Jubilant Ingrevia VS Laxmi Organics

Both related to the chemicals (specialty chemicals)

Extensive thread

#fundamentalanalysis #peercomparison #investing

Both related to the chemicals (specialty chemicals)

Extensive thread

#fundamentalanalysis #peercomparison #investing

1)Jubilant Ingrevia (JI) is global integrated life science products and innovative solutions provider owned by the Jubilant group.

Jubilant Ingrevia and Jubilant Pharmova were de-merged in FY21 from the single entity Jubilant Life Sciences.

Jubilant Ingrevia and Jubilant Pharmova were de-merged in FY21 from the single entity Jubilant Life Sciences.

2)Laxmi Organics (LO) is a specialty chemical manufacturer in Acetyl Intermediaries and specialty intermediaries.

3)Business of the company:

JI engages in the production of specialty chemicals, fine chemicals CDMO, Nutrition and Health ingredients specialty ethanol etc.

LO is engaged in the production of Ethyl Acetate, Acetyl intermediaries and other specialty chemicals.

JI engages in the production of specialty chemicals, fine chemicals CDMO, Nutrition and Health ingredients specialty ethanol etc.

LO is engaged in the production of Ethyl Acetate, Acetyl intermediaries and other specialty chemicals.

4)The common thing which connects both the companies is that both these companies are engaged in the production of Acetyl intermediaries majorly ethyl acetate.

5)JI revenue Breakup: 34% from Specialty chemicals, 18% from nutrition and health solutions and 48% from life science chemicals

Lo revenue breakup 50% from Acetyl intermediaries, 32% from specialty chemicals and 9% from other traded goods.

Lo revenue breakup 50% from Acetyl intermediaries, 32% from specialty chemicals and 9% from other traded goods.

6)Demand for Ethyl acetate is increasing because it is less harmful as compared to other chemicals and greener in nature

JI has an annual capacity of 150 tonnes of Ethyl acetate and Laxmi organics has a capacity of 167 tonnes per annum.

JI has an annual capacity of 150 tonnes of Ethyl acetate and Laxmi organics has a capacity of 167 tonnes per annum.

7)Other listed companies which manufacture them are OIL chemicals.

Both these companies have 30-35% markets share in the production of Ethyl acetate.

Both these companies have 30-35% markets share in the production of Ethyl acetate.

8)Another common chemical which both these companies produce is Diketene.

Diketene can be easily procured by forward integrating one step more from the value chain of Ethyl Acetate and Acetic anhydride.

Diketene can be easily procured by forward integrating one step more from the value chain of Ethyl Acetate and Acetic anhydride.

9)Diketene is a colorless liquid and is a building block. It is very difficult to produce and hazardous in nature and difficult to transport. Producing these are a competitive edge to both these companies as Diketene cannot be produced so easily.

10)LO has 55% market share in Diketne and its derivatives, whereas JI is forward integrating itself and launching 6 Diketene derivatives.

11)JI is well diversified and has various products in different segments (48-50% of revenue from Specialty chemicals and Acetyl Intermediaries ) whereas LO specializes in Specialty chemicals and Acetyl Intermediaries only (80-90% revenue)

12)JI in its nutrition segment is globally no. 1 producer in Niacinamide and top 2 in Vitamin B3 (19% market share)

They are the largest manufacturer of Vitamin B4 in India.

They are the largest manufacturer of Vitamin B4 in India.

13)JI's different divisions have been backward integrated which helps them to reduce costs and provides them a competitive advantage

14)Capex Plans:

JI is planning for a capex of 900 CR in the next 2-3 years. They also went through a capex in FY19-20 between 300-600 Cr for Acetyl Dehyde

Out of 900 Cr, 550 Cr: Specialty chemicals, 100 Cr: Nutrition and Health Solutions and 250 Cr: Life science chemicals.

JI is planning for a capex of 900 CR in the next 2-3 years. They also went through a capex in FY19-20 between 300-600 Cr for Acetyl Dehyde

Out of 900 Cr, 550 Cr: Specialty chemicals, 100 Cr: Nutrition and Health Solutions and 250 Cr: Life science chemicals.

15)LO has recently acquired a plant from an Italian player which is into Florine chemicals which has huge margins

and they are planning a capex of 91 Cr into specialty chemicals expanding in Diketene

and they are planning a capex of 91 Cr into specialty chemicals expanding in Diketene

16)Financials:

JI Revenue from FY 17, 2714 Cr to 3653 Cr in FY20,

where EBITDA margin have been very volatile in the past because their products have characteristics of a commodity

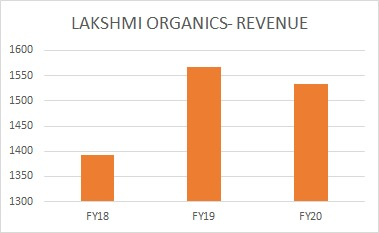

where as, LO's Revenue in FY18 1393 Cr to 1534 Cr in FY 20 having a low EBITDA margin 10-11%.

JI Revenue from FY 17, 2714 Cr to 3653 Cr in FY20,

where EBITDA margin have been very volatile in the past because their products have characteristics of a commodity

where as, LO's Revenue in FY18 1393 Cr to 1534 Cr in FY 20 having a low EBITDA margin 10-11%.

Follow @FinterestC for more!

• • •

Missing some Tweet in this thread? You can try to

force a refresh