The good news is that the rate in which employed workers are going directly into *permanent* layoff has fallen, though is still elevated [left].

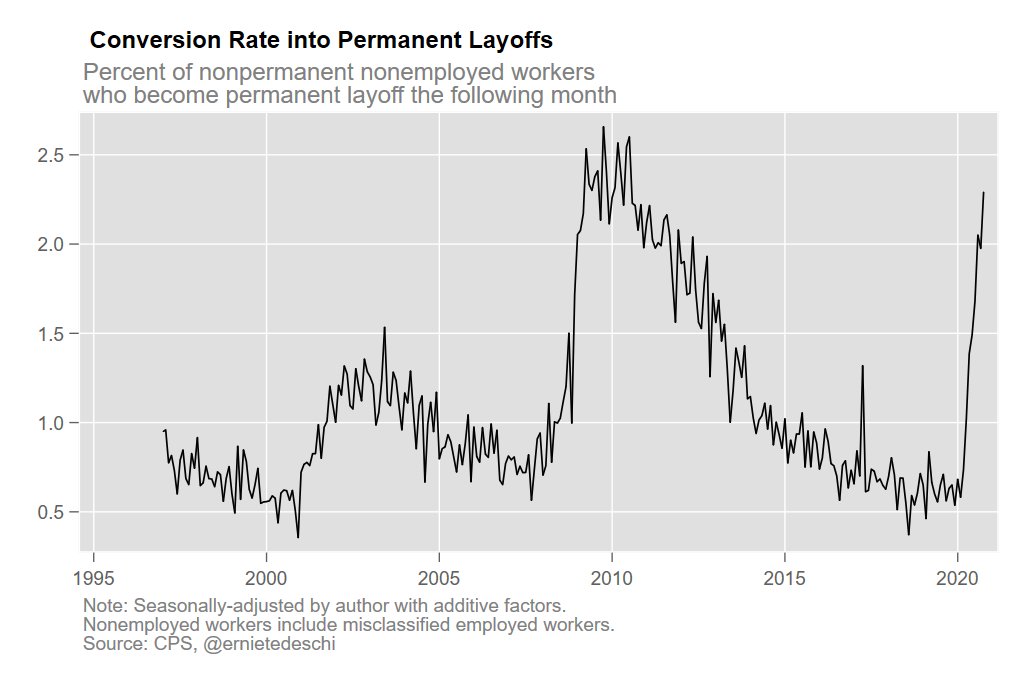

The bad news is that the rate at which already-nonemployed workers are *becoming* permanent layoffs is high and rising [right].

The bad news is that the rate at which already-nonemployed workers are *becoming* permanent layoffs is high and rising [right].

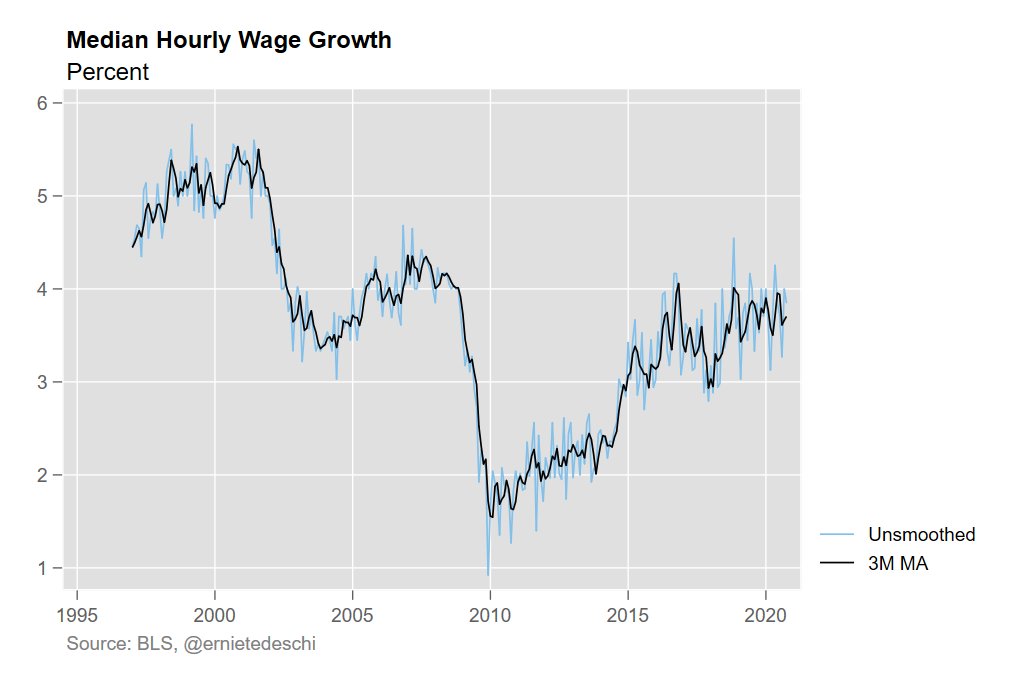

Meanwhile, hourly wage growth among workers keeping their jobs is stable [L], but weekly wage growth has fallen [R], a sign that employed workers are getting fewer hours.

And a rising share of workers aren't seeing any nominal wage growth at all.

• • •

Missing some Tweet in this thread? You can try to

force a refresh