MARKET PRICES - volatility, liquidity and trading around extreme high and low prices - some personal reflections on the current European gas market but equally applicable to oil, electricity, coal, steel and other commodities:

EUROPEAN natural gas prices are nearing a peak - in time if not price.

As liquidity falls, prices are rising at an accelerating rate - a classic sign that the turning point is near

Market time is becoming telescoped:

As liquidity falls, prices are rising at an accelerating rate - a classic sign that the turning point is near

Market time is becoming telescoped:

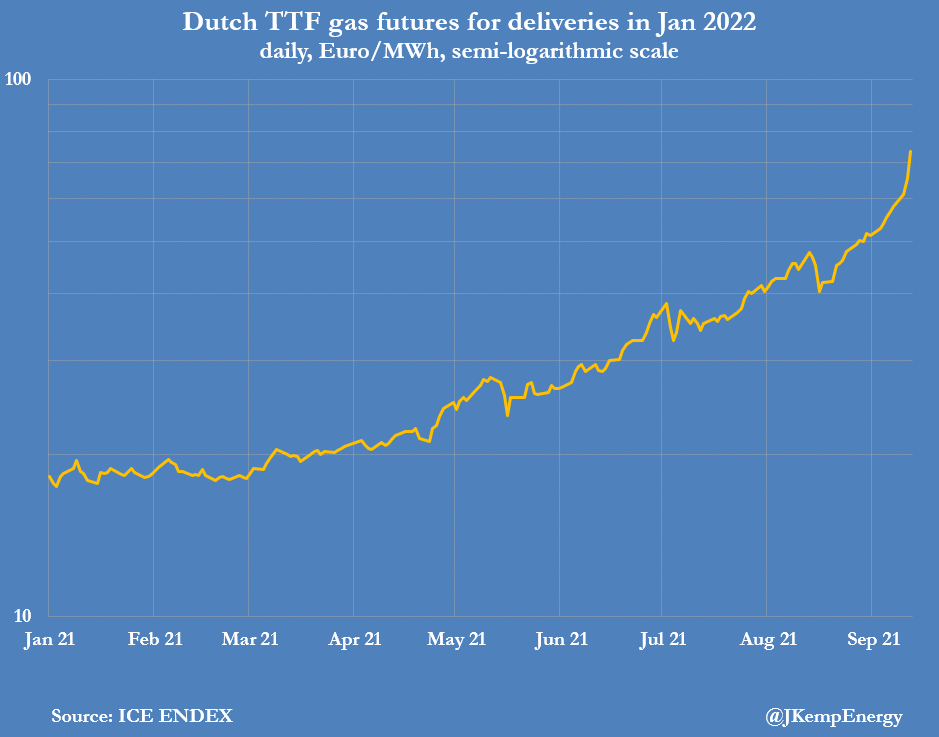

EUROPEAN natural gas prices - shown in a semi-log scale to show the acceleration in price gains. First and second derivatives now strongly positive - with prices turning vertical - classic indicator normal pricing relationships are breaking down under extreme stress:

• • •

Missing some Tweet in this thread? You can try to

force a refresh