1/ Causal Effect of Limits to Arbitrage on Asset Pricing Anomalies (Chu, Hirshleifer, Ma)

"We examine the causal effect of limits to arbitrage using Regulation SHO, which relaxed short-sale constraints for a set of pilot stocks, as a natural experiment."

papers.ssrn.com/sol3/papers.cf…

"We examine the causal effect of limits to arbitrage using Regulation SHO, which relaxed short-sale constraints for a set of pilot stocks, as a natural experiment."

papers.ssrn.com/sol3/papers.cf…

2/ "Reg SHO removed the uptick rule and bid price test on randomly selected pilot stocks.

"The SEC then eliminated short-sale price tests for all exchange-listed stocks, so SHO effectively ran from 5/2/2005 to 7/6/2007."

11 anomalies: L/S decile portfolios, equally weighted

"The SEC then eliminated short-sale price tests for all exchange-listed stocks, so SHO effectively ran from 5/2/2005 to 7/6/2007."

11 anomalies: L/S decile portfolios, equally weighted

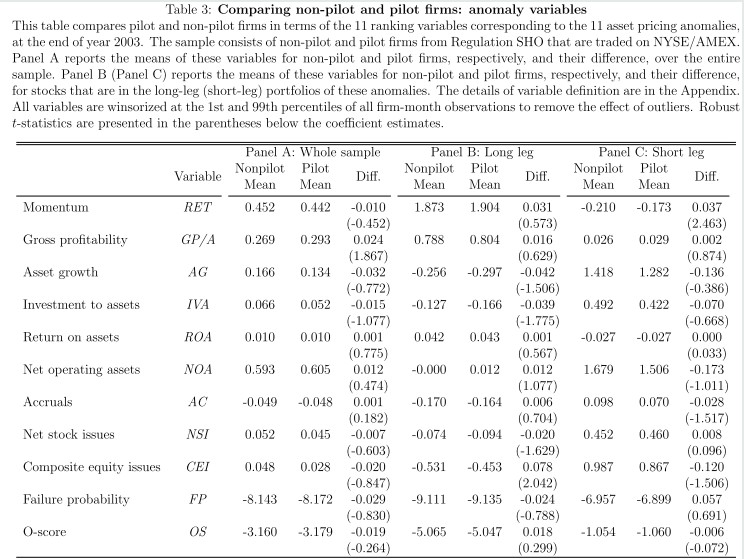

3/ "We confirm that the pilot firms were in fact randomly assigned with respect to firm characteristics associated with the 11 anomalies.

"Results suggest that there was no significant difference between pilot and non-pilot firms prior to the announcement of the pilot program."

"Results suggest that there was no significant difference between pilot and non-pilot firms prior to the announcement of the pilot program."

4/ "The pilot program reduced anomaly returns by 72 bps per month, on average.... the decreases are almost entirely from the short legs.

"Using benchmark-adjusted (CAPM- and FF3-adjusted) returns as the dependent variable delivers almost identical results as those in Table 4."

"Using benchmark-adjusted (CAPM- and FF3-adjusted) returns as the dependent variable delivers almost identical results as those in Table 4."

5/ "Our tests use a short (two-year) pilot period to estimate the effect of relaxing short-sale constraints.

"Observing the *difference* in anomaly strength between pilot versus non-pilot firms hedges away much of the factor volatility, increasing the test's precision."

"Observing the *difference* in anomaly strength between pilot versus non-pilot firms hedges away much of the factor volatility, increasing the test's precision."

6/ "As the difference in short-sale restrictions between pilot and non-pilot firms disappeared, the difference in anomaly returns between them also vanished.

"Easier arbitrage reduced anomaly returns for non-pilot stocks right after the end of Regulation SHO."

"Easier arbitrage reduced anomaly returns for non-pilot stocks right after the end of Regulation SHO."

7/ "There was a large initial price decrease on pilot short legs once the uptick rule was lifted: evidence that overpricing was reduced.

"The difference between pilot/non-pilot short-leg returns vanished in the post-pilot period, all stocks being exempted from the uptick rule."

"The difference between pilot/non-pilot short-leg returns vanished in the post-pilot period, all stocks being exempted from the uptick rule."

8/ "Pilot short-leg portfolios experienced more short selling once short-sale constraints were relaxed, consistent with our argument that the relaxation of short sale constraints reduces mispricing associated with the asset pricing anomalies."

9/ "We address the concern that the during-pilot period is shorter than the pre-pilot period.

Using shorter sample periods, "in aggregate, the β estimates are still statistically and economically significant for the short leg and the long-short portfolios."

Using shorter sample periods, "in aggregate, the β estimates are still statistically and economically significant for the short leg and the long-short portfolios."

10/ "None of these falsification tests generates results that are similar to our main results in Table 4.... This evidence further suggests that our main results are unlikely to have arisen by chance."

11/ "We expect a minimal effect of Regulation SHO on anomaly returns of Nasdaq-listed stocks.

"Results suggest little effect on anomaly returns for Nasdaq stocks and confirm that our main results derive from the relaxation of short-sale constraints generated by Regulation SHO."

"Results suggest little effect on anomaly returns for Nasdaq stocks and confirm that our main results derive from the relaxation of short-sale constraints generated by Regulation SHO."

12/ "The uptick rule impeded short selling more for small and less liquid stocks.... The effect of the pilot program on asset pricing anomalies is indeed more pronounced among small stocks.

"The results from subsample analysis split by liquidity are similar to those in Table 9."

"The results from subsample analysis split by liquidity are similar to those in Table 9."

13/ "The effect of the pilot program on asset pricing anomalies is indeed more pronounced among stocks that are more restricted by the uptick rule... further suggesting that the lift of the uptick rule is the underlying driving force of our main results."

14/ Related research:

Short-Selling Risk

When Equity Factors Drop Their Shorts

Equity Factors: To Short Or Not To Short

Shorting Costs and Profitability of Long–Short Strategies

Short-Selling Risk

https://twitter.com/ReformedTrader/status/1335084455023706113

When Equity Factors Drop Their Shorts

https://twitter.com/ReformedTrader/status/1200183194718371840

Equity Factors: To Short Or Not To Short

https://twitter.com/ReformedTrader/status/1252013541487304707

Shorting Costs and Profitability of Long–Short Strategies

https://twitter.com/ReformedTrader/status/1249502722253971457

• • •

Missing some Tweet in this thread? You can try to

force a refresh