Just finished a piece on secular stagnation and interest rate. Developed version of what I send a few month ago to Trust and Estate magazine. Here are the main points:

1- key driver of interest-rate trend is monetary policy. It is not inflation, fiscal balance, or credit rating.

1- key driver of interest-rate trend is monetary policy. It is not inflation, fiscal balance, or credit rating.

2- to make sense of what interest rates will do in the future, need to make expectations about what FOMC will do

3- low-growth + high leverage economy makes it difficult for FOMC to raise rate quickly and much + low inflation will persist no incentive to raise policy rates much.

3- low-growth + high leverage economy makes it difficult for FOMC to raise rate quickly and much + low inflation will persist no incentive to raise policy rates much.

4- growing inequalities, jobless recovery, growing job precariousness, lack of shared prosperity => we can expect low rate to last for a decade or more unless policies are put in place to reverse stagnationist forces.

5- low interest rate environment poses challenge for Money Manager Capitalism that is deeper than "bubble". Money managers have rate of return targets => buy riskier assets and use leverage to compensate for low => promotes use and spread of Ponzi finance

6- Private pension system can't generate financial safety for retirees without promoting overall financial fragility.

7- Economic growth is demand driven (Domar, Walker and Vatter, PKs...) and investment-led growth is unstable => central role for gov to promote ecological and financially sustainable shared economic growth

8- example of major role: ILE show need of rapid and radical shift in energy structure that requires heavy involvement of gov at all levels to shift domestic resources to that goal (R&D, invention to innovation, dvpt and promotion of market)

IEA (not ILE): International Energy Agency (recent Net Zero by 2050 report)

As for my other papers, draft will be on my webpage shortly

A few graphs and tables from the paper (US driven I am afraid)

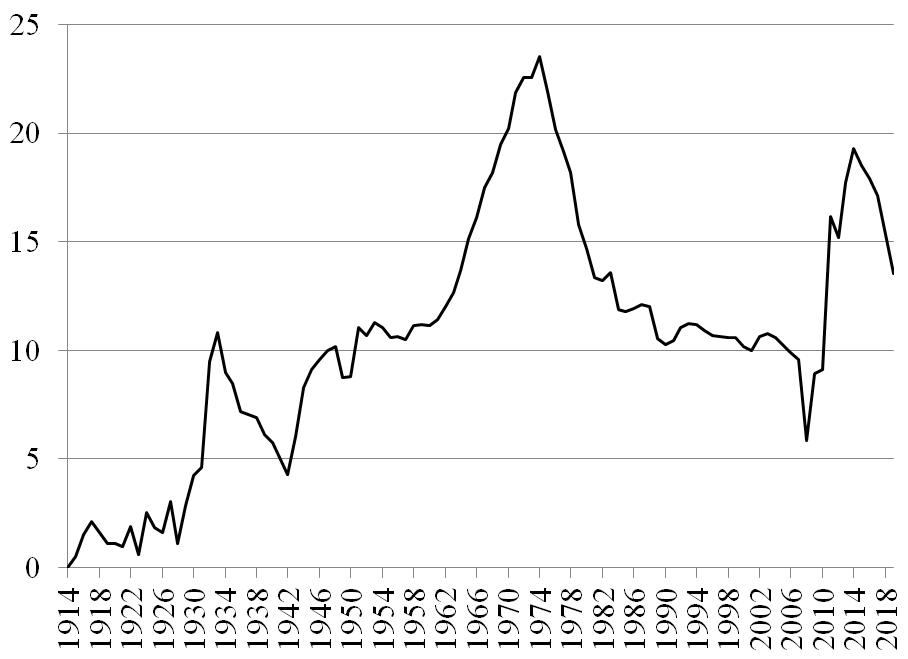

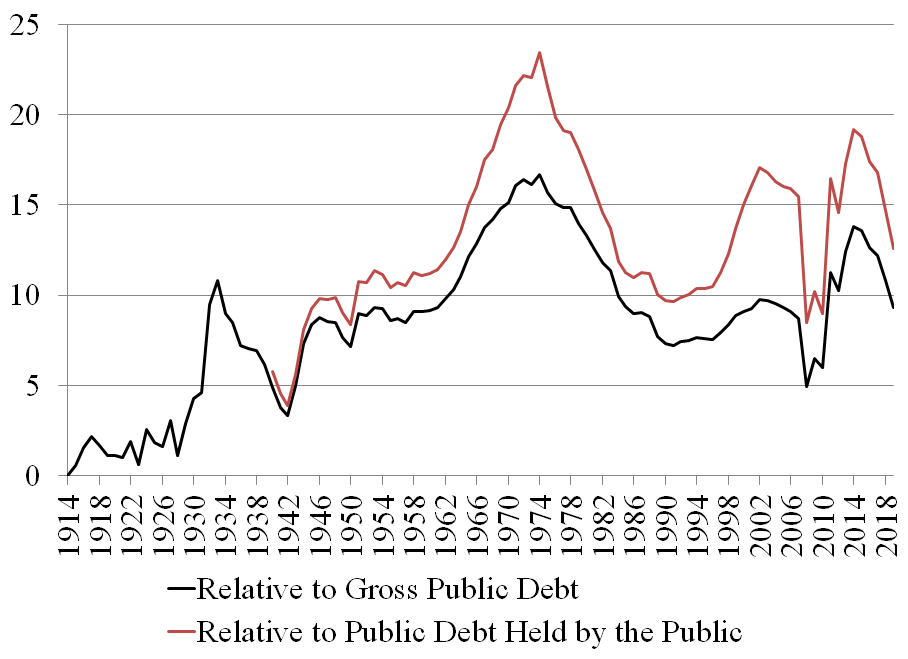

Monetary policy and nominal interest rates, January 1919 to June 2021

Monetary policy and nominal interest rates, January 1919 to June 2021

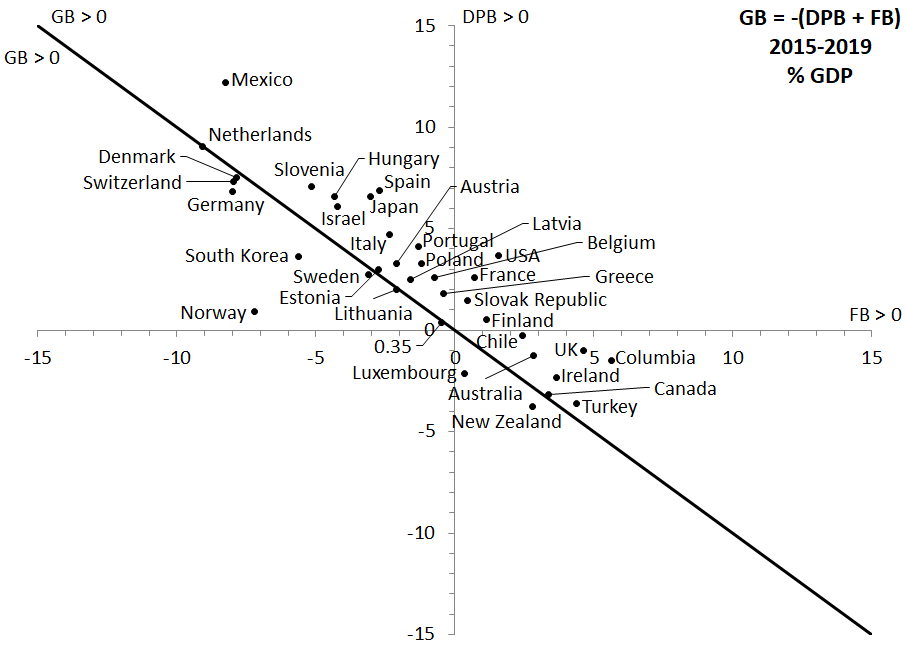

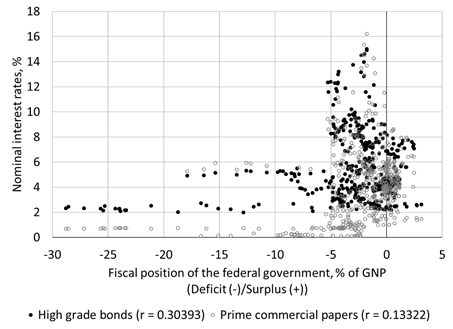

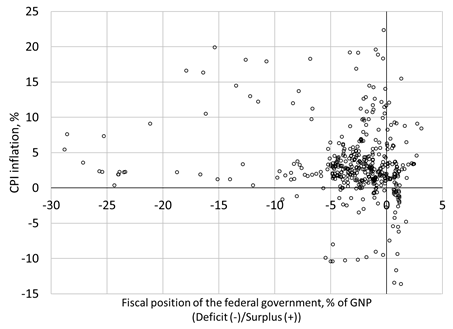

Figure 3. Fiscal Balance and Interest Rates, 1900 to 2021

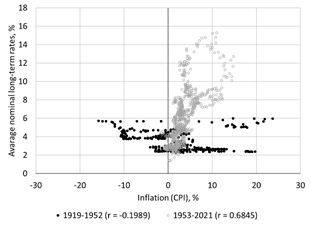

Figure 4 Inflation and interest rates, 1919 to 2021 (Here only shows long-term rates)

Figure 5. A century of fiscal balance and inflation, Q1 1914 to Q1 2021

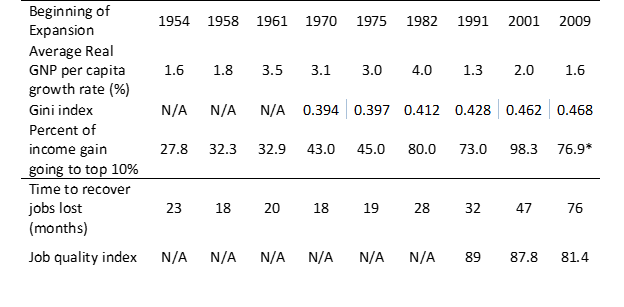

Table 2. Long-term economic outlook: Toward Secular Stagnation

• • •

Missing some Tweet in this thread? You can try to

force a refresh