$TSLA has blown my Q3 2021 earnings expectations out of the water (more analysis to follow):

tesla-cdn.thron.com/static/TWPKBV_…

tesla-cdn.thron.com/static/TWPKBV_…

"Quarter-end cash & cash equivalents decreased to $16.1B in Q3, driven mainly by net debt and finance lease repayments of $1.5B, partially offset by free cash flow of $1.3B. Our total debt excluding vehicle and energy product financing has fallen to just $2.1B at the end of Q3."

Tesla here is shaming the major credit rating agencies into an upgrade.

As @garyblack00 argued yesterday, it's preposterous for them to consider leaving Tesla rated below investment grade.

As @garyblack00 argued yesterday, it's preposterous for them to consider leaving Tesla rated below investment grade.

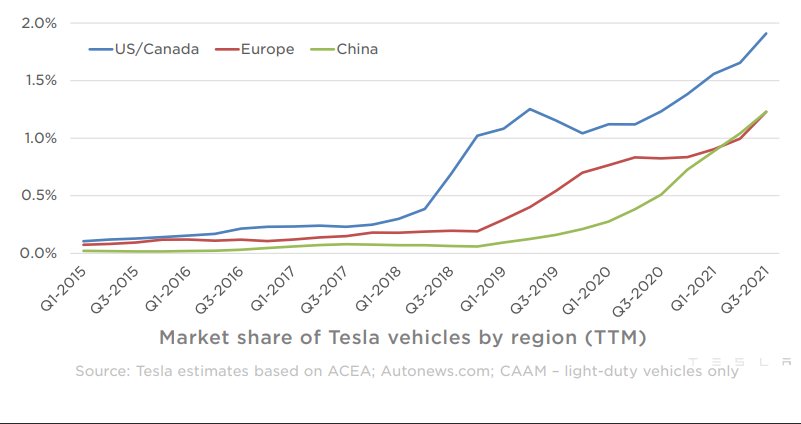

For anyone claiming "Tesla is losing market share all around the world", @MartinViecha has supplied this chart:

$TSLA @elonmusk

$TSLA @elonmusk

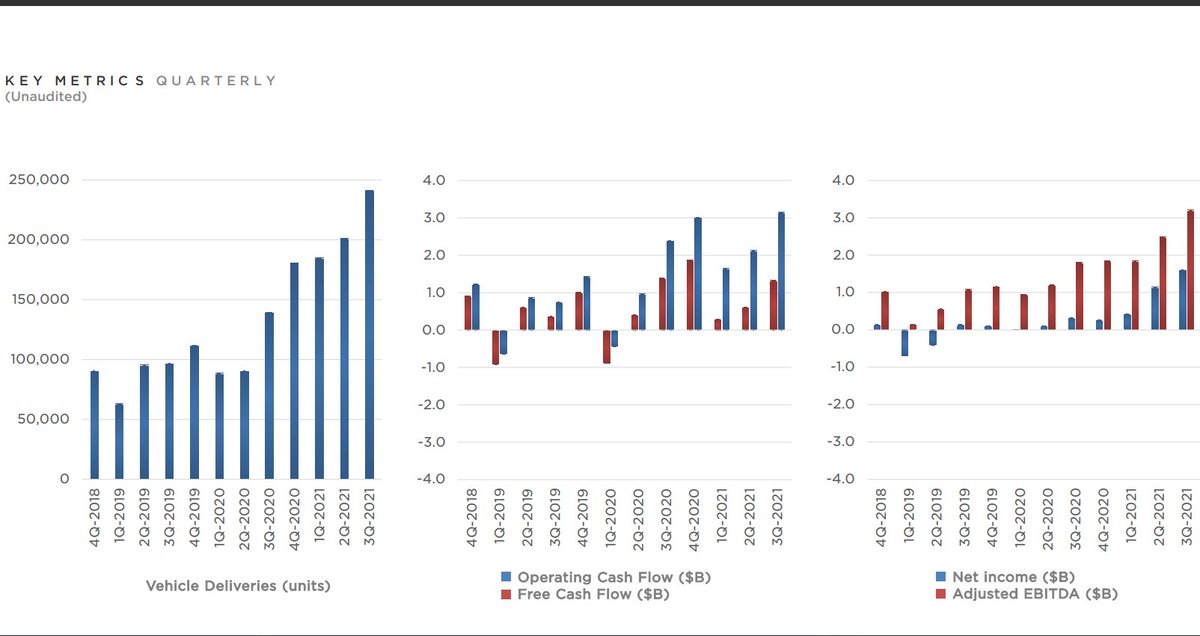

The charts on Page 18 tell the growth story nicely:

The 12-trailing month trends are so clear- especially the Adjusted EBITDA (profit before items unrelated to the current quarter or beyond management control):

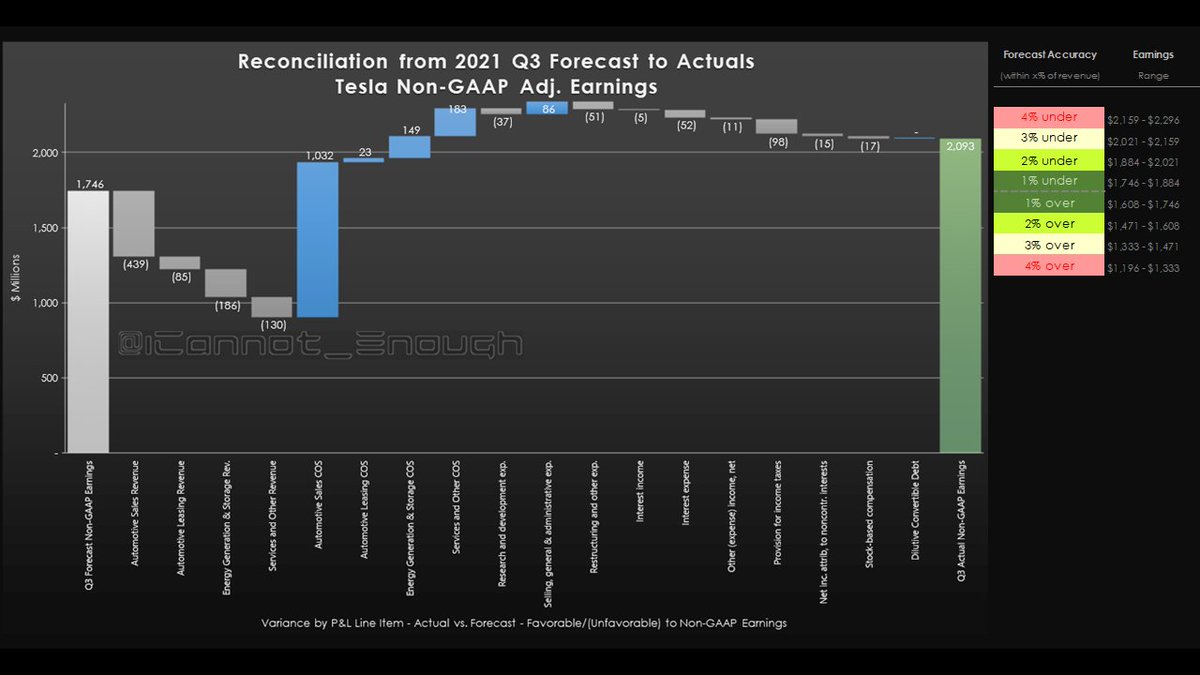

Here are my forecast variances by Income Statement line item.

My earnings forecast was low by about 2.5% of Actual revenue.

The largest variance was Automotive COS, which came in *extremely favorable* to my expectation. Look for me to adjust that favorably in my next forecast.

My earnings forecast was low by about 2.5% of Actual revenue.

The largest variance was Automotive COS, which came in *extremely favorable* to my expectation. Look for me to adjust that favorably in my next forecast.

$TSLA GAAP EPS (diluted), last 11 quarters:

(numbers in parentheses indicate a loss)

2019 Q1 ($0.78)

2019 Q2 ($0.44)

2019 Q3 $0.15

2019 Q4 $0.11

2020 Q1 $0.02

2020 Q2 $0.10

2020 Q3 $0.27

2020 Q4 $0.24

2021 Q1 $0.39

2021 Q2 $1.02

2021 Q3 $1.44

E A R N I N G S G R O W T H

(numbers in parentheses indicate a loss)

2019 Q1 ($0.78)

2019 Q2 ($0.44)

2019 Q3 $0.15

2019 Q4 $0.11

2020 Q1 $0.02

2020 Q2 $0.10

2020 Q3 $0.27

2020 Q4 $0.24

2021 Q1 $0.39

2021 Q2 $1.02

2021 Q3 $1.44

E A R N I N G S G R O W T H

• • •

Missing some Tweet in this thread? You can try to

force a refresh