1/ Just added on $ETSY. My avg. cost increased from $114 to $122

A few questions that I received:

A few questions that I received:

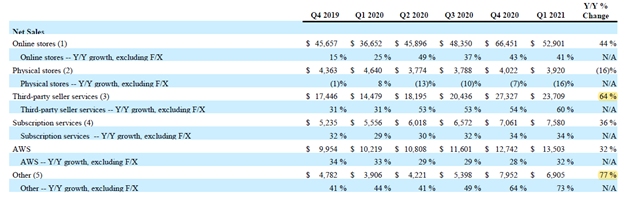

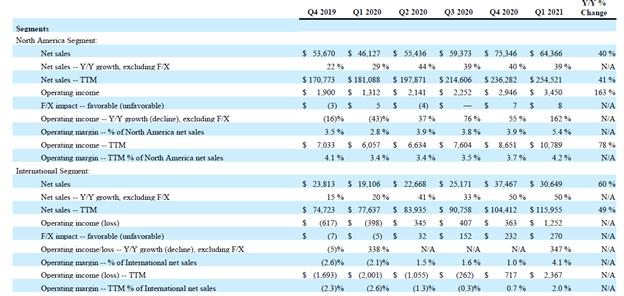

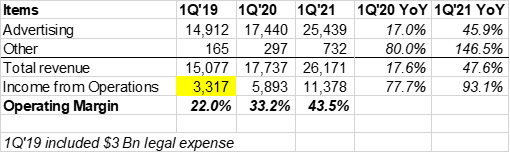

2/ Q1: How can $AMZN guide 24-30% growth when Etsy guided 5-15% GMS growth?

Four counter points.

I. Let’s look at apple to apple as much as possible. AMZN’s guide was on revenue. Etsy’s revenue guide is 15-25%.

Four counter points.

I. Let’s look at apple to apple as much as possible. AMZN’s guide was on revenue. Etsy’s revenue guide is 15-25%.

3/

II. If we exclude masks from last year’s GMS and if Etsy does the high end of guidance next quarter ($3.1 Bn GMS), GMS growth is 32% YoY, not 15%.

III. AMZN moved its Prime day from Q4 last year to Q2 this year which would bump ~5-6% topline growth YoY.

II. If we exclude masks from last year’s GMS and if Etsy does the high end of guidance next quarter ($3.1 Bn GMS), GMS growth is 32% YoY, not 15%.

III. AMZN moved its Prime day from Q4 last year to Q2 this year which would bump ~5-6% topline growth YoY.

4/

IV. AMZN is bit of a miracle. If you benchmark against AMZN for any company, you’ll mostly be disappointed.

Nobody is as good as AMZN is. This is why a Seattle-based online book store ended up conquering capitalism.

Etsy isn’t going to do that. It’s NOT your next AMZN.

IV. AMZN is bit of a miracle. If you benchmark against AMZN for any company, you’ll mostly be disappointed.

Nobody is as good as AMZN is. This is why a Seattle-based online book store ended up conquering capitalism.

Etsy isn’t going to do that. It’s NOT your next AMZN.

5/ Q2: What about IG Shopping?

Good question. If you are following me for a while, you know I'll be the last person to underestimate Zuck.

Unfortunately, we don’t have much data points to properly assess how Etsy is faring against IG Shopping.

Good question. If you are following me for a while, you know I'll be the last person to underestimate Zuck.

Unfortunately, we don’t have much data points to properly assess how Etsy is faring against IG Shopping.

6/ GMV through FB Shops became 4x YoY, but obviously from a very low base.

Too early to say, but this is indeed one of the risks.

Too early to say, but this is indeed one of the risks.

7/ Q3: What about the buybacks?

I am very encouraged to see there was no buyback at all in 1Q’21. Will Josh Silverman mostly buyback opportunistically and not on autopilot mode?

I am very encouraged to see there was no buyback at all in 1Q’21. Will Josh Silverman mostly buyback opportunistically and not on autopilot mode?

8/ We’ll have a hint in the next earnings if they decide to buyback decent chunk of shares now that stock is down 35% from the peak.

End/ Thread on 1Q’21 earnings here if you missed this:

https://twitter.com/borrowed_ideas/status/1390138966607806468

• • •

Missing some Tweet in this thread? You can try to

force a refresh