1) When we start with Asset Allocation, actually we are already underweight equities (less than 100%) based on the % of temporary falls we can tolerate.

2) This default underweight does not require identifying 'when' the market will crash. But should be based on expectation (derived from history) i.e 10-20% temporary decline almost every year and 50-60% temporary fall once every 7-10 years in equities.

3) If markets happen to crash suddenly, our default underweight position (called asset allocation) will reduce the impact and debt allocation can be used to buy at lower levels

4) Going underweight beyond this needs to be a rare thing - not trying to time every 10-20% fall. Here is a heuristic for going u/w below the original allocation - even at 20% lower prices will you still be negative on the markets - if yes, then this needs serious evaluation.

5) Look out for a combination of extremes in 1) Valuations (pe,pb,mcap to gdp, earnings yield vs bond yields), 2) Earnings cycle 3) Sentiments (fii, dii flows, ipo, past returns etc)

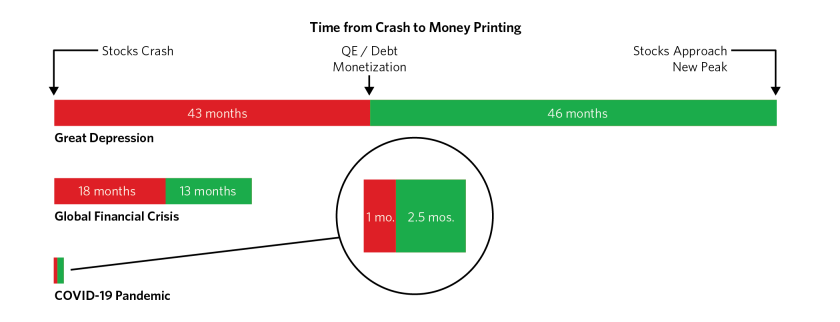

6) Remember markets can remain irrational for a long time - and you may miss out on significant upmoves - the last leg of bull markets is vociferous.

The best of investors and economists have got underweight calls wrong. We are no exception.

The best of investors and economists have got underweight calls wrong. We are no exception.

7) So build another layer of "room for error" via shifting to Dynamic Asset Allocation funds instead of debt when you want to go underweight. Trend following strategies may work well.

Don't take the all in or all out approach. Keep it limited to a certain % of equity.

Don't take the all in or all out approach. Keep it limited to a certain % of equity.

8) If you find all this complicated. It is! Here is a simple solution - Time and Patience are superpowers. If you got this, ignore all the above and stick to a simple annual rebalancing plan. This will do wonders!

• • •

Missing some Tweet in this thread? You can try to

force a refresh