1/ Resurrecting the Value Premium (Blitz, Hanauer)

"We use more powerful value metrics, apply basic risk management, and make more effective use of the breadth of the liquid universe of stocks and conclude that a healthy value premium is still present."

papers.ssrn.com/sol3/papers.cf…

"We use more powerful value metrics, apply basic risk management, and make more effective use of the breadth of the liquid universe of stocks and conclude that a healthy value premium is still present."

papers.ssrn.com/sol3/papers.cf…

2/ "The big-cap component of HML has been flat on balance since the early 1980s.

"HML has been critically dependent on the efficacy of B/M in the small-cap space. The concern that the HML premium is seriously impaired or may even have disappeared does not seem unreasonable."

"HML has been critically dependent on the efficacy of B/M in the small-cap space. The concern that the HML premium is seriously impaired or may even have disappeared does not seem unreasonable."

3/ "The U.S. post-publication HML value premium is less than 1% per annum with an insignificant t-stat. The big-cap HML component even displays a negative average return.

"The only significant HML performance in Developed-ex-US and Emerging Markets is in the small-cap space."

"The only significant HML performance in Developed-ex-US and Emerging Markets is in the small-cap space."

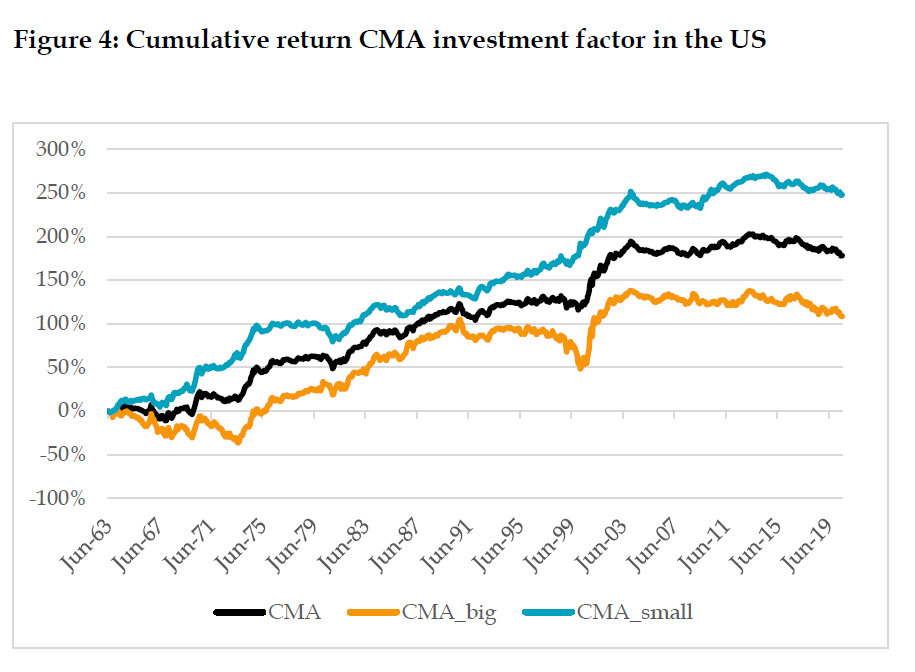

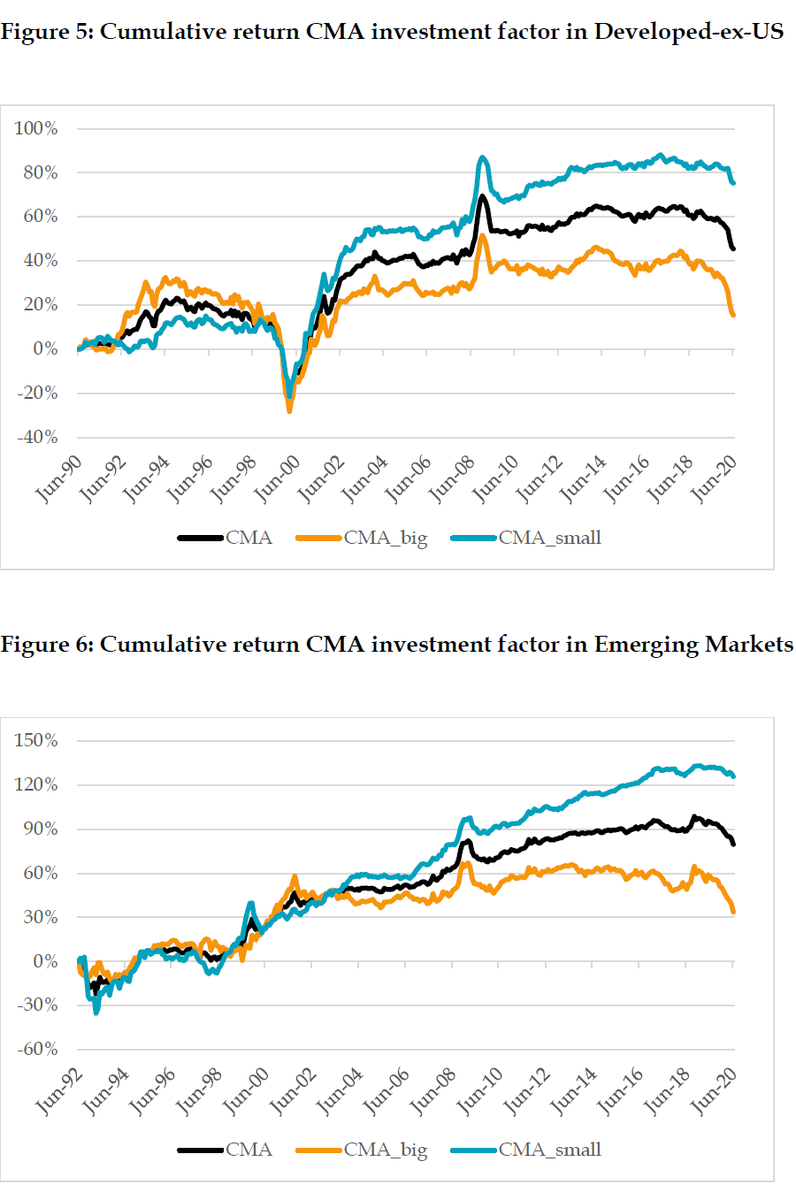

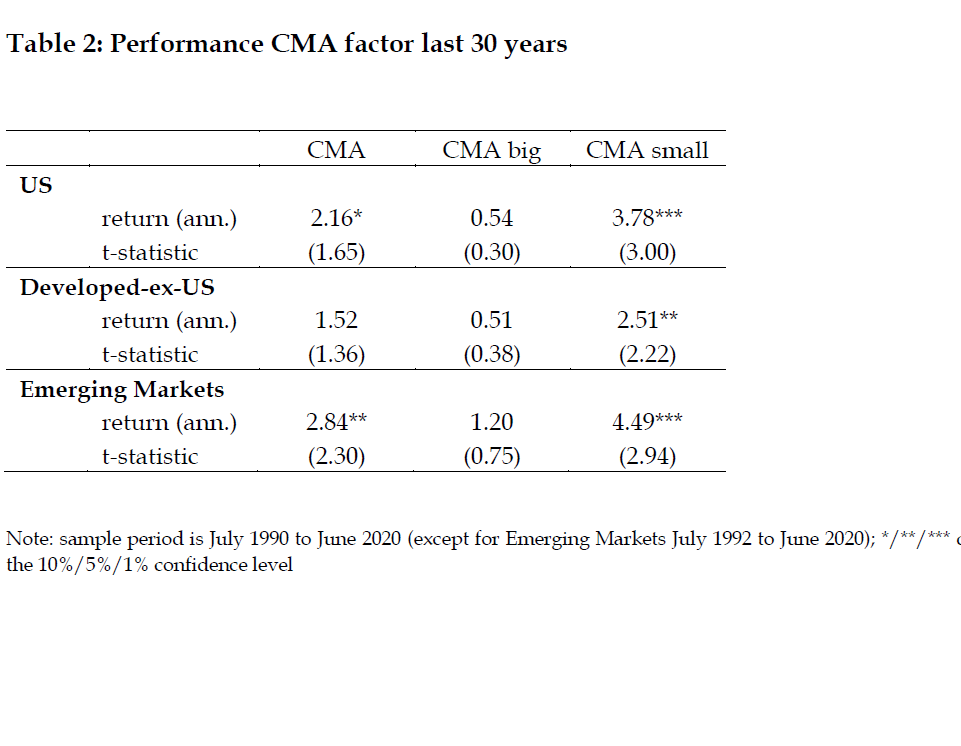

4/ "CMA has not been much better than HML over the last thirty years.

"This is all the more remarkable, since the factor stems from the Fama and French (2015) study that uses data until December 2013: i.e. our sample is still mostly the in-sample period for this new factor."

"This is all the more remarkable, since the factor stems from the Fama and French (2015) study that uses data until December 2013: i.e. our sample is still mostly the in-sample period for this new factor."

5/ "We use a broader set of metrics [EBITDA/EV, CF/P, net payout yield, B/M adjusted by capitalizing R&D expenses), apply basic risk management, and make more efficient use of the breadth offered by large caps.

"Portfolios are rebalanced monthly. Returns are total USD returns."

"Portfolios are rebalanced monthly. Returns are total USD returns."

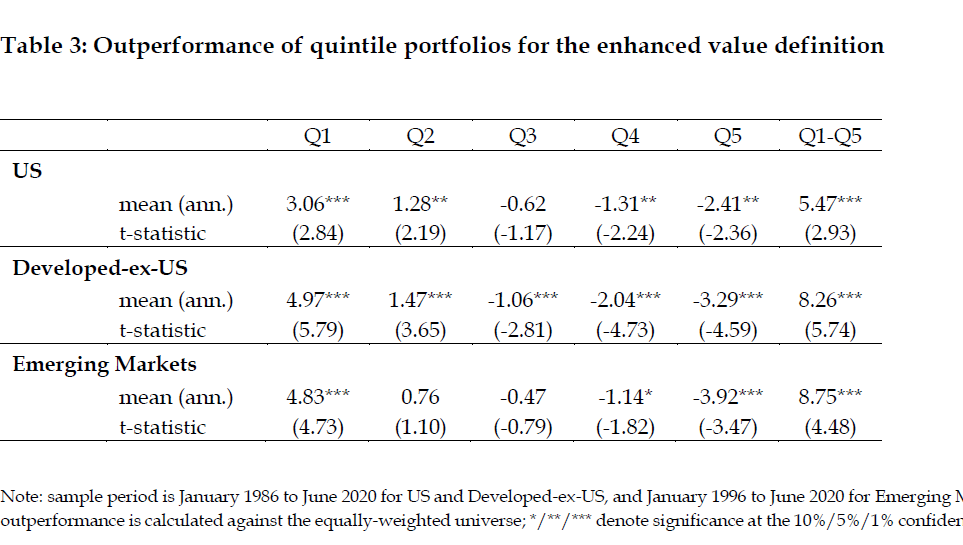

6/ "T-statistics are highly significant. For each region, the top and bottom quintiles contribute jointly to the value premium and are both highly significant, implying that the premium is not critically dependent on the short side where limits to arbitrage are most prevalent."

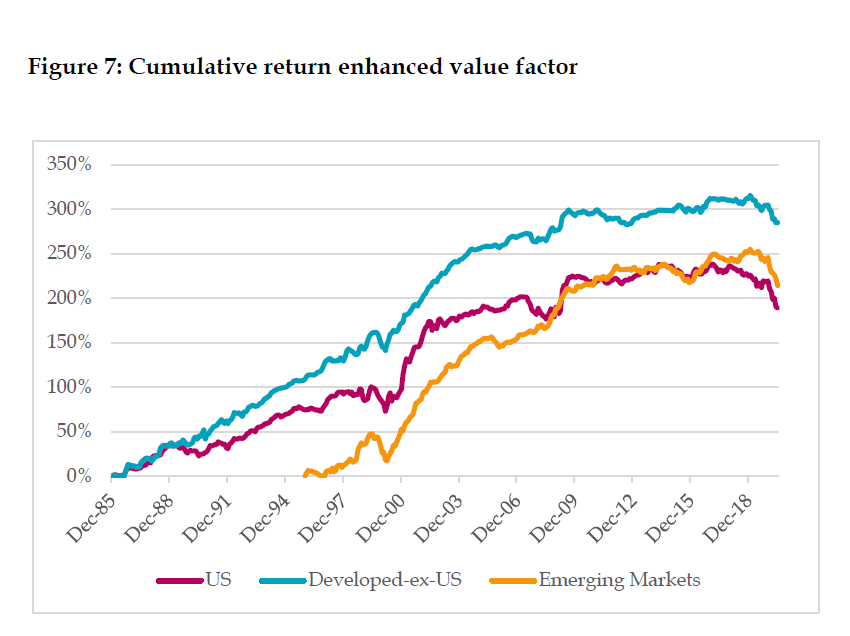

7/ "Whereas existential concerns are understandable for HML, they do not appear justified for the enhanced value strategy. In other words, if we move beyond the generic academic definition of value, a solid premium is still clearly present in the cross-section of stock returns."

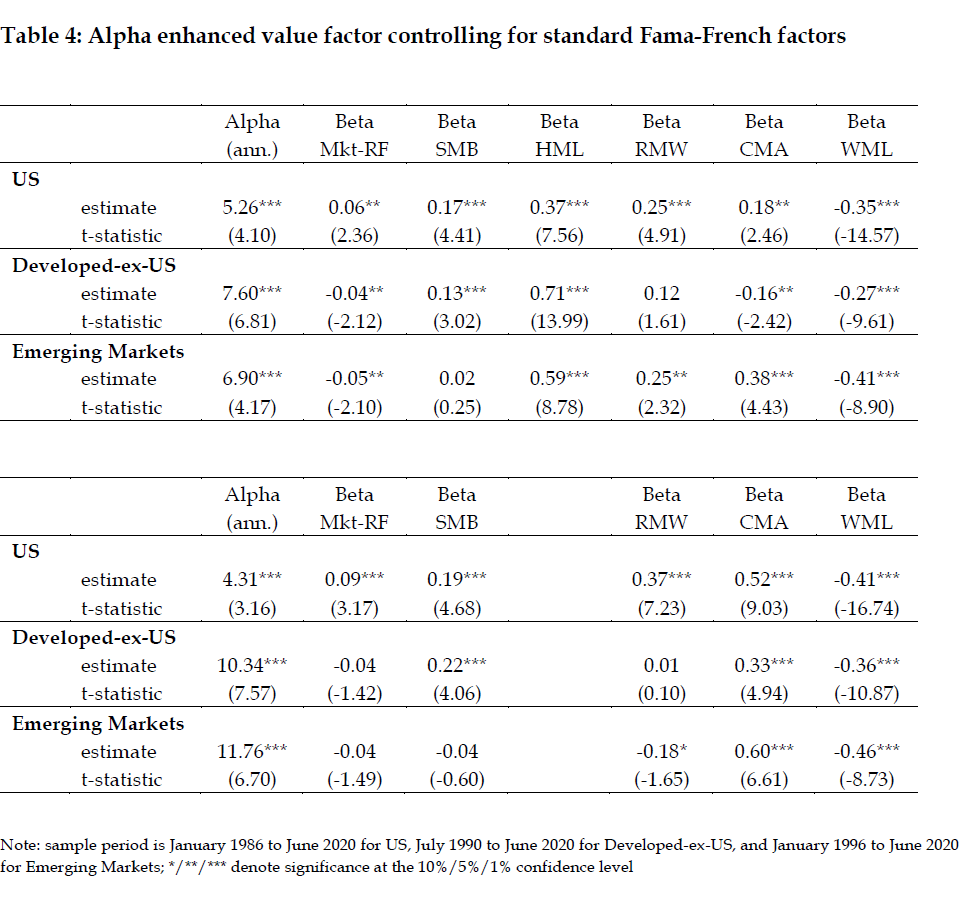

8/ "After adjusting for other factors, we obtain highly significant alphas that are roughly in the 5-8% range: close to the raw return levels.

"Unlike HML, our enhanced value factor is not subsumed by the non-value factors (and so does indeed resurrect the value premium)."

"Unlike HML, our enhanced value factor is not subsumed by the non-value factors (and so does indeed resurrect the value premium)."

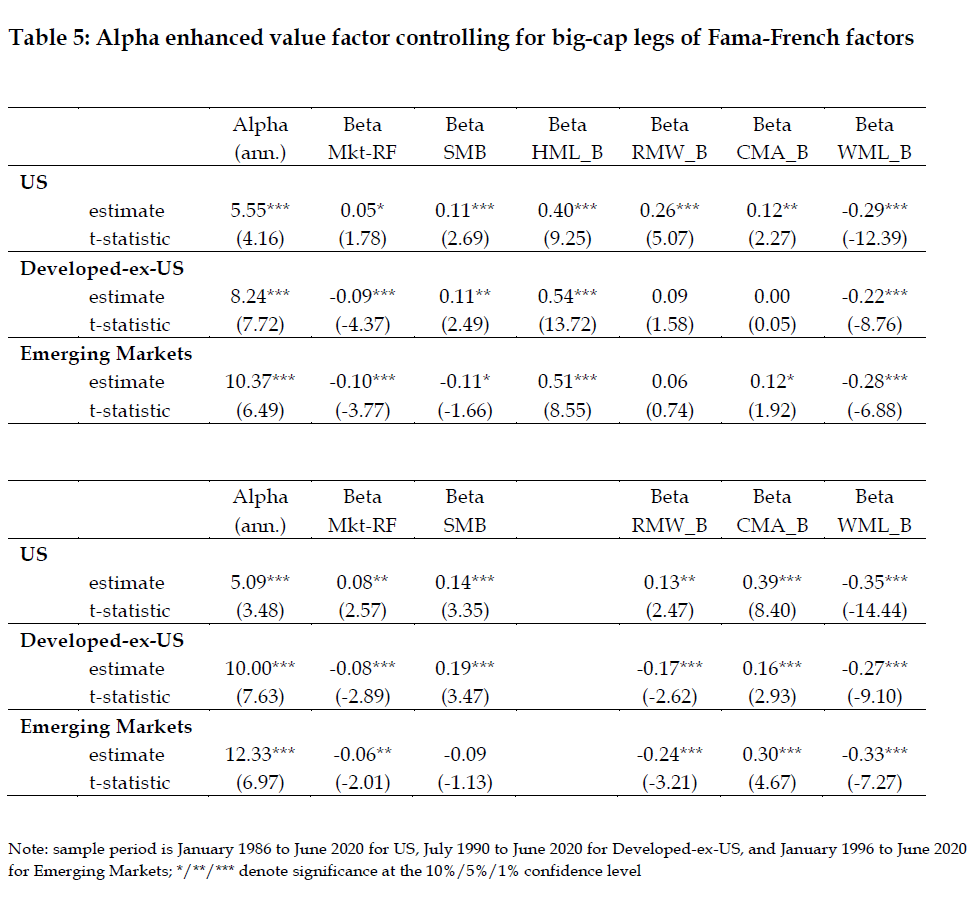

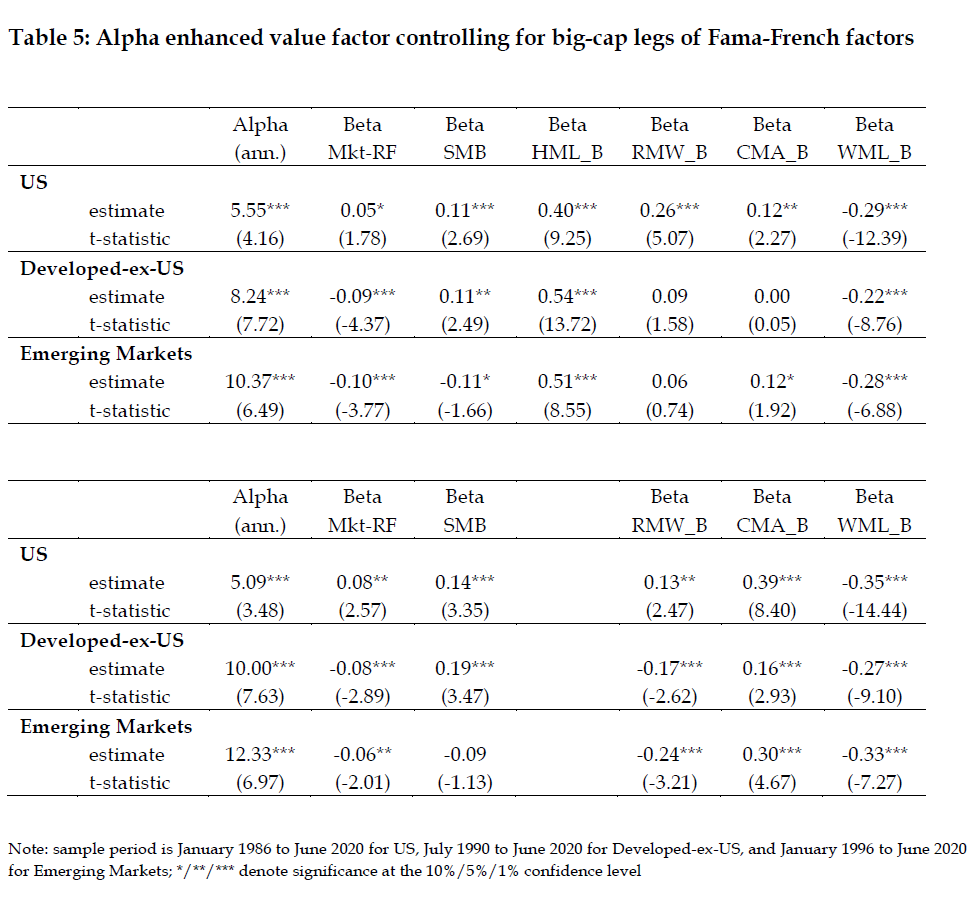

9/ "Findings are robust to using the big-cap versions of the Fama-French factors.

"Alpha increases (from lower premia on factors to which the enhanced value strategy is positively exposed) are largely offset by alpha decreases (from a lower premium on the momentum factor)."

"Alpha increases (from lower premia on factors to which the enhanced value strategy is positively exposed) are largely offset by alpha decreases (from a lower premium on the momentum factor)."

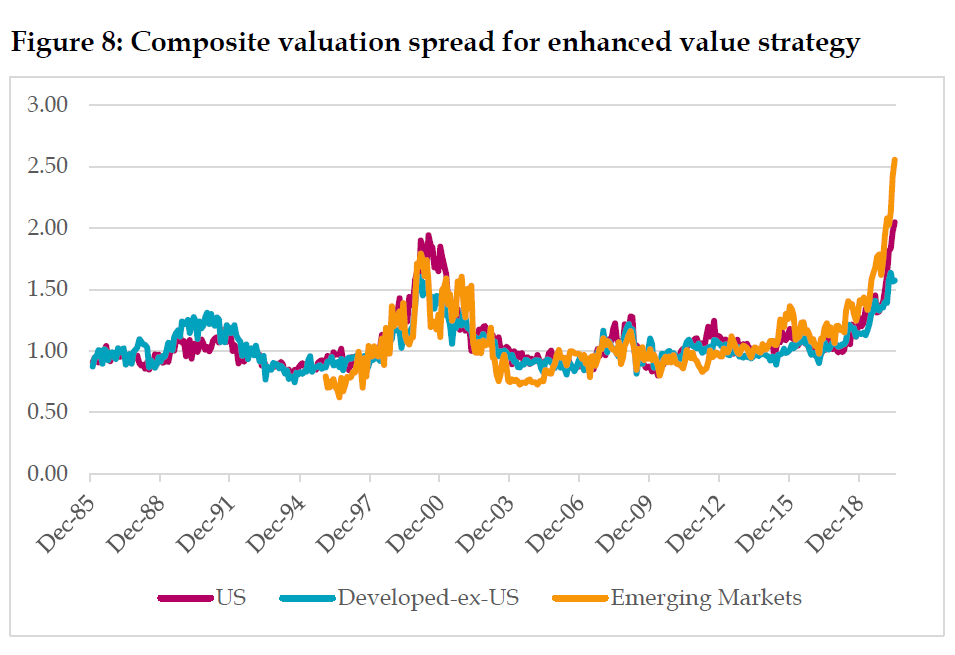

10/ "The net value spread widening that occurred over our sample period means returns over this period might underestimate the ‘true’ magnitude of the value premium.

The increasing spread is "inconsistent with the concern that the value premium may have been arbitraged away."

The increasing spread is "inconsistent with the concern that the value premium may have been arbitraged away."

11/ "Similar to the classic HML factor, our enhanced value factor remains a theoretical construct that ignores various practical limits to arbitrage that investors face in reality, such as transaction costs, shorting costs, taxes, and long-only constraints."

12/ Related research:

Is (Systematic) Value Investing Dead?

Will value survive its long winter?

Fact, Fiction, and Value Investing

Factor Performance 2010-2019: A Lost Decade?

Is (Systematic) Value Investing Dead?

https://twitter.com/ReformedTrader/status/1259165422412128259

Will value survive its long winter?

https://twitter.com/ReformedTrader/status/1304557723392962561

Fact, Fiction, and Value Investing

https://twitter.com/ReformedTrader/status/1117084235318190087

Factor Performance 2010-2019: A Lost Decade?

https://twitter.com/ReformedTrader/status/1245559396714729473

• • •

Missing some Tweet in this thread? You can try to

force a refresh