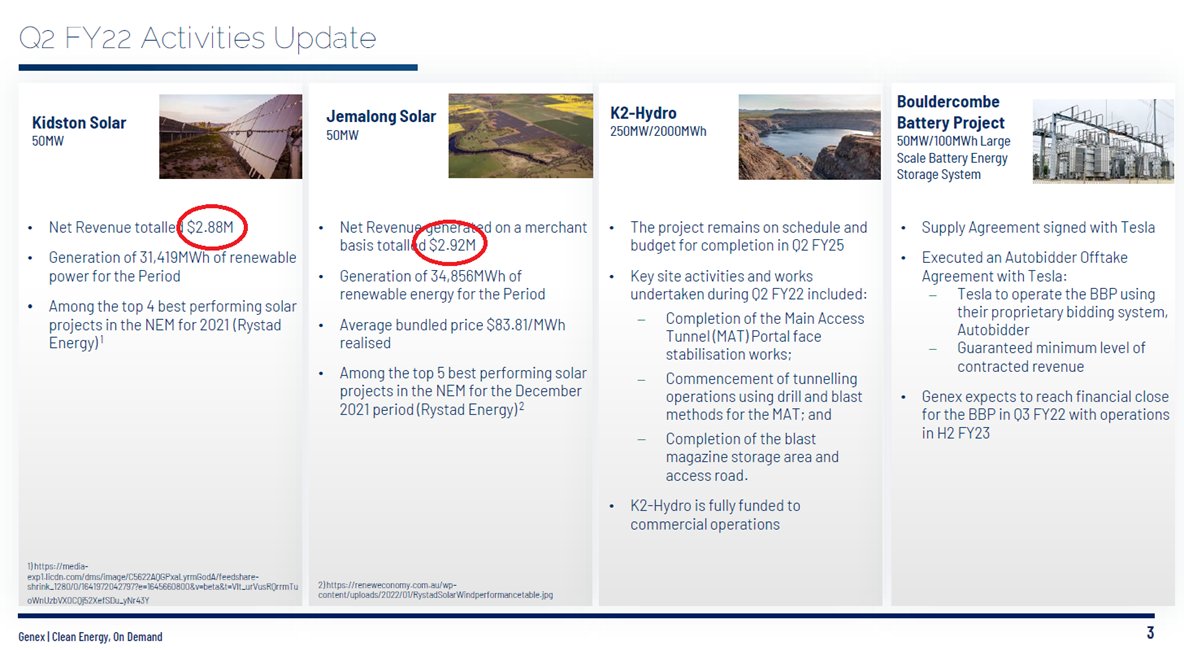

Tassal $TGR $TGR.AX reported their FY21 results to a mute market response. So, what happened that made the share price do basically nothing when it’s the 7th most shorted (7.5% shares) company on the #ASX?

My six key takeaways 👇

My six key takeaways 👇

To recap my investment thesis I am betting that Tassal can double revenue, triple EBITDA, and quadruple cash flow / dividends from FY20 to FY30. This report has done nothing to dampen my expectations.

You can see my previous deep dives here 👇

You can see my previous deep dives here 👇

https://twitter.com/DownunderValue/status/1379956575461249029

The results for FY21 and 2H21 were weak, impacted heavily by covid headwinds. I won’t repeat the investor presentation - for those interested, it’s just a click away:

cdn-api.markitdigital.com/apiman-gateway…

cdn-api.markitdigital.com/apiman-gateway…

1. Salmon domestic is a tough competitive business. The two big supermarkets $COL $WOW have renegotiated excellent rates that puts downward pressure on margins for 3-5 years.

No significant growth can realistically be expected here.

No significant growth can realistically be expected here.

A possible outcome is $HUO owners seek to increase margins, which benefits TGR's wholesale market. Petuna has taken a low risk / high volume / low margin approach to supply the supermarkets delis - but if deli-salmon is removed in 3yrs, Tassal has pole position with their MAP.

2. Salmon exports was a missed opportunity. Despite low prices in 1H21, they returned to normal in March and Tassal didn’t export enough. They have realised their mistake and have set record export volumes in July and August 2021 (1H22).

What could have been…. ?

What could have been…. ?

TGR had 7000t of salmon in their freezers. If this was reduced to normalised ~2000t, it would have added around $60m revenue and $12m EBITDA (up 8% instead of 0.6%), and potentially negated any NPAT losses.

This may have been the difference on squashing the short thesis. 🤷

This may have been the difference on squashing the short thesis. 🤷

3. Air freight is a massive headwind, and should be reported under EBITDA. It was $16.4m in FY21 (~$2/kg for exports), and may come down to $1.70/KG as they focus on China. But still, this won’t disappear in FY22 (“one off”?).

h/t to @abroninvestor that flagged this too.

h/t to @abroninvestor that flagged this too.

4. CAPEX has come down, and will continue to do so. A major part of the short thesis is the CAPEX requirements will remain elevated and depreciation is under reported. It reduced by +$30m in FY21 and will reduce by ~$20m in FY22 – ongoing savings that hit the FCF.

TGR can scale up the salmon to 45,000t by FY25 and prawns to 20,000t by FY30 with very little additional CAPEX too – e.g. they have the land, just need the ponds / permits. 👊

Depreciation will reduce, ROA will increase as prawns have 1-2% depreciation vs salmon 8-10%.

Depreciation will reduce, ROA will increase as prawns have 1-2% depreciation vs salmon 8-10%.

5. Normalised earnings expected for FY23+ are really strong. The platform for growth is in place. Once CAPEX lowers and the market conditions fully return to normal (almost there ex. air freight), operating cash flow may +60% and FCF becomes positive.

Here’s my model👇

Here’s my model👇

6. ESG is a real focus. They contend that Tassal is best-in-class, and that salmon and prawns are more efficient forms of protein. One of their next growth platforms may also be seaweed / blue carbon farming.

Here’s their response to Flannery’s Toxic:

Here’s their response to Flannery’s Toxic:

If you enjoyed this, bash the like / retweet / follow buttons.

A deep dive per week is my commitment to FinTwit.

Questions and feedback always welcome. DYOR.

Disclaimer, I'm long TGR.

A deep dive per week is my commitment to FinTwit.

Questions and feedback always welcome. DYOR.

Disclaimer, I'm long TGR.

• • •

Missing some Tweet in this thread? You can try to

force a refresh