Personal Income:

Interesting trends under the surface of the "surprise" increase in income for September.

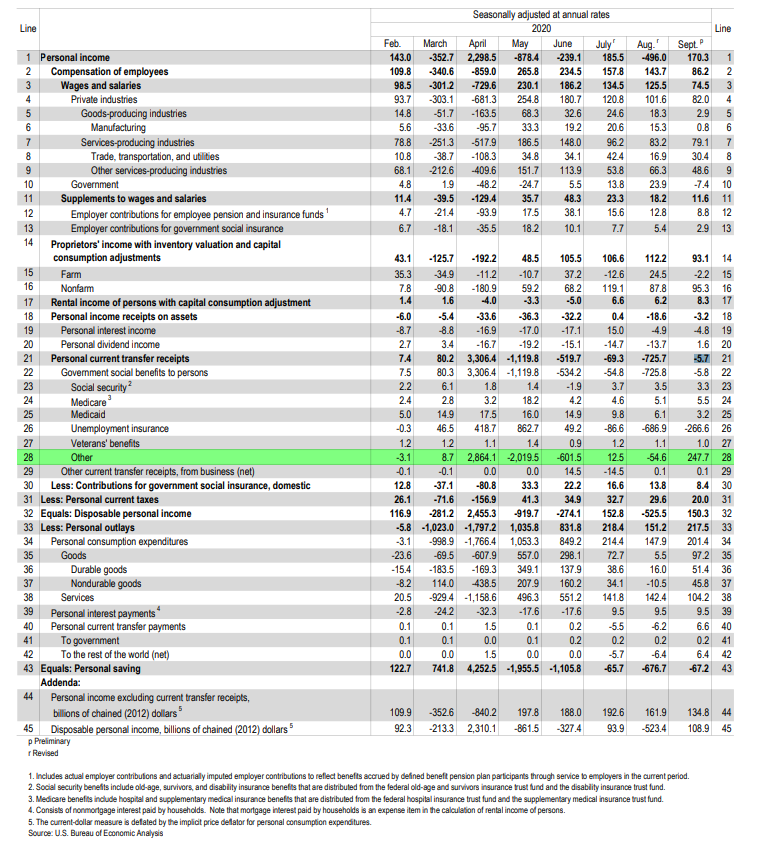

The compensation of employees increased $86B, the smallest increase in five months.

The last five months increase (billions):

$265 > $234 > $157 > $143 > $86

Interesting trends under the surface of the "surprise" increase in income for September.

The compensation of employees increased $86B, the smallest increase in five months.

The last five months increase (billions):

$265 > $234 > $157 > $143 > $86

Government transfer payments declined just $5.7 billion.

Last month the decline in transfer payments was ($725) billion.

The delta came from the "other" category of transfer payments.

Last five months of "other":

-$2,019 > -$601 > +$12.5 > -$54.6 > +$247

Last month the decline in transfer payments was ($725) billion.

The delta came from the "other" category of transfer payments.

Last five months of "other":

-$2,019 > -$601 > +$12.5 > -$54.6 > +$247

"Other" was boosted by "Lost Wages Supplemental Payments"

Monthly change in wages and salaries:

• • •

Missing some Tweet in this thread? You can try to

force a refresh