Why should any investor own bonds at this point, given that they barely produce any nominal income, and are likely to lose value in real terms? Take a look at this chart, and we'll explore the question a bit more. (THREAD)

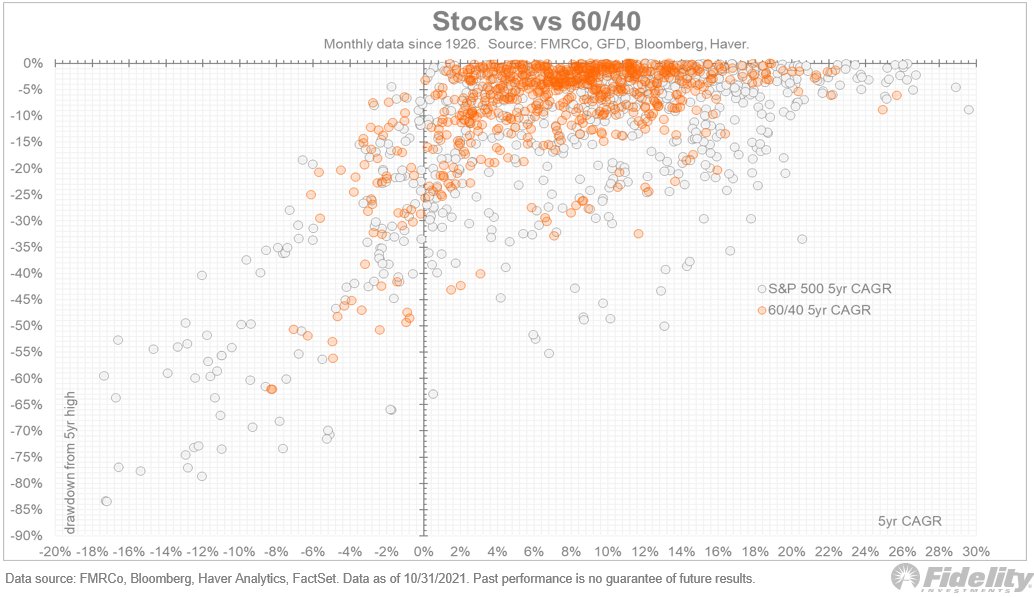

In recent years, the reason to go with a 60/40 portfolio was to diversify and protect. We can see this in the chart above. /2

60/40 produced about 2 percentage points less return per year than the S&P 500, but still a very respectable 9% – well above the inflation rate. It also helped investors sleep at night when the stock market was down (which it was about 40% of the time). /3

Today, portfolio diversification is the only reason to own Treasuries for the long-term. In my view, the 60 side of the 60/40 model remains the anchor for any long-term investment portfolio. The power of compounding is simply beyond dispute. /4

Maybe we can tinker around the edges, under-weighting the sectors that are negative correlated to inflation and over-weighting the winners. But that’s about it. I see little cause to mess with the 60 side. /5

As for the 40 side, bonds are on a short leash, but I am not quite ready to give up yet. We don’t know what the future will look like, and it’s entirely possible that the stocks/bonds correlation will remain negative, as it has been for the past two decades. /6

Financial repression does strange things to the rates market, as shown both in the US during the 1940s and Japan more recently. In Japan, long-term JGBs yield nothing, yet continue to be negatively correlated to Japanese stocks. /7

But I do think it makes sense to consider being more creative in what we put in that 40 bucket. Commodities, high-yield bonds, TIPS, floaters, real estate, gold and silver, and, yes, Bitcoin, all could be viable alternatives or complements to the 40. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh