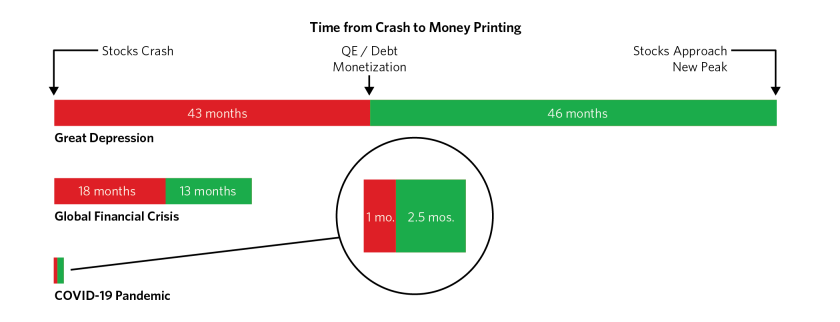

1/4

Thumb rule to understand Inflation: RULE of 2

In India, Inflation historically has been around 7%.

Boring Stat!

Here is what this really means -

Our COSTS DOUBLE EVERY 10 YEARS!

So if our money doubles in the next 10 years, we are still at square one!

Thumb rule to understand Inflation: RULE of 2

In India, Inflation historically has been around 7%.

Boring Stat!

Here is what this really means -

Our COSTS DOUBLE EVERY 10 YEARS!

So if our money doubles in the next 10 years, we are still at square one!

2/4

The rough math for a 7% inflation implies prices will approximately go up by

1.4x or 40% up in the next 5 years

2x in the next 10 years

3x in the next 15 years

4x in the next 20 years

The rough math for a 7% inflation implies prices will approximately go up by

1.4x or 40% up in the next 5 years

2x in the next 10 years

3x in the next 15 years

4x in the next 20 years

3/4

How do we use this?

If your monthly expenditure is Rs 1 lakh today then it becomes

1.4x i.e Rs 1.4 lakhs after 5 years

2x i.e Rs 2 lakhs after 10 years

3x i.e Rs 3 lakhs after 15 years

4x i.e Rs 4 lakhs after 20 years

How do we use this?

If your monthly expenditure is Rs 1 lakh today then it becomes

1.4x i.e Rs 1.4 lakhs after 5 years

2x i.e Rs 2 lakhs after 10 years

3x i.e Rs 3 lakhs after 15 years

4x i.e Rs 4 lakhs after 20 years

4/4

Assume your kid is 2 years. Current cost of college ~Rs 10 lakhs.

Without using excel, you can quickly find the rough college cost after 15 years to be 3x of 10 lakhs i.e Rs 30 lakhs.

So go ahead calculate all your future costs in your next chai break :)

Assume your kid is 2 years. Current cost of college ~Rs 10 lakhs.

Without using excel, you can quickly find the rough college cost after 15 years to be 3x of 10 lakhs i.e Rs 30 lakhs.

So go ahead calculate all your future costs in your next chai break :)

• • •

Missing some Tweet in this thread? You can try to

force a refresh