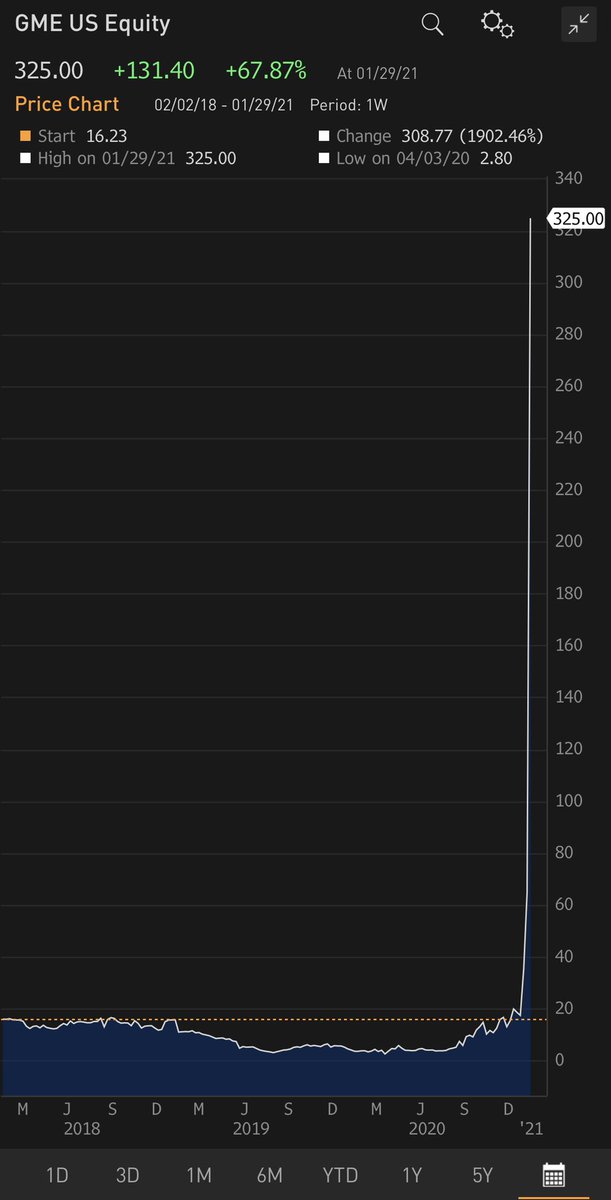

Why wouldn’t $GME execs take advantage of the $300/sh stock price to raise capital to transform their business? A $2B cap raise on $22B mkt cap (10%) would dwarf the entire $1.4B market cap at which $GME was trading 3 weeks ago. The obvious buyer? Some of the 58M shares short.

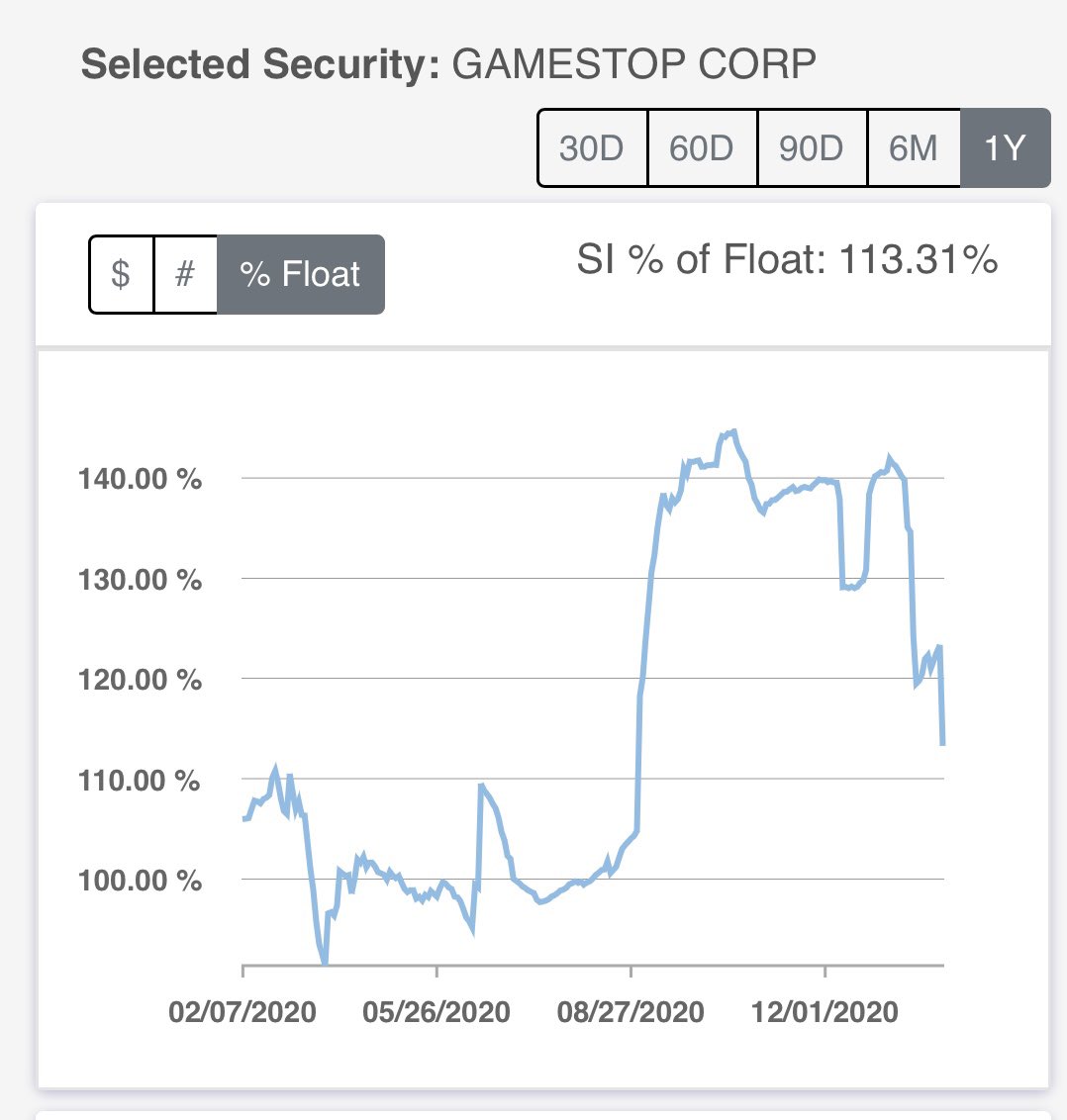

2/ Perhaps Ryan Cohen and his fellow new board members don’t want to ease the squeeze. If $GME short int fell below 100%, Reddit traders may go elsewhere. Or they don’t want to put out an S-1 that shows how bad the $GME business really is. Sunlight can be a bad disinfectant.

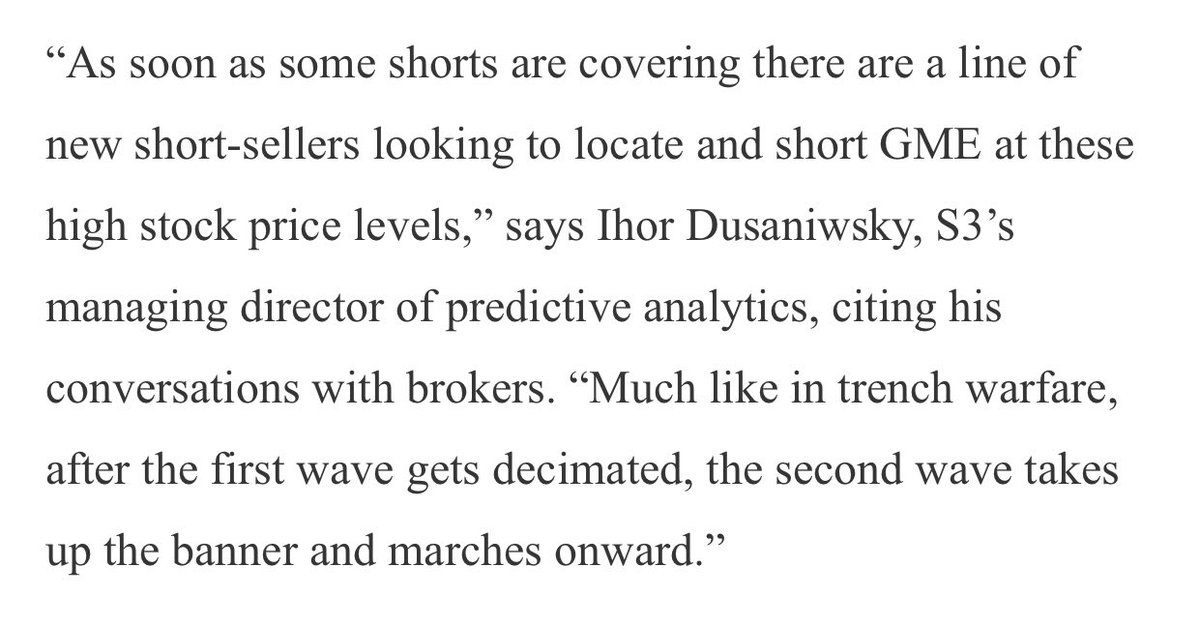

3/ My view: A secondary combined with new action by Treasury, SEC, or the brokers to squash $GME speculation will push GME back to $20/share. At a 50% borrow (12.5% for 3 mos), new shorts will take up the battle, much like the second wave of an infantry, and $GME will collapse.

For the record, I am not short $GME. There needs to be a catalyst. I’ll know it when I see it.

• • •

Missing some Tweet in this thread? You can try to

force a refresh