1/

My thoughts on the $CRYPTO market over the coming weeks!

Hope you enjoy!

'Funding rates are yet to spike'

My thoughts on the $CRYPTO market over the coming weeks!

Hope you enjoy!

'Funding rates are yet to spike'

2/

'Funding rates are yet to spike' (ctd)

'Funding rates are yet to spike' (ctd)

3/

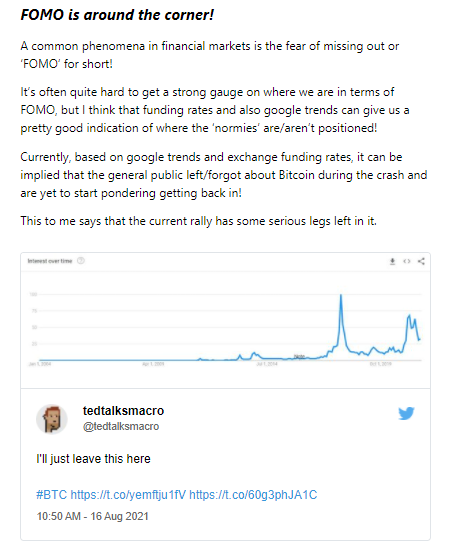

'FOMO is around the corner'

'FOMO is around the corner'

4/

'Demand for downside protection for the August month-end expiry'

'Demand for downside protection for the August month-end expiry'

5/

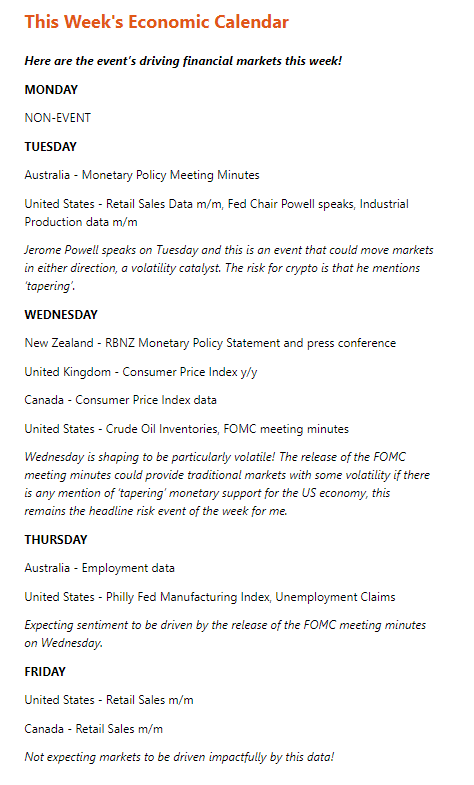

This Week's Economic Calendar

This Week's Economic Calendar

7/

Thanks for reading, if you'd like to have these newsletters delivered for free (2x per week), please subscribe via the link below 👇

getrevue.co/profile/MacroU…

Thanks for reading, if you'd like to have these newsletters delivered for free (2x per week), please subscribe via the link below 👇

getrevue.co/profile/MacroU…

• • •

Missing some Tweet in this thread? You can try to

force a refresh