Quick thread on $AMZN valuation.

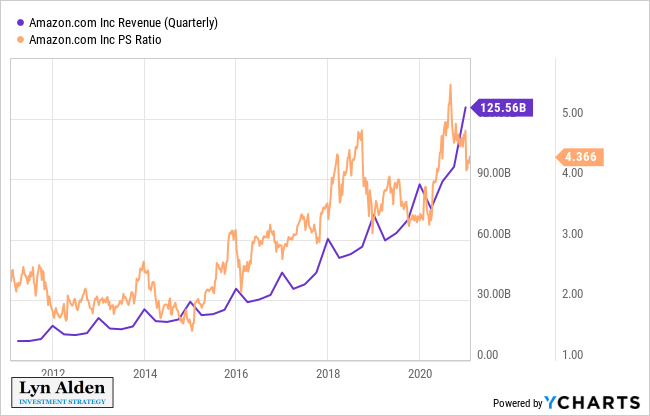

From a price to sales perspective, it remains elevated compared to its history:

From a price to sales perspective, it remains elevated compared to its history:

However, operating cash flow has grown more quickly than revenue.

From a price to cash flow perspective, Amazon is near the mid-to-low end of its historical valuation range:

From a price to cash flow perspective, Amazon is near the mid-to-low end of its historical valuation range:

Amazon stock has followed a 25x operating cash flow multiple almost like clockwork for nearly two decades.

Chart via @FASTGraphs

Chart via @FASTGraphs

My base case would be for a consolidation and then move higher over the next 3 years, but the big variable that could derail the valuation narrative would be notably higher treasury rates.

• • •

Missing some Tweet in this thread? You can try to

force a refresh