RocoMamas is the top performer in the Spur Corporation stable in the last 2 years.

The RocoMamas brand seems to have fitted well in the Spurs Corporation stable.

Spur Corporation was bought two brands in 2015.

The RocoMamas brand seems to have fitted well in the Spurs Corporation stable.

Spur Corporation was bought two brands in 2015.

1) Spur bought a 51% interest in the RocoMamas Franchise Co, (owners of the trademark and related intellectual property of RocoMamas) in 2015.

Purchase consideration was determined as 5x RocoMamas’ EBITDA of the 3rd year following date of acquisition which ended on 28 Feb 2018.

Purchase consideration was determined as 5x RocoMamas’ EBITDA of the 3rd year following date of acquisition which ended on 28 Feb 2018.

The total purchase consideration actually paid over the three-year period was ~R59.2m determined as follows;

Initial payment of R2m,

Annual payment of R20.4m in the 1st year after the acquisition

R18.3m 2nd in the second year.

Final payment of R18.54m was paid in March 2018.

Initial payment of R2m,

Annual payment of R20.4m in the 1st year after the acquisition

R18.3m 2nd in the second year.

Final payment of R18.54m was paid in March 2018.

At acquisition of the 51% stake in RocoMamas, it only had 5 restaurants.

On 1 Apr 2017, the Spur Corporation acquired a further 19% interest in RocoMamas taking the Group’s equity interest in RocoMamas to 70%.

Purchase consideration for thd 19% was R14.04m and settled in cash.

On 1 Apr 2017, the Spur Corporation acquired a further 19% interest in RocoMamas taking the Group’s equity interest in RocoMamas to 70%.

Purchase consideration for thd 19% was R14.04m and settled in cash.

From 5 restaurants in 2015, the Spur Corporation has made to increase the number of RocoMamas stores as at 31 Dec 2020 to;

69 in South Africa Africa

9 in the rest of Africa

4 India and Middle East

1 Australasia

The capital expenditure for this expansion was massive.

69 in South Africa Africa

9 in the rest of Africa

4 India and Middle East

1 Australasia

The capital expenditure for this expansion was massive.

2) Spur bought Hussar Grill steakhouse chain for R35 million in cash.

Hussar Grill comprised six restaurants at the time of purchase.

3 of the restaurants were company-owned and 3 were

franchised outlets.

This gave the group exposure to an upmarket specialist steakhouse chain.

Hussar Grill comprised six restaurants at the time of purchase.

3 of the restaurants were company-owned and 3 were

franchised outlets.

This gave the group exposure to an upmarket specialist steakhouse chain.

Spur Corporation has grown the Hussar Grill brand significantly since the 2015 acquisition when it had 6 stores.

Total Hussar Grill stores is 24

SA 22

Africa 1

Middle East 1.

The Hussar Grill outlets took a beating in 2020 due to the restriction on the sale of alcohol.

Total Hussar Grill stores is 24

SA 22

Africa 1

Middle East 1.

The Hussar Grill outlets took a beating in 2020 due to the restriction on the sale of alcohol.

The worst performer year on year is Nikos Coalgrill Greek.

Spur Corporation acquired a 51% shareholding from the founding family members in 2018 with an option to acquire an additional 19% shareholding after three years.

Spur Corporation acquired a 51% shareholding from the founding family members in 2018 with an option to acquire an additional 19% shareholding after three years.

Some fun fact.

Spur gets its beef patties from the same plant as Burger King South Africa.

The meat plant was wholly owned by Grand Parade Investments (GPI) and is called Grand Foods Meat Plant (GFMP).

GPI has a 9,1% effective interest in Spur.

Spur gets its beef patties from the same plant as Burger King South Africa.

The meat plant was wholly owned by Grand Parade Investments (GPI) and is called Grand Foods Meat Plant (GFMP).

GPI has a 9,1% effective interest in Spur.

Deal between GPI and ECP is going ahead with the absence of Grand Foods Meat Plant that will now be sold to a black owner for R23m.

ECP will spend R500m opening new stores, creating jobs.

ECP had agreed to create a 5% black empowerment stake within two years.

ECP will spend R500m opening new stores, creating jobs.

ECP had agreed to create a 5% black empowerment stake within two years.

GPI paid R700m for the Burger King master franchise for the Republic of South Africa in 2012.

It is selling its entire 91,1% stake in Burger King SA to ECP and will capitalise loans to the firm amounting to a 4.7% stake leading to a total divestment of a 95.7% stake for ~R570m.

It is selling its entire 91,1% stake in Burger King SA to ECP and will capitalise loans to the firm amounting to a 4.7% stake leading to a total divestment of a 95.7% stake for ~R570m.

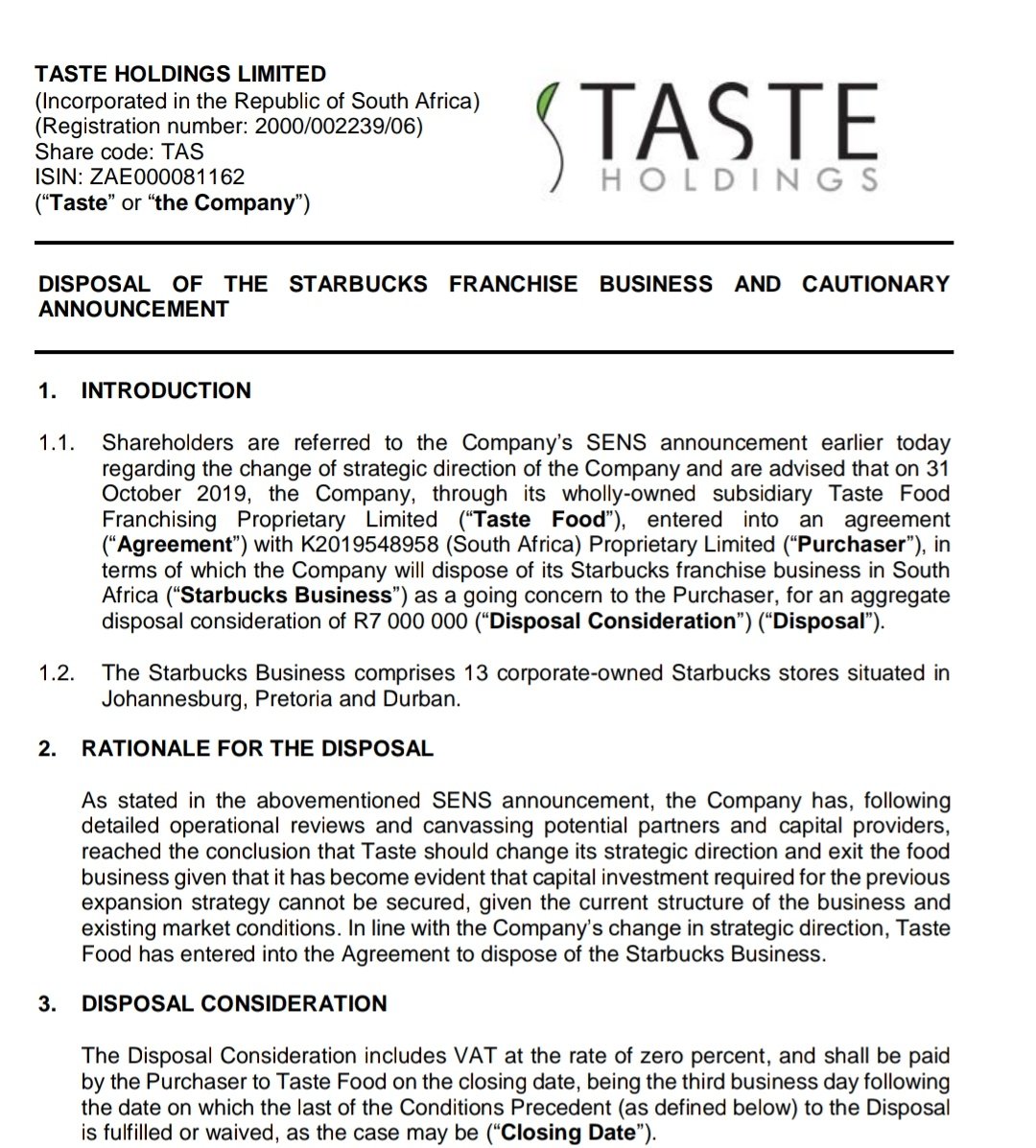

Taste Holdings bought the South African master licence agreement for Starbucks for R226m in 2015 for 25 years.

Taste was required to pay yearly royalties to Starbucks US of R2.5 million.

Taste had envisaged on establishing 12 to 15 outlets within the first 24 months.

Taste was required to pay yearly royalties to Starbucks US of R2.5 million.

Taste had envisaged on establishing 12 to 15 outlets within the first 24 months.

Capital expenditure and pre-opening expenses for the first 12 to 15 stores were estimated at R108m.

Market opportunity was estimated at 150-200 outlets, at an estimated capital expenditure per store of R3m-R10m.

We all know they never got to that 150-200 outlets.

Market opportunity was estimated at 150-200 outlets, at an estimated capital expenditure per store of R3m-R10m.

We all know they never got to that 150-200 outlets.

Taste Holdings later disposed of 13 Starbucks stores for a mere lousy R7m, which was ~R538k a store as well as the franchise master to Rand Capital Coffee.

The estimated cost of opening a Starbucks store in South Africa was around R3m-R10m at the time.

The estimated cost of opening a Starbucks store in South Africa was around R3m-R10m at the time.

October 2015, Taste raised R226m via a rights offer of 75m new shares at R3 each. This was shortly after it acquired the South African master licence agreement for Starbucks for 25 years.

This was the start (or continuion) of the destruction of shareholders' wealth.

This was the start (or continuion) of the destruction of shareholders' wealth.

December 2017, it (Taste) did other capital raising and raised ~R398m by issuing 442 million shares at 90c.

That rights offer came just 6 months after a “claw-back offer” in June 2017 in which Taste Holdings had raised R120m by issuing 80 million new shares at R1.50 each.

That rights offer came just 6 months after a “claw-back offer” in June 2017 in which Taste Holdings had raised R120m by issuing 80 million new shares at R1.50 each.

Inclusive of debt and share multiple rights issues, Taste management raised and squandered R1.4bn to keep Starbucks afloat.

The wealth destroyed over that period is one for the history books.

The wealth destroyed over that period is one for the history books.

Another blunder was when Taste Holdings bought and liquidated Domino’s SA after struggling to find a buyer.

Taste’s paid ~R6m for 15 stores with a negative net asset value of R10.25m and which made a loss after tax of R8.02m in the year ended 29 Feb 2016.

Taste’s paid ~R6m for 15 stores with a negative net asset value of R10.25m and which made a loss after tax of R8.02m in the year ended 29 Feb 2016.

Taste bought 60% of the ordinary shares in issue and 100% of the claims held by Fiamme Pizza in Aloysius Trading.

The then CEO of Taste, Carlo Gonzaga, was a director and shareholder of Aloysius through his shareholding in Fiamme Pizza.

The then CEO of Taste, Carlo Gonzaga, was a director and shareholder of Aloysius through his shareholding in Fiamme Pizza.

The total purchase consideration was R6 000 320 which was made up as follows;

R120 for the 120 shares in Aloysius

R6 000 000 for the claims in

Aloysius and

R200 for the subscription of 200 Aloysius shares.

R120 for the 120 shares in Aloysius

R6 000 000 for the claims in

Aloysius and

R200 for the subscription of 200 Aloysius shares.

Taste decided to place Taste Food Franchising (owned and licensed the Domino’s business in South Africa), Taste Commissary and Taste Food Trading into voluntary liquidation.

Taste then fully impaired the remaining intercompany loans with TFF and TC to the value of R450m.

Taste then fully impaired the remaining intercompany loans with TFF and TC to the value of R450m.

Taste management estimated that it would require ~R700m, including amount raised in the prior rights offers, to reach positive free cash flow and that the Starbucks network will need to expand to between 150 and 200 cafés and Domino’s to between 220 and 280 restaurants.

Taste then went and sold their entire food brands, comprising of; Starbucks, Domino’s Pizza, Maxi’s and The Fish & Chips Co in order to focus on "luxury" brands such as Arthur Kaplan & World’s Finest Watches (NWJ).

This let to a rebrand from Taste Holdings to Lux Holdings.

This let to a rebrand from Taste Holdings to Lux Holdings.

Spurs first listed on the JSE in 1986.

A restructuring of the group in 1999 resulted in the formation of the Spur Corporation.

Spur Corporation's fingers have also been burnt in acquisitions.

It introduced a drive thru service this year.

A restructuring of the group in 1999 resulted in the formation of the Spur Corporation.

Spur Corporation's fingers have also been burnt in acquisitions.

It introduced a drive thru service this year.

https://twitter.com/MaanoMadima/status/1399754575767298049?s=19

Comparison of Famous Brands (FB) and Spur Corporation is unfair at times.😂

FB has 2 436 restaurants in SA alone and had a turnover of ~R4,7bn for year ended 28 Feb 2021 (a 35% ⬇️ YoY)

Famous Brand's FY2021 revenue is ~5x the market cap of Spur.

Spur Corp has ~633 restaurants.

FB has 2 436 restaurants in SA alone and had a turnover of ~R4,7bn for year ended 28 Feb 2021 (a 35% ⬇️ YoY)

Famous Brand's FY2021 revenue is ~5x the market cap of Spur.

Spur Corp has ~633 restaurants.

• • •

Missing some Tweet in this thread? You can try to

force a refresh