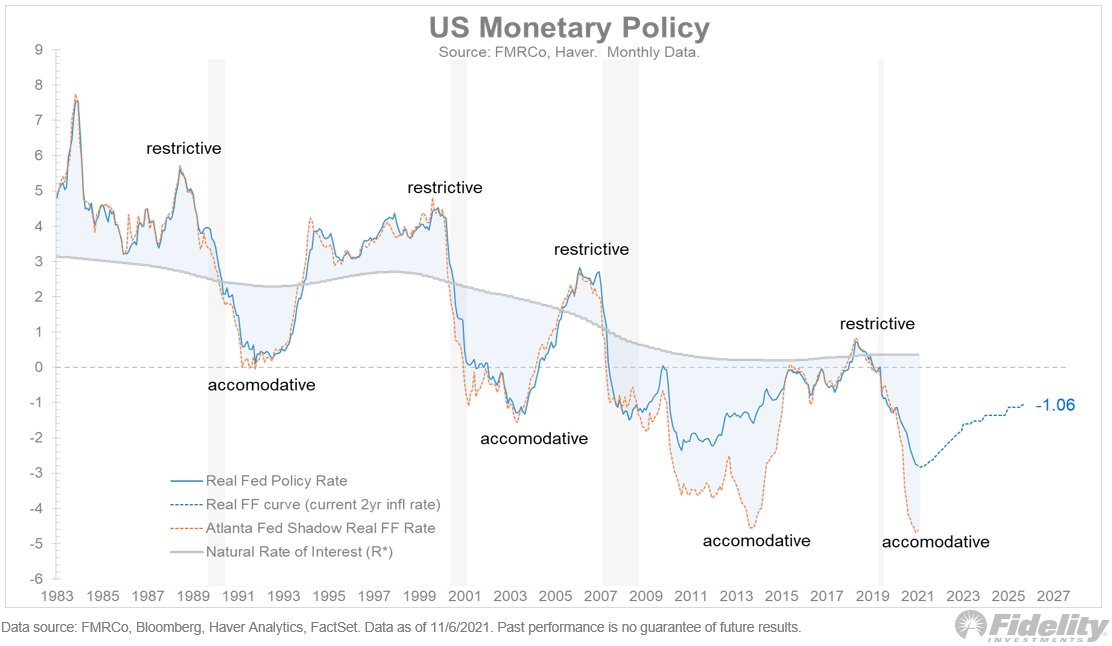

In some ways, the current Fed cycle reminds me of 2015-18. Take a look at this chart and I'll explain. (THREAD)

Back in late 2015, the Fed finally hiked rates for the first time. Back then there was a massive policy divergence between the US (which was normalizing) and the rest of the world (mainly Europe and China, which were spiraling down). /2

Just a few weeks after achieving lift-off, energy spreads blew out and the dollar soared, causing financial conditions to seize up. The Fed backed off, and this enabled the economy to ease back into mid-cycle. It was the great cycle extender. /3

Today, we have another late-cycle signal, but it is coming mostly from the labor market, and not from a tightening of financial conditions. /4

Given that the Fed is not expected to start raising rates until the second half of 2022 (and not even approach the neutral rate until 2025), perhaps the Fed’s current gradual pace will have the same cycle-extending effects. /5

One big difference between now and then: Inflation is running much hotter now. That’s a wild card that the Fed has not had to contend with for several decades. /6

In my view, the Fed is hoping/expecting that the CPI will have cooled down by next summer (when the taper ends and rate hikes begin). If not, it will have no choice but to accept structurally higher inflation. /END

• • •

Missing some Tweet in this thread? You can try to

force a refresh