The rapid deterioration in macro/financial conditions will put a great deal of pressure on the ECB on Thursday.

How can they hint at an increase in asset purchases without saying it? What else could @Lagarde say or do? (1/n)

How can they hint at an increase in asset purchases without saying it? What else could @Lagarde say or do? (1/n)

Even before the second virus wave hit, there was little doubt that the ECB would need to ease again by year-end, based on the PEPP's dual function, Philip Lane's “two-stage approach” and Fabio Panetta’s “asymmetric reaction”. (2/n)

The ECB will likely postpone a decision to December based on the updated/extented staff projections, aiming at a broader consensus. But now that downside risks are materialising, @Lagarde needs to do more than just “send a signal” to markets on Thursday. (3/n)

First, the ECB can "task the relevant committees" to look into the various policy options available (APP/PEPP; TLTRO; DFR; tiering). The usual trick, though unlikely to save the day. (4/n)

Second, @Lagarde can do a "Sintra 2019", reversing the burden of proof by saying that "in the absence of improvement in the outlook [December staff projections], additional stimulus will be required". (5/n) ecb.europa.eu/press/key/date…

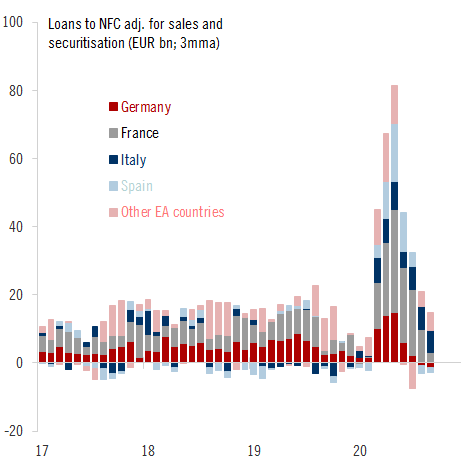

Third, @Lagarde can signal a pick-up in the pace of asset purchases, e.g. weekly PEPP accelerating from €15bn to €20-25bn until a formal decision is made about the total envelope. (6/n)

Fourth, the ECB can ease TLTRO-III funding conditions now, including by extending the discount period during which the minimum interest rate of -1% is applied (currently between June 2020 and June 2021), by 6 to 12 months. (7/n)

A longer TLTRO discount period (and/or a larger discount, i.e. lower dual rate) would encourage a larger take-up at the December operation (banks to submit bids by 9 Dec) while signalling a longer horizon during which the ECB is willing to provide emergency support. (8/n)

Fifth, the ECB can close the door to a rate cut a little further. A recent study shows that QE is more efficient in easing financial conditions, including FX. The QE boost could be even larger. The banking sector would welcome it, too. (9/n)

The longer the ECB waits, the easier it might be to sell a package to the hawks as the data deteriorate. The longer the ECB waits, the greater the risk to financial conditions and to its credibility. @Lagarde needs to strike a delicate balance but the pressure is mounting. (10/n)

Ideally, we should not have to wait until the ECB publishes a blog on Friday for the message to be received, loud and clear. (11/11)

• • •

Missing some Tweet in this thread? You can try to

force a refresh