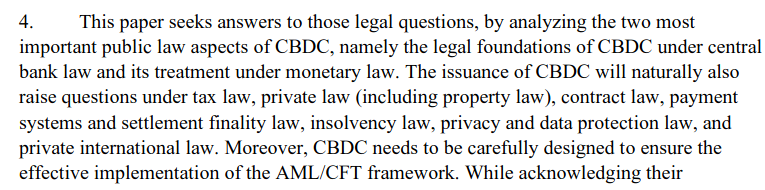

A brief (critical) thread on the new IMF paper on the law of CBDC:

imf.org/en/Publication…

1. From the outset, it commits original sin of CBDC discourse: naturalizing the CB as the sole monetary institution of relevance to the analysis. Where is Tsy?

imf.org/en/Publication…

1. From the outset, it commits original sin of CBDC discourse: naturalizing the CB as the sole monetary institution of relevance to the analysis. Where is Tsy?

The paper is structured around the premise that CBs are the only govt entities responsible for public money. There is only one reference to Tsy's money power in the whole paper, & it is buried in a footnote, where they begrudgingly acknowledge this premise is not, in fact, true.

2. The paper also displays its bias from the outset - asserting, without justification, that digital public currency *must* be designed in compliance with existing AML/CFT laws. If you were hoping for a more balanced analysis of privacy/law enforcement tensions, look elsewhere.

3. The paper does a good job - especially relative to other CB reports out there - distinguishing between account and token based digital currencies, being careful not to reduce the latter solely to a distributed-ledger/blockchain model.

4. This paper is to be commended for asking legal questions so many others have failed to ask in the growing CBDC/DFC literature, but actual legal analysis itself is wanting. For ex, it argues 'banknotes & coins' should be given plain reading but assumes that excludes digital.

But there's no reason to presume that the plain reading of a term like 'coin', absent further qualifications, must necessarily exclude virtual coins, unless you're an originalist. Today, plenty of 'coins' exist that aren't stamped on metal. These laws can and should reflect that.

The paper notes this possibility in the context of interpreting tokens as digital banknotes, but then just asserts it "might be a stretched legal interpretation" and moves on. And the legal definition of coins isn't even discussed other than to say it must be 'metallic'.

5. The paper also discusses "currency" at length, but waivers between defining it as a functional term referring to instruments whose ownership is based on possession (ie currency as 'current', see Fox: jstor.org/stable/4508252…), and a formal term meaning 'coins and notes'.

6. The confusion is exacerbated by a false dichotomy between 'ownership by possession' & 'ownership by knowledge of password'. In fact, these are not mutually exclusive or tech-specific-digital/physical currency ownership can be established by either or both depending on design.

The paper actually acknowledges this point when discussing validation of transfer, but then forgets it again when considering the scope of the legal definition of 'currency'.

7. I agree with the paper's overall recommendation for explicit legislation to clarify many of these issues and give digital public currency issuers a clear and intentional mandate and framework. However, yet again, privacy is treated as an afterthought, "someone else's problem".

This is problematic, especially when viewed in conjunction with the paper's initial deference to existing AML/CFT law compliance. The effect is, once again, to pay lip service to privacy issues without actually grappling with what would be needed to address those issues properly.

8. The paper should also be commended for giving proper treatment and consideration to the principle of nominalism, which undergirds contemporary monetary law and is widely misunderstood by those in the digital currency space.

9. Unfortunately, however, its treatment of the concept of monetary sovereignty is less strong, conflating legal tender status with tax-receivability when the two are, conceptually and historically, not the same.

10. Additionally, their claim that banknotes cannot pay interest is simply not true, & belied by various forms of 'stamped money' where interest is added ex-post upon tendering to an authority in the right way, something also easily possible with digital bearer instruments.

11. Finally, the claim, repeated multiple times, that a digital token would be difficult to establish as legal tender due to the fact many people might face difficult accepting is not persuasive, as it is equally true today of both physical currency and account-money.

12. Overall, this is a great contribution to the ongoing law of digital currency literature, even as I find it limited and problematic in different areas. It pushes the conversation forward significantly and has a bunch of fantastic information, analysis, and resources.

@Kiffmeister, @jerrybrito, @NathanTankus, @MorganRicks1, @MehrsaBaradaran, @chastitycmurphy, @RaulACarrillo, @STOmarova, @Suitpossum, @dgwbirch, @dandolfa, @moneyontheleft, @DavidBeckworth, @johndhaskell, @angela_walch

• • •

Missing some Tweet in this thread? You can try to

force a refresh