Inflation is much on the minds of investors and rightly so. So let’s take a look at sector performance during inflation waves in the past. It may surprise you. (THREAD)

In addition to the inflation regimes of the 1940s and 1970s, there were two smaller waves over the past few decades, as measured by swings in the 5-year inflation CAGR. The first was 1987-92 and the second was 2003-08. The chart above shows these four regimes. /2

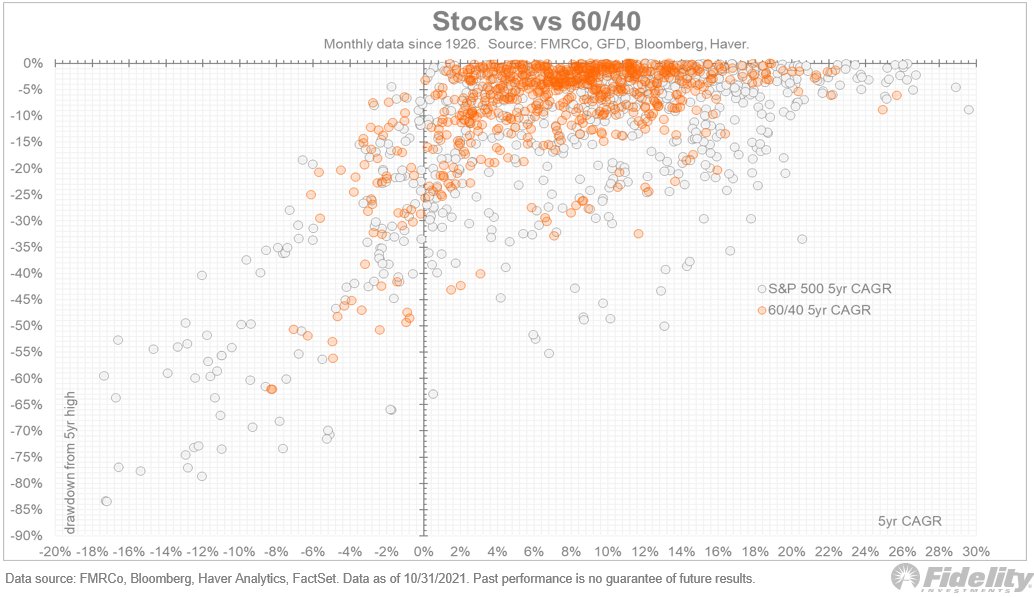

The next chart shows the S&P 500 real return during those regimes. The long-term CAGR for the inflation-adjusted S&P 500 is 6.82% (since 1926). Stocks have done OK during inflation regimes (the '70s being the exception), at least compared to its long-term trend. /3

We know that equity valuations are inversely correlated to inflation, but that doesn’t necessarily translate to negative or below-average returns. It all depends on the starting point and what happens on the “E” side of the P/E ratio. /4

My guess is that most people would just assume that inflation regimes are uniformly bad for equity returns, using the 1970s as the obvious example. But the data show otherwise. /5

And by the way, did you notice that these structural inflation waves tend to occur in cycles of around 10-15 years? 1942-50, 1965-80, 1987-92, 2003-08, 2020-?. On that basis alone, we seem to be due for another wave. /6

So which sectors win and lose during inflation waves? The next chart shows the correlation of monthly relative returns against the monthly inflation rate for the 11 GIC sectors. /7

The message is fairly consistent: energy sector relative returns have been positively correlated to inflation every single time, while consumer discretionary and financials have been negatively correlated every single time. /8

The relative performance data are a bit less consistent, however, as this next chart shows. Energy is still the most consistent relative winner, but consumer and financial stocks are a bit more mixed. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh