

My guess is that a lot of the capital will leave to greener pastures for farming, unless @SushiSwap can drastically differentiate its platform (besides token).

Why?

9/ When Sushiswap comes live, LPs are the ones receiving and likely holding most $SUSHI.

Fees are split between LPs and $SUSHI holders.

This means the end result may not be that different from current version of @UniswapProtocol (LPs earning most fees).

Fees are split between LPs and $SUSHI holders.

This means the end result may not be that different from current version of @UniswapProtocol (LPs earning most fees).

10/ To do a rug pull, @UniswapProtocol can also issue its own token for fee distribution.

My guess is most everyday users likely also prioritize a safe, battle tested product and are okay with progressive decentralization. But I've been wrong before.

My guess is most everyday users likely also prioritize a safe, battle tested product and are okay with progressive decentralization. But I've been wrong before.

11/ For the sake of the argument, I do think there are a few ways that liquidity migration could potentially work on forking some Uniswap liquidity:

- Vertical-specific feature differentiation

- Another product with traction

- Vertical-specific feature differentiation

- Another product with traction

12/ There are a few "AMMs" that have material feature differentiation (@BreederDodo), and could retain users obtained via incentivized migration.

Profitable Uni LPs probably won't give up fat fees to join a new AMM, so this will probably only work on thinly traded pairs first.

Profitable Uni LPs probably won't give up fat fees to join a new AMM, so this will probably only work on thinly traded pairs first.

13/ What I would be more concerned about if I were Uniswap is if an existing product with material feature differentiation *and* significant growth + traction (@BalancerLabs ?) tries to do this...

If you can earn comparable fees to be an LP and get paid extra to do it, why not?

If you can earn comparable fees to be an LP and get paid extra to do it, why not?

Fin/ I'm curious about $SUSHI, but more excited about the idea behind liquidity migration.

This challenges my assumptions around first mover advantage, and highlights the fact that liquidity is not a moat.

AMMs will become highly competitive, and users will benefit.

This challenges my assumptions around first mover advantage, and highlights the fact that liquidity is not a moat.

AMMs will become highly competitive, and users will benefit.