1/ Bubbles for Fama (Greenwood, Shleifer, You)

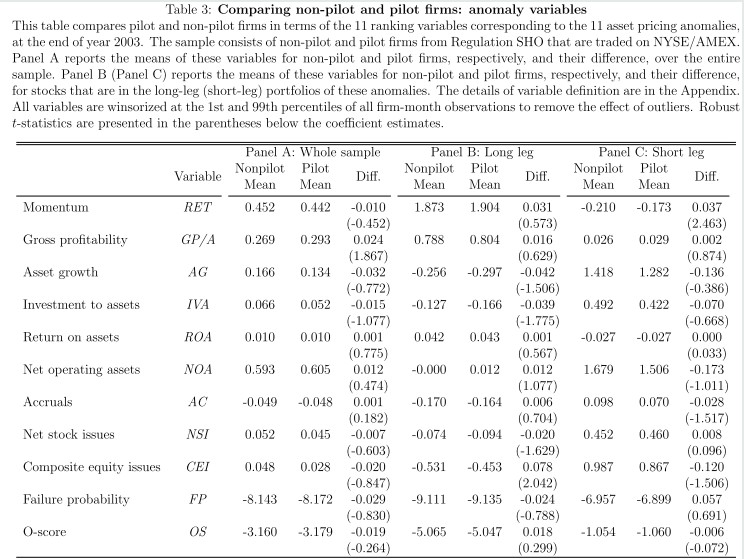

"A sharp price increase of an industry portfolio does not, on average, predict unusually low returns going forward, but such sharp price increases predict a substantially heightened probability of a crash."

papers.ssrn.com/sol3/papers.cf…

"A sharp price increase of an industry portfolio does not, on average, predict unusually low returns going forward, but such sharp price increases predict a substantially heightened probability of a crash."

papers.ssrn.com/sol3/papers.cf…

2/ "On average, industries that experienced a price run-up continue to go up by 7% over the next year (5% net of market) and 0% over the next two years (0% net of market).

"An *industry* run-up is also associated with poor average subsequent *market* returns."

"An *industry* run-up is also associated with poor average subsequent *market* returns."

3/ "If we study only cases in which a crash occurs, the average return experienced between the initial run-up and subsequent peak is 30% (107% for precious metal stocks in the late 1970s). It is difficult to bet against a bubble, even if one has correctly identified it ex-ante."

4/ "The international data is not a fully independent test. However, even in episodes that are shared across industries in different countries, the timing of the boom and bust varies substantially.

"Our conclusion about average returns also holds in the international data."

"Our conclusion about average returns also holds in the international data."

5/ "How sensitive is our conclusion about average returns to the 100% past return cutoff?

"Our earlier conclusion that Fama is correct about average returns must be substantially tempered: excess returns in the two years subsequent to very high past returns are negative."

"Our earlier conclusion that Fama is correct about average returns must be substantially tempered: excess returns in the two years subsequent to very high past returns are negative."

6/ "The probability of a crash is strongly associated with high past returns.

"Controlling for lagged industry volatility slightly attenuates the coefficient on past returns, but the effect is modest."

"Controlling for lagged industry volatility slightly attenuates the coefficient on past returns, but the effect is modest."

7/ "Crashes are more predictable than returns.

"There is considerable heterogeneity between episodes in how long it takes before the crash starts. Not surprisingly, average returns are much lower for the episodes in which the crash comes sooner."

"There is considerable heterogeneity between episodes in how long it takes before the crash starts. Not surprisingly, average returns are much lower for the episodes in which the crash comes sooner."

8/ "Below, we present results based on cross-sectional industry comparisons. (Volatility, age, turnover, sales growth are based on percentile ranks.)

"Volatility and turnover tend to be elevated during the price run-ups that subsequently crash compared to run-ups that do not."

"Volatility and turnover tend to be elevated during the price run-ups that subsequently crash compared to run-ups that do not."

9/ "Price run-ups experiencing increases in volatility, involving younger firms, higher returns among the younger firms, and accelerating faster and in periods of overall good stock market performance, are all more likely to crash."

10/ "For the 107 price run-ups among international sector portfolios, across all the characteristics we consider, the results are broadly consistent, and in some cases statistically somewhat stronger, than our findings in the US, mainly driven by a larger number of observations."

11/ "Δvolatility, age tilt, issuance, book-to-market ratio, CAPE, and acceleration predict raw and excess returns.

"Only Δvolatility and age tilt successfully predict net-of-market returns, suggesting that an industry bubble is closely intertwined with overall market valuation."

"Only Δvolatility and age tilt successfully predict net-of-market returns, suggesting that an industry bubble is closely intertwined with overall market valuation."

12/ "A separate concern is the potential for data snooping.

"Panel A of Table 7 shows the false discovery tests that correspond to our prior results in Table 4 and Table 5.

"Panel B of Table 7 shows the false discovery tests applied to our regressions from Table 6."

"Panel A of Table 7 shows the false discovery tests that correspond to our prior results in Table 4 and Table 5.

"Panel B of Table 7 shows the false discovery tests applied to our regressions from Table 6."

13/ "Even for a run-up that will crash, the industry continues to perform well (on average) for another 6 months.

"Conditioning on both price increases and characteristics can help avoid crashes but at the cost of also exiting the market before large subsequent price increases."

"Conditioning on both price increases and characteristics can help avoid crashes but at the cost of also exiting the market before large subsequent price increases."

14/ Related research:

Industry Long-Term Return Reversal

Industry Long-Term Return Reversal

https://twitter.com/ReformedTrader/status/1116523225884708864

• • •

Missing some Tweet in this thread? You can try to

force a refresh