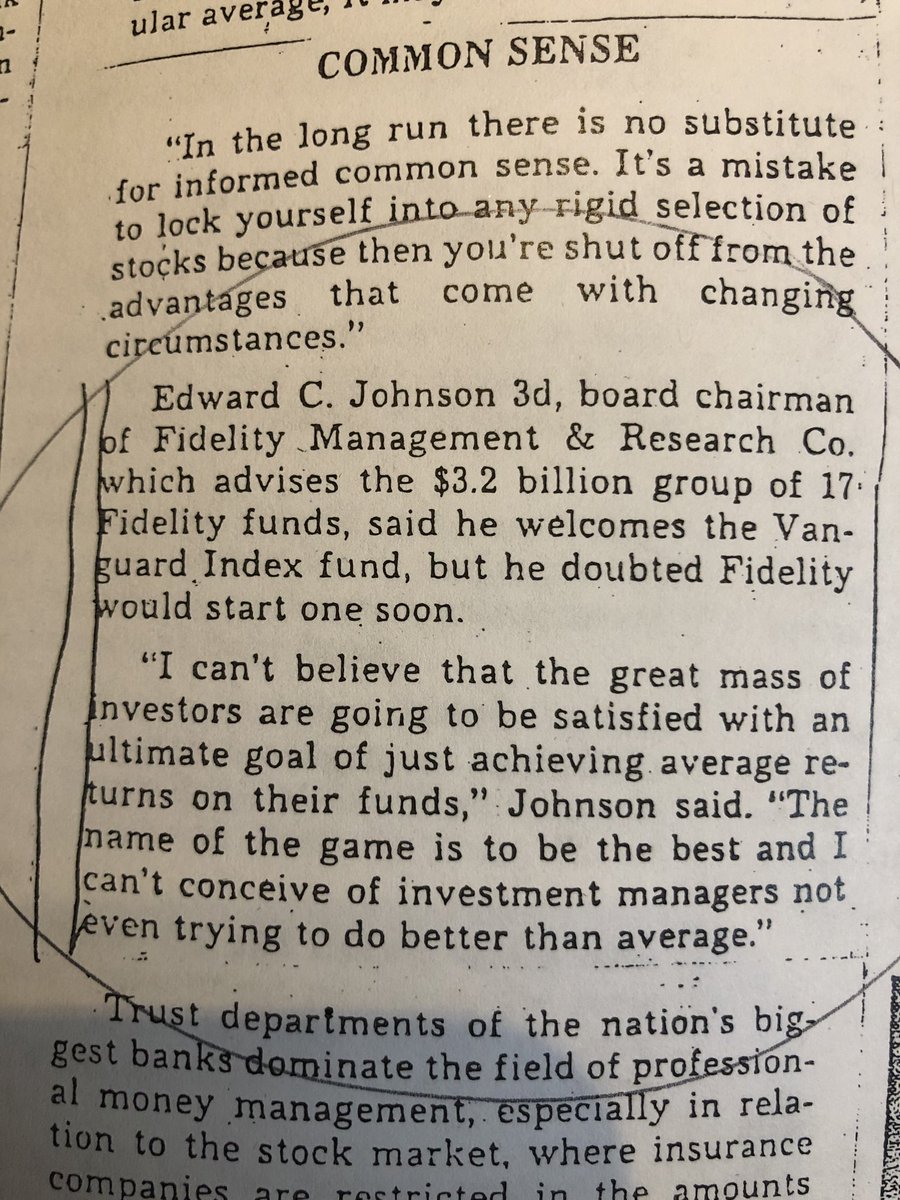

“Indexing doesn’t constitute any real threat to professional managers because its goal is mediocre performance.” Cleaning up some of my book research notes, and there are some 👀 quotes there.

(From the Boston Globe, august 24, 1976)

David Babson REALLY didn’t like the smell of this new fad.

“Index funds... an idea whose time has passed”. Professor Roger Murray in 1976.

🤪

If you like this, then pretty-please pre-order my book! amazon.com/dp/0593087682

• • •

Missing some Tweet in this thread? You can try to

force a refresh