1/ Here is a public version of Lux's Q3 Letter to LPs

"Do Good Things"...

medium.com/lux-capital/do…

"Do Good Things"...

medium.com/lux-capital/do…

2/ In preview, we hold the minority view that this moment in time is not––

in the context of all that has ever happened and all yet to happen

––uniquely special, even with all the evident chaos...

in the context of all that has ever happened and all yet to happen

––uniquely special, even with all the evident chaos...

3/ Instead there are directional arrows of positive progress, technological inevitabilities, more + new options created by agency + ambition of scientific + technical founders we FUND

From any moment in the present, they are always setting up a perpetually more promising FUTURE

From any moment in the present, they are always setting up a perpetually more promising FUTURE

4/ But isn’t this time different?

The phrase “historic moment” is used by journalists 100 times a month, on average three times daily. Authors and anchors assert this moment, right now, is the most critical moment in history...

The phrase “historic moment” is used by journalists 100 times a month, on average three times daily. Authors and anchors assert this moment, right now, is the most critical moment in history...

5/... It’s only in hindsight that historians ascribe meaning of import to things of the PAST

We say when investing that 100% of the information we have is based on the past and 100% of the value of the decisions we make is in the FUTURE

which is inherently probabilistic.

We say when investing that 100% of the information we have is based on the past and 100% of the value of the decisions we make is in the FUTURE

which is inherently probabilistic.

6/ Part of the reason we say “never forget” is because we often do. Even the scarring moments of 9/11 or '08 crisis risk fading from recent memory — especially in the younger minds unburdened with the visceral experience of either....

7/ It seems more than provocative to note that the pandemic will have killed more people in the U.S. than all military conflicts over the past 70 years.

Do we believe in a decade it will have been the most defining and important moment in our history?

Do we believe in a decade it will have been the most defining and important moment in our history?

8/ The hustlers acting with the urgent impatience of NOW

need the waiters to provide the patient capital of LATER

Urgency most often comes from the young and the restless...

need the waiters to provide the patient capital of LATER

Urgency most often comes from the young and the restless...

9/ Thus the truth is: the future lies mostly with those who rebel against tradition (and often their older predecessors) and seize the PRESENT over POSTERITY — until yet younger yearn to do the very same.

10/ Perspective depends on distance.

Now at Lux, we are UNCOMFORTABLY optimistic, near-term comfortably cautious and long-term conditionally certain.

...The reason is thus: the less-than-usual things that Lux seek to fund now have more-than-usual demand.

Now at Lux, we are UNCOMFORTABLY optimistic, near-term comfortably cautious and long-term conditionally certain.

...The reason is thus: the less-than-usual things that Lux seek to fund now have more-than-usual demand.

11/ The cause for our optimism is the ENDOGENOUS — fundamentals we can + have influenced:

recruiting top talent: execs, engineers, BoD

introducing cornerstone customers

constructing strong syndicates of follow-on investors

advising on competitive positioning + strategy...

recruiting top talent: execs, engineers, BoD

introducing cornerstone customers

constructing strong syndicates of follow-on investors

advising on competitive positioning + strategy...

12/ Many Lux co's have seen record quarter growth. Including Aeva, @anduriltech @AvailMedsystems , @AppliedInt @Matterport @latchaccess @RecursionPharma @Science37x Subspace have not only not skipped a BEAT, they’ve turned up the TEMPO...

13/ The cause for our uncomfortable optimism is the EXOGENOUS —

the outside mood and movement of markets independent of anything we may do or have done and over which we have little to NO influence...

the outside mood and movement of markets independent of anything we may do or have done and over which we have little to NO influence...

14/ The TRUTH is this:

we do not know if this current zeitgeist zigs, zags or zeroes out in 2 days, 2 weeks, 2 months or 2 years.

We do know how to make a case for it lasting longer than it should — or ending earlier than it could.

we do not know if this current zeitgeist zigs, zags or zeroes out in 2 days, 2 weeks, 2 months or 2 years.

We do know how to make a case for it lasting longer than it should — or ending earlier than it could.

15/ EXCERPT:

"...The Case of it Ending Earlier Than it Could...

Let’s start with the latter. Failure comes from a failure to imagine failure. So let’s posit and dispense with the case for this optimism ending earlier than it could, or seeing reversal:

"...The Case of it Ending Earlier Than it Could...

Let’s start with the latter. Failure comes from a failure to imagine failure. So let’s posit and dispense with the case for this optimism ending earlier than it could, or seeing reversal:

16/ EXCERPT:

"The Case for it Lasting Longer than it SHOULD.."

...rests also on low rates, high expectations for equities and relative unattractiveness of fixed income, rising confidence and animal spirits, growing participation from individual investors...

"The Case for it Lasting Longer than it SHOULD.."

...rests also on low rates, high expectations for equities and relative unattractiveness of fixed income, rising confidence and animal spirits, growing participation from individual investors...

17/ In the late 1980’s, Michael Milken @ Drexel, through a combo of academic + portfolio theory, turned a backwater undesired asset, the “junk bond”, into a legitimized coveted capital tool of “high yield” to unlock entrepreneurial creativity, growth and create enormous wealth...

18/ With rates at 0, investors are applying little discount to terminal values — a dollar in 2025 is given nearly full credit today — lending logic to valuations that would have otherwise seemed high by historical standards...

19/ It may not be zero-sum but game theory will push more co's to seek the cash + stock currency — both of which create optionality for strategic maneuvering. A Lux co that goes public earlier than its competitors may be rewarded with a large warchest of cash + stock currency...

20/ ... from which it can afford tuck-in acquisitions to lock in talent, technology, product pipeline, customers and market share.

21/ BUT...

the sheer volume of vehicles seeking targets and the risk of not finding a partner and turning into a pumpkin before the clock runs out will also create an abundance of low-quality acquisitions — companies that really shouldn’t be public.

the sheer volume of vehicles seeking targets and the risk of not finding a partner and turning into a pumpkin before the clock runs out will also create an abundance of low-quality acquisitions — companies that really shouldn’t be public.

22/ We have already seen companies get acquired on nothing more than a narrative and a video rendering, and at least one company already accused of fraud still trades at a nearly $7 billion market capitalization....

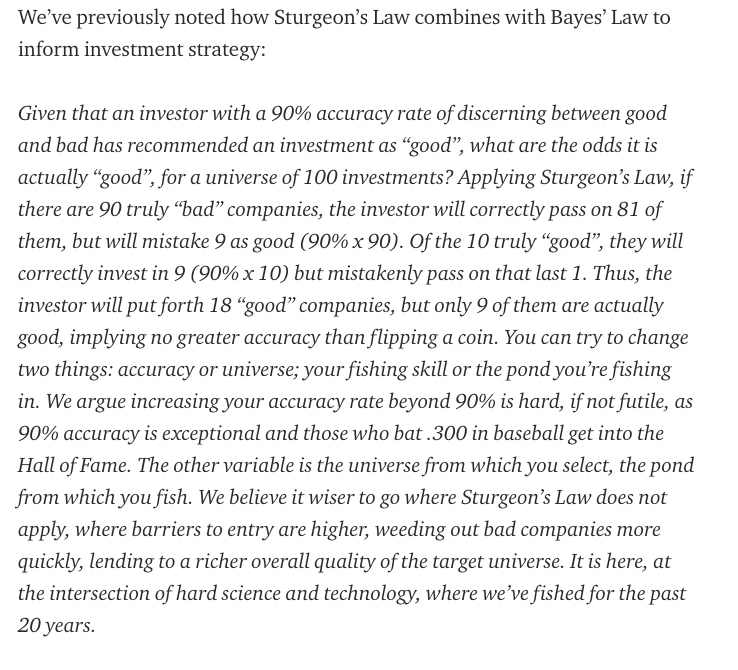

Beware of Sturgeon's Law as applied to SPACs!

Beware of Sturgeon's Law as applied to SPACs!

23/ Combine Sturgeon's Law + Bayes Theorem...

And it informs where you ought to look as an investor.

And it informs where you ought to look as an investor.

24/ There is also a VERY good chance of an M&A boom, if not an M&A craze.

There is a good chance the incumbents find themselves competing with already public companies with higher multiples as well as SPACs seeking targets.

*WATCH OUT for imminent AOL/TimeWarner-like mergers.

There is a good chance the incumbents find themselves competing with already public companies with higher multiples as well as SPACs seeking targets.

*WATCH OUT for imminent AOL/TimeWarner-like mergers.

25/ Remember: Stockdale's Paradox.

NEVER confuse the necessary belief that you’ll prevail in the end––with the discipline to confront the most brutal facts of current REALITY, whatever they may be...

NEVER confuse the necessary belief that you’ll prevail in the end––with the discipline to confront the most brutal facts of current REALITY, whatever they may be...

26/ A growing list of RISKS nobody is paying attention to as politics + covid monopolize your ATTENTION.

From corporate bond defaults to emerging geopolitical crisis to countries on the cusp of contagious war...

It may be wise to be LONG entropy + ventures that help in chaos.

From corporate bond defaults to emerging geopolitical crisis to countries on the cusp of contagious war...

It may be wise to be LONG entropy + ventures that help in chaos.

27/ There are power laws found from ecosystems to economies of cities as described by @sfiscience

And asymmetries in the time it takes to BUILD or BREAK something.

"..True of toys and towers, bridges and buildings, tree branches and trust..."

And asymmetries in the time it takes to BUILD or BREAK something.

"..True of toys and towers, bridges and buildings, tree branches and trust..."

28/ When a material in a built structure loses “INTEGRITY” it can collapse quickly. So too for immaterial social structures: from global international order to markets, economies + flowing commerce — all based upon coordination +common shared reality, expectations, relationships

29/ Material structures lack memory––but people do.

An engineered building holds no grudges, doesn’t reason with game theory + seeks neither reciprocity nor retribution

It’s why the bonds that bind us make trust the most valuable currency — especially amid abundant conflict.

An engineered building holds no grudges, doesn’t reason with game theory + seeks neither reciprocity nor retribution

It’s why the bonds that bind us make trust the most valuable currency — especially amid abundant conflict.

• • •

Missing some Tweet in this thread? You can try to

force a refresh