I am very happy to share that my paper "Optimal Taxation with Home Ownership and Wealth Inequality" with Pietro Reichlin has been now accepted for publication at the @RevEconDyn [1/n] #EconTwitter

In the paper we consider optimal taxation in a model with wealth-poor and wealth-rich households, where wealth derives from business capital and home ownership, and investigate the consequences of a rising wealth inequality at steady state on these tax rates [2/n]

We find that the optimal tax structure includes some taxation of labor, zero taxation of financial and business capital, and critically a housing wealth tax on the wealth-rich households and a housing subsidy on the wealth-poor households [3/n]

We also find that the source of increasing wealth matters in the optimal balance between labor and housing wealth taxes [4/n]

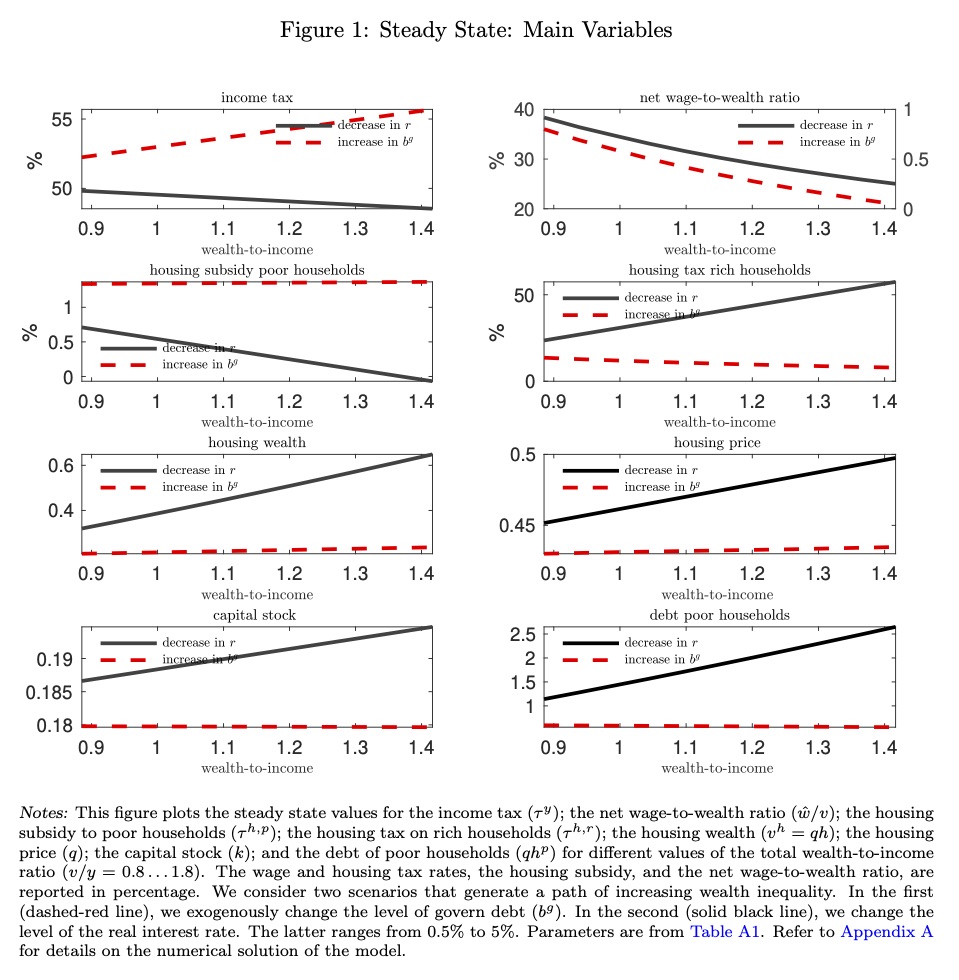

When wealth rises because of a rising public debt, then the optimal income tax rises with inequality, the housing subsidy is flat while the housing tax on rich households falls substantially [5/n]

When instead wealth rises because of a falling real rate, then the optimal income tax falls with inequality, the housing tax on the rich households rises strongly, and the housing subsidy falls a bit [6/n]

In both scenarios, housing subsidies are small, while the hosuing tax rates are large (see figure) [7/n]

Many more details and economic intuition in the paper (working paper available at ssrn.com/abstract=34891…) [8/n]

• • •

Missing some Tweet in this thread? You can try to

force a refresh