FISCAL DOMINANCE is massively overstated as a motivation or risk for the Fed.

FINANCIAL DOMINANCE is greatly overstated as a motivation or risk for the Fed.

Understanding the actual Fed the issue is really about EMPLOYMENT DOMINANCE, and that is more good than bad. A 🧵:

FINANCIAL DOMINANCE is greatly overstated as a motivation or risk for the Fed.

Understanding the actual Fed the issue is really about EMPLOYMENT DOMINANCE, and that is more good than bad. A 🧵:

1. Fiscal dominance says the Central Bank deliberately keeps interest rates lower than it would otherwise in order to prevent the government's debt from growing too fast. With debt much higher than in the past they have the motive, so the argument goes, to keep rates low.

Most serious people think we don't have fiscal dominance now but some worry that we'll have it in the future if there is a less responsible Fed Chair or President. I think this misunderstands both the White House's interests and the Fed's actual behavior.

Any White House (not specifically commenting on this one) is always going to care much much more about inflation and employment (both of which matter to ordinary voters) than to whether the deficit is, say, $1.3T or $1.1T (a distinction that doesn't matter to voters).

Any White House will always care about what is, and is widely agreed should be, the Fed's mandate much more than it cares about changes in debt. (To the clear, the White House might weight unemp vs. inflation differently & certainly weights unemp today vs. tomorrow differently.)

Also, if the Fed keeps rates lower that doesn't have a huge immediate impact on deficits because it doesn't affect interest payments on longer dated bonds. It only matters as these bonds mature & get refinanced. And WH cares even less about $1.1T vs. $1.3T deficit 5 yrs from now.

And even if the White House cared more about how interest rates affect deficits a few years from now than employment and inflation the Fed would ignore them--and there are a lot of cultural and institutional checks that would need to be overcome to change that.

2. Financial dominance says the Fed is keeping rates lower than it would otherwise in order to keep stock prices high, either because it wants to help the rich or because it is afraid of a stock crash or some such.

This also misunderstands Fed policy. First, in the past there has been as much push in the opposite direction (raise rates to pop bubbles) as in this direction. But neither helping nor hurting financial markets its own sake has ever really carried the day in a huge way.

The Fed should, can and does care about overall financial conditions. So if interest rate spreads are rising and this threatens employment then it should consider easing.

In general, however, interest rates have been low because their naturally much lower than in the past, not because the Fed woke up with some crazy theory.

3. Employment dominance comes closer to explaining the way the Fed actually thinks and acts lately (and to a lesser degree in the past). They really care about maximum employment. This is a much, much, much, much bigger motivation than affecting interest on the debt

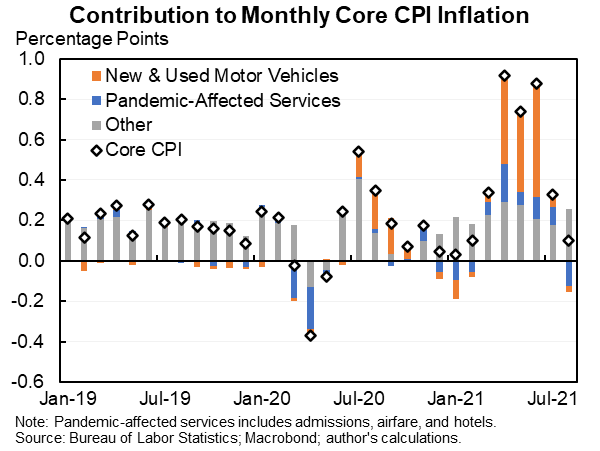

One way you get to employment dominance is thinking that inflation will always be 2% next year. Which means that even if in theory you're supposed to have a dual mandate in practice it collapses down to a unitary employment mandate.

The Fed has more employment dominance now but it is not completely new. In the 1990s it was almost universally thought that the natural rate of unemployment was 6% and many argued it was 7%. Alan Greenspan barely bat an eyelid as it fell to 4%.

I think employment dominance is mostly a good thing and is a big improvement over a mental model that thinks that unemployment can't fall below some poorly measured level or that hyperinflation is around the corner.

Still, like all mostly good things, not every aspect of its current implementation is ideal. For example, I would rather see the Fed admit it places much more weight on employment than inflation than pretend that inflation is about to be 2%.

https://twitter.com/jasonfurman/status/1440743624094806019?s=20

Still, a lot of people make the mistake of thinking the Fed does what it does to help the White House by keeping interest payments/deficits/debt low or to help Wall Street. Anyone who has talked to monetary policy makers, or observed their actions, understands that's not true.

• • •

Missing some Tweet in this thread? You can try to

force a refresh