I was asked to comment on this. So comments follow.

There is more to this thread above.

Please forgive typos. Happy to have feedback/discuss.

There is more to this thread above.

Please forgive typos. Happy to have feedback/discuss.

https://twitter.com/chamath/status/1326234320080531456

This is obviously just one person's comment.

YAFIYGI , WYSIWYG, YMMV, TAR33SIB, and ILCWWR

YAFIYGI , WYSIWYG, YMMV, TAR33SIB, and ILCWWR

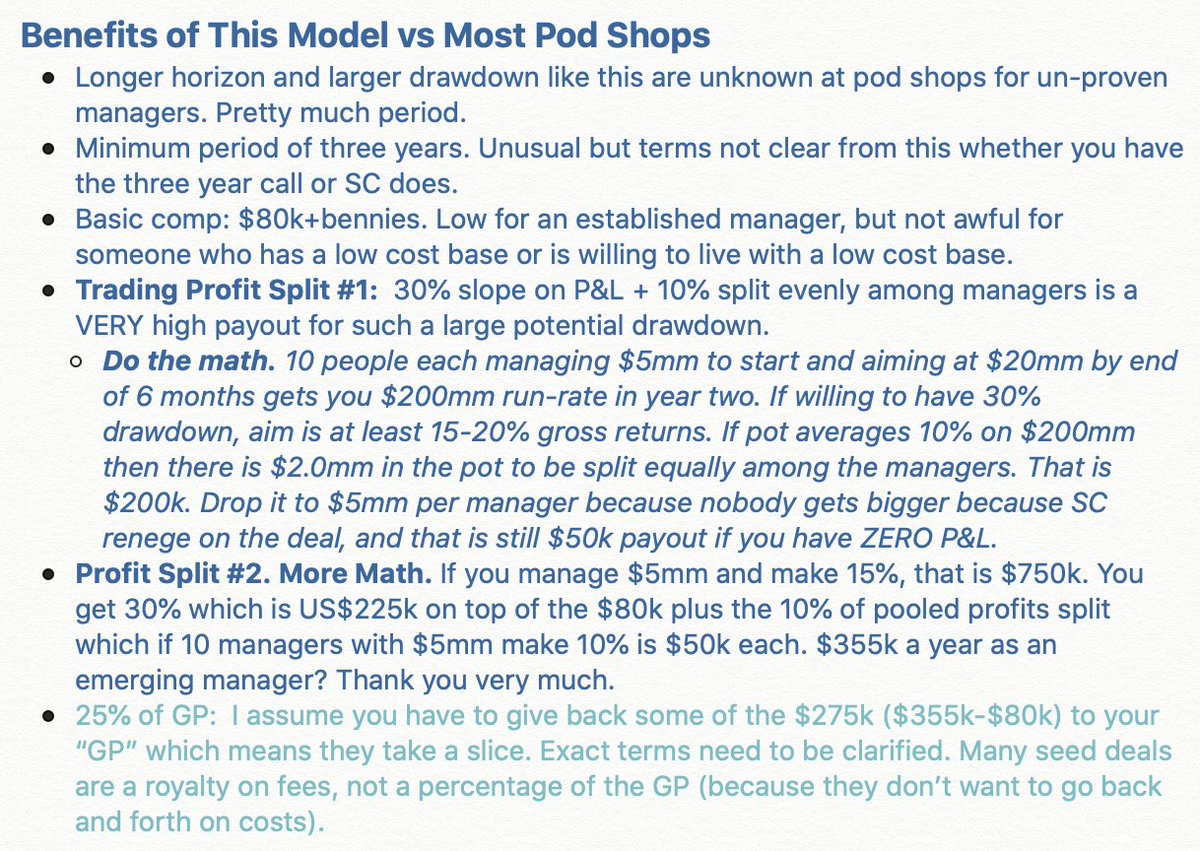

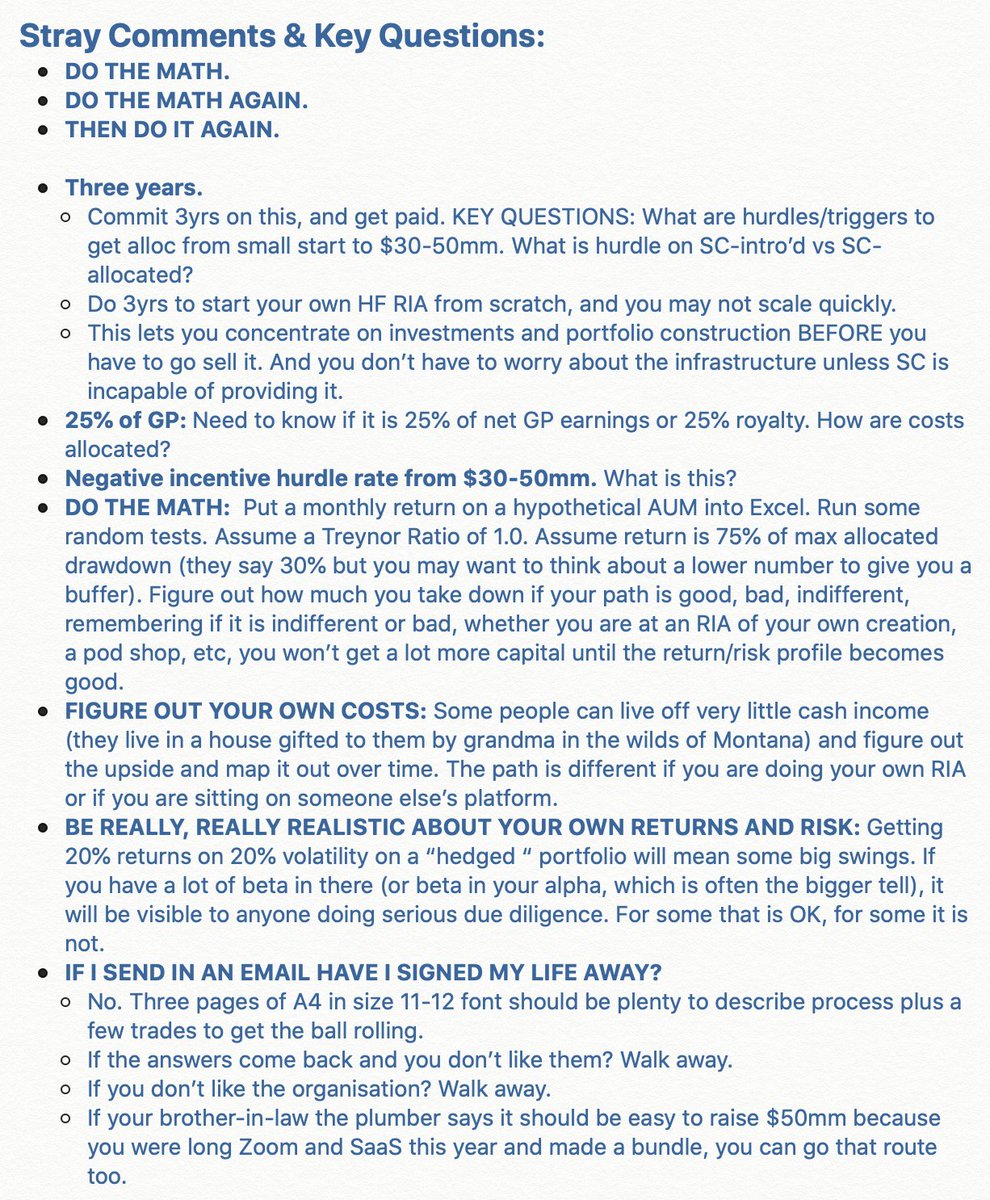

Apols if not clear. "That is still $50k payout if you have ZERO P&L" means that if the pool makes that money and you don't, you still end up with a share of the pool payout. The 30% payout obviously is a coefficient multiplied against zero.

To caveat all of this, I know nothing of Social Capital and anyone getting in bed with them would have to do their work on that angle.

And with such weakly-defined Ts & Cs here, one does not know nearly enough to commit to anything.

And with such weakly-defined Ts & Cs here, one does not know nearly enough to commit to anything.

• • •

Missing some Tweet in this thread? You can try to

force a refresh