Air Passenger Duty changes will INCREASE FLYING….

OBR forecasts ~400k more flights per year.

But NOT UK EMISSIONS. Here’s why (reason is not obvious):

1/N

(from @StuartAdam_IFS

@TheIFS

presentation)

OBR forecasts ~400k more flights per year.

But NOT UK EMISSIONS. Here’s why (reason is not obvious):

1/N

(from @StuartAdam_IFS

@TheIFS

presentation)

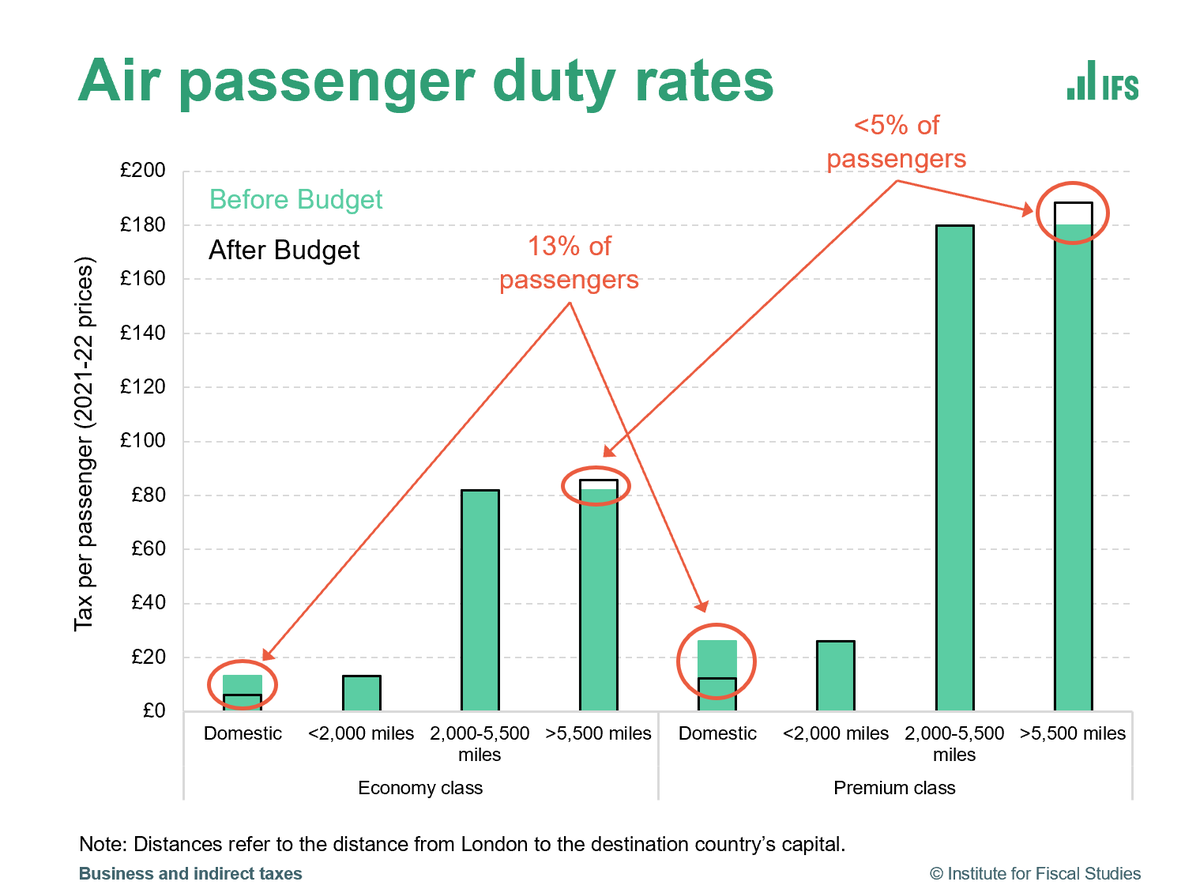

Domestic flights are within UK Emissions Trading Scheme. This puts a cap on emissions from things covered. BROADLY, more emissions from domestic aviation -> more demand for permits -> higher ETS prices -> lower emissions elsewhere. Overall emissions within ETS unchanged. 2/n

At same time, higher APD on long haul will cut emissions.

(worth remembering that, thanks to VAT, business flights still subsidised. We showed that here: ifs.org.uk/publications/1…)

3/n

(worth remembering that, thanks to VAT, business flights still subsidised. We showed that here: ifs.org.uk/publications/1…)

3/n

Punchline: Another example of why it’s important to look at all policies together and not just on the direct effects of one.

End.

End.

• • •

Missing some Tweet in this thread? You can try to

force a refresh