1/ There's been so much regulatory & enforcement news in crypto lately, it's impossible to keep up.

So instead of getting lost in the details, let's step back & consider the big picture. What's really going on here?

In short: an ideological war over self-custody & privacy. 👇

So instead of getting lost in the details, let's step back & consider the big picture. What's really going on here?

In short: an ideological war over self-custody & privacy. 👇

2/ This thread is long but very important.

If you believe in the principles of financial privacy & self-sovereignty at the heart of Bitcoin, as I do, you need to pay attention now.

We've made the world stage, but our biggest challenges still lie ahead.

If you believe in the principles of financial privacy & self-sovereignty at the heart of Bitcoin, as I do, you need to pay attention now.

We've made the world stage, but our biggest challenges still lie ahead.

https://twitter.com/jchervinsky/status/1146226075757940736?s=20

3/ Crypto market infrastructure has improved dramatically in recent years.

It's now quite easy for most people to convert fiat into crypto, withdraw any amount to their own wallet, & then do as they wish without restriction or identification, subject only to the consensus rules.

It's now quite easy for most people to convert fiat into crypto, withdraw any amount to their own wallet, & then do as they wish without restriction or identification, subject only to the consensus rules.

4/ There's some regulation at the on-ramps & off-ramps, but so far, not enough to seriously infringe on the freedoms of self-custody & privacy.

This is changing.

Policymakers' approach to AML regulation is shifting significantly toward harsher restrictions on a *global* scale.

This is changing.

Policymakers' approach to AML regulation is shifting significantly toward harsher restrictions on a *global* scale.

5/ AML regulations are intended to prevent criminals from using & abusing the financial system.

The goal is to make sure that "crime doesn't pay" -- to stop bad actors from spending illegally-obtained funds & to help law enforcement detect & prosecute the underlying crimes.

The goal is to make sure that "crime doesn't pay" -- to stop bad actors from spending illegally-obtained funds & to help law enforcement detect & prosecute the underlying crimes.

6/ AML regulations seek to accomplish this goal by deputizing financial institutions, the gatekeepers of the financial system, to act like government agents.

For example, regulated institutions are required to identify customers, surveil transactions, & file reports with gov't.

For example, regulated institutions are required to identify customers, surveil transactions, & file reports with gov't.

7/ AML regulations depend on intermediaries to perform the functions of identification, surveillance, censorship, seizure, exclusion, & more.

Enter Bitcoin -- a peer-to-peer electronic cash system that lets anyone transfer any amount of value to anywhere without intermediaries.

Enter Bitcoin -- a peer-to-peer electronic cash system that lets anyone transfer any amount of value to anywhere without intermediaries.

8/ AML regulations break down in the context of cash.

With no intermediary to deputize, gov'ts are less able to detect transactions, identify counterparties, determine sources of funds, conduct censorship & seizure, etc.

This is true for both paper cash & electronic cash.

With no intermediary to deputize, gov'ts are less able to detect transactions, identify counterparties, determine sources of funds, conduct censorship & seizure, etc.

This is true for both paper cash & electronic cash.

9/ Many gov'ts would love to get rid of paper cash & some are trying.

But paper cash doesn't pose that big a risk. Like gold, it only works for in-person transfers & isn't easy to move long distances in large amounts.

Regulators are much more concerned about digital transfers.

But paper cash doesn't pose that big a risk. Like gold, it only works for in-person transfers & isn't easy to move long distances in large amounts.

Regulators are much more concerned about digital transfers.

10/ For years, regulators have cracked down on digital transfers that use institutions like money transmitters & offshore banks.

But aside from the occasional "[country X] bans Bitcoin" headline, most gov'ts haven't tried to significantly restrict Bitcoin or other blockchains.

But aside from the occasional "[country X] bans Bitcoin" headline, most gov'ts haven't tried to significantly restrict Bitcoin or other blockchains.

11/ There are a few reasons for this.

First, gov'ts have been content to regulate on-ramps & off-ramps, partly on the belief that crypto's main utility comes from conversion into fiat.

They've been satisfied by limiting access to conversion & catching criminals in the process.

First, gov'ts have been content to regulate on-ramps & off-ramps, partly on the belief that crypto's main utility comes from conversion into fiat.

They've been satisfied by limiting access to conversion & catching criminals in the process.

12/ Second, gov'ts can track crypto transfers via blockchain analytics fairly easily, even supposedly private ones (sorry to break it to you).

Third, there really isn't that much criminal activity in crypto, so the overall risk is low & hasn't warranted a ton of gov't resources.

Third, there really isn't that much criminal activity in crypto, so the overall risk is low & hasn't warranted a ton of gov't resources.

13/ However, over the last year, Bitcoin has gained geopolitical significance & fiat-pegged stablecoin volume has exploded upward.

As a result, gov'ts are getting more concerned about both illicit activity & the threat to their monetary sovereignty (a topic for another day).

As a result, gov'ts are getting more concerned about both illicit activity & the threat to their monetary sovereignty (a topic for another day).

14/ So, what are they doing?

For starters, they're enforcing current AML regulations more aggressively.

Most of us expected BitMEX to get tagged by the CFTC for unregistered derivatives trading, but it was a big deal to see DOJ turn the case criminal. That doesn't happen often.

For starters, they're enforcing current AML regulations more aggressively.

Most of us expected BitMEX to get tagged by the CFTC for unregistered derivatives trading, but it was a big deal to see DOJ turn the case criminal. That doesn't happen often.

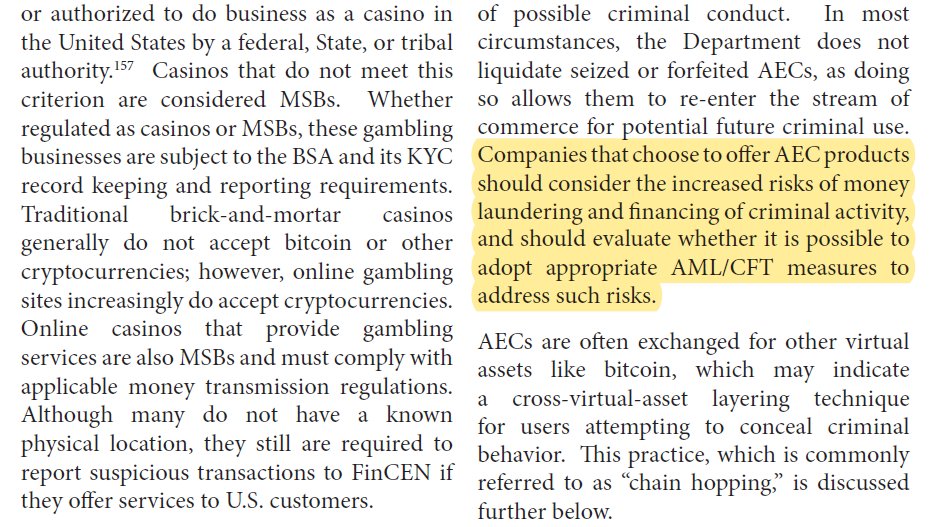

15/ They're also attacking privacy more aggressively.

Last week's DOJ Framework described anonymous transactions as "a high-risk activity...indicative of possible criminal conduct."

And it had an ominous warning for exchanges about "anonymity enhanced cryptocurrencies" (AEC):

Last week's DOJ Framework described anonymous transactions as "a high-risk activity...indicative of possible criminal conduct."

And it had an ominous warning for exchanges about "anonymity enhanced cryptocurrencies" (AEC):

16/ The phrase "...whether it is possible..." is heavily loaded.

Translated into DC speak, this means "we definitely don't think it's possible, so you better not, or else."

Keep in mind, this is a DOJ that disapproved of end-to-end encryption yesterday:

justice.gov/opa/pr/interna…

Translated into DC speak, this means "we definitely don't think it's possible, so you better not, or else."

Keep in mind, this is a DOJ that disapproved of end-to-end encryption yesterday:

justice.gov/opa/pr/interna…

17/ Perhaps most importantly, policymakers *worldwide* are signaling a desire to expand existing laws to restrict access to crypto.

Consider the "Swiss Rule," which practically prohibits self-custody in the guise of verifying the owner of a private key.

Consider the "Swiss Rule," which practically prohibits self-custody in the guise of verifying the owner of a private key.

https://twitter.com/jp_koning/status/1292882005277933569?s=20

18/ This June, the Financial Action Task Force (FATF), an international standard-setting body for AML regulation, said that the "lack of explicit coverage of peer-to-peer transactions...was a source of concern."

Next June, they might adopt the Swiss Rule as a global standard.

Next June, they might adopt the Swiss Rule as a global standard.

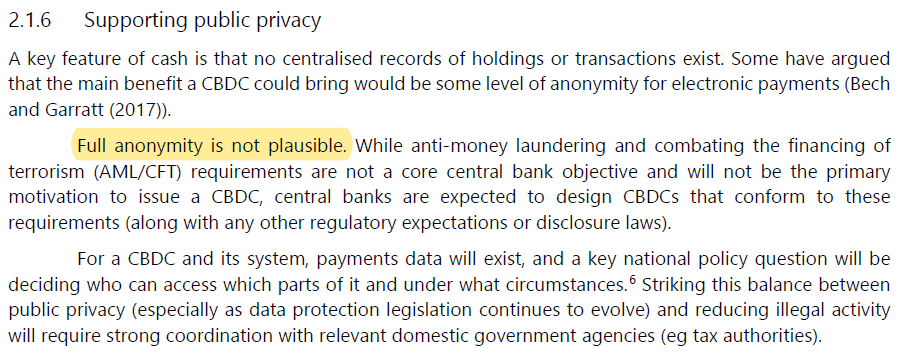

19/ I won't bother reciting all the recent gov't statements targeting financial privacy as a major risk. There are too many.

The Bank for International Settlements (BIS) said it all in its report on central bank digital currencies last week:

"Full anonymity is not plausible."

The Bank for International Settlements (BIS) said it all in its report on central bank digital currencies last week:

"Full anonymity is not plausible."

20/ I fear we're heading for a world where withdrawing crypto from exchanges to self-custody is restricted as a means of attacking privacy.

We'd have two separate crypto markets: one of "clean" custodial coins & another of "dirty" self-sovereign ones, with no bridge between.

We'd have two separate crypto markets: one of "clean" custodial coins & another of "dirty" self-sovereign ones, with no bridge between.

21/ This is a worst-case scenario, to be sure, & all hope isn't lost.

Many of us are working to convince policymakers why it's a terrible idea, & I'll have a lot more to say on that soon.

But you should know that it's a live issue, & our main challenge for years to come.

[end]

Many of us are working to convince policymakers why it's a terrible idea, & I'll have a lot more to say on that soon.

But you should know that it's a live issue, & our main challenge for years to come.

[end]

• • •

Missing some Tweet in this thread? You can try to

force a refresh