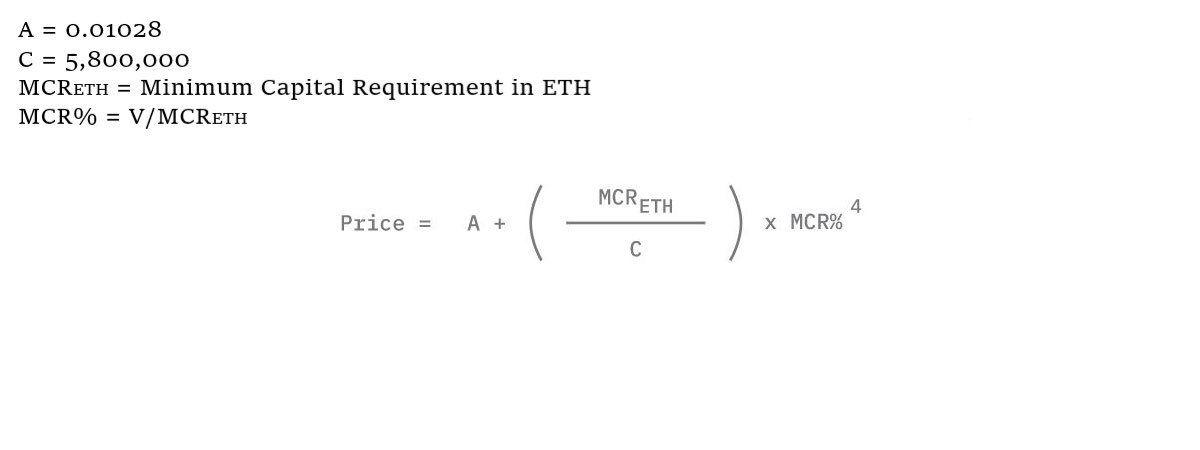

If a mutual member’s funds are lost due to an event outlined in the cover agreement, they can file a claim.

Any cover purchased after 21 October 2021 requires proof of loss when filing a claim. (1/9)

Any cover purchased after 21 October 2021 requires proof of loss when filing a claim. (1/9)

As I mentioned in the tweet below, 10% of your cover premium is reserved for filing a claim. You need to stake 5% of the cover premium to file a claim.

Because 10% is reserved for filing a claim, you can submit a claim for assessment 2 times. (2/9)

Because 10% is reserved for filing a claim, you can submit a claim for assessment 2 times. (2/9)

https://twitter.com/BraveDeFi/status/1380218072439652353

If a claim is accepted, the 5% staked for claims assessment is returned.

If a claim is denied, the 5% staked for claims assessment is forfeited. (4/9)

If a claim is denied, the 5% staked for claims assessment is forfeited. (4/9)

Once a claim is submitted, it is reviewed by Claims Assessors. I’ll go into more detail about Claims Assessors tomorrow, but below is a brief overview. (5/9)

To vote on a claim, Claims Assessors need to stake $NXM. Between all assessors, the total amount of staked $NXM needs to be 5x greater than the claim being voted on.

If Claims Assessors reach 70% consensus in favor of a claim, it's accepted. See diagram for more detail. (6/9)

If Claims Assessors reach 70% consensus in favor of a claim, it's accepted. See diagram for more detail. (6/9)

If Claims Assessors do not come to a 70% consensus on a claim, then the claim is put to a full member vote which requires a consensus of over 50%. (7/9)

For information on past claims and claims assessment decisions, you can review the Claims History section in the docs: nexusmutual.gitbook.io/docs/users/cla…

(8/9)

(8/9)

If you have questions about buying cover or filing a claim, you can visit the Nexus Mutual Discord: discord.gg/xxFaAEn

This concludes today’s @NexusMutual helpful threads.

I’ll review Claims Assessment, Risk Assessment, and Governance topics tomorrow. 😁👋🐢 (9/9)

This concludes today’s @NexusMutual helpful threads.

I’ll review Claims Assessment, Risk Assessment, and Governance topics tomorrow. 😁👋🐢 (9/9)

• • •

Missing some Tweet in this thread? You can try to

force a refresh