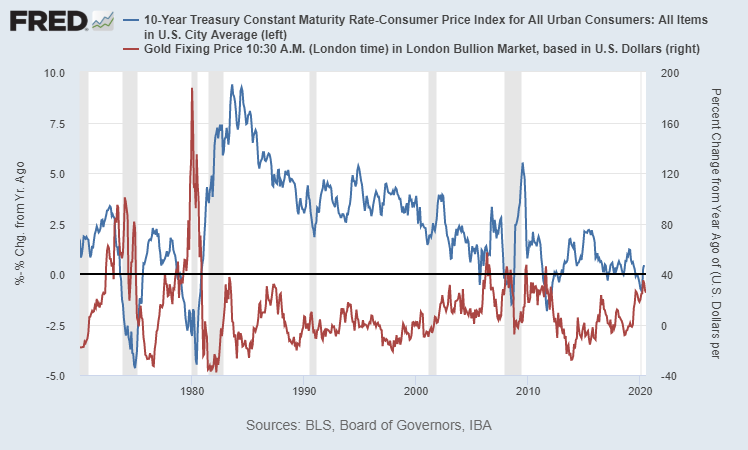

When interest rates hit zero for the first time in decades, interesting things happen.

Here's the 100-year chart of total debt to GDP in blue on the left axis, vs interest rates in orange on the right axis. Total debt includes public and private debt.

Here's the 100-year chart of total debt to GDP in blue on the left axis, vs interest rates in orange on the right axis. Total debt includes public and private debt.

Another way of looking at it is total debt as a % of M2.

With this metric, we can see the big changes since 2008 in particular. The ratio dropped from 700% to 400% in 12 years.

With this metric, we can see the big changes since 2008 in particular. The ratio dropped from 700% to 400% in 12 years.

If we separate out federal debt vs nonfederal debt as a percentage of GDP, it also provides more clarity.

In each long-term cycle, the first stage was a private debt bubble and banking crisis, while the second stage was a public debt bubble and massive M2 increase.

In each long-term cycle, the first stage was a private debt bubble and banking crisis, while the second stage was a public debt bubble and massive M2 increase.

Lastly, we can look at the monetary base as a percentage of GDP. When rates hit zero, monetary policy shifts to increasing the monetary base instead (aka QE).

More charts here:

lynalden.com/fiscal-and-mon…

What has been will be again, what has been done will be done again; there is nothing new under the sun.

lynalden.com/fiscal-and-mon…

What has been will be again, what has been done will be done again; there is nothing new under the sun.

• • •

Missing some Tweet in this thread? You can try to

force a refresh