Always fascinated by how rapidly Enron unraveled. From $100 billion in reported revenue in 2000 to bankruptcy by December 2001.

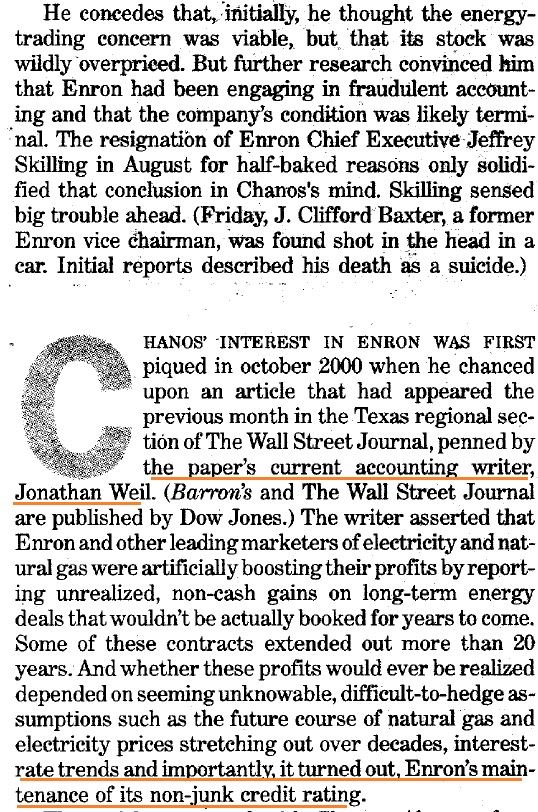

Jonathan Weil’s 2000 Wall Street Journal article that kicked it all off: “Energy Traders Cite Gains, But Some Math Is Missing”

That made @WallStCynic sharpen his pencil.

"Easiest short we ever had."

"It skyrocketed then rolled over and pretty much went straight down."

"It skyrocketed then rolled over and pretty much went straight down."

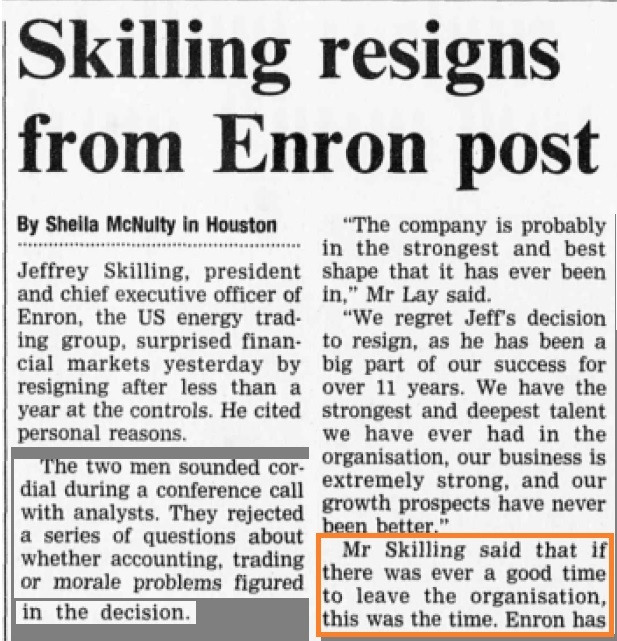

"It wasn't until after Skilling left in August of 2001 where I began to really get suspicious."

Bethany McLean’s March 2001 article in Fortune: “Is Enron Overpriced?”

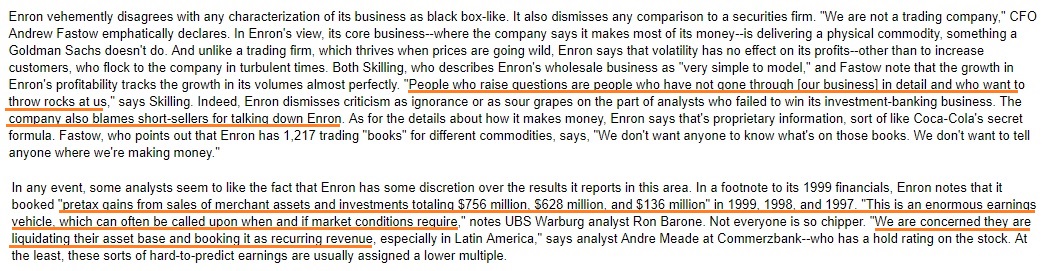

“Start with a pretty straightforward question: How exactly does Enron make its money?

‘If you figure it out, let me know,’ laughs credit analyst Todd Shipman at S&P.'”

archive.fortune.com/magazines/fort…

“Start with a pretty straightforward question: How exactly does Enron make its money?

‘If you figure it out, let me know,’ laughs credit analyst Todd Shipman at S&P.'”

archive.fortune.com/magazines/fort…

"Insiders selling hundreds of millions."

"The more I looked the more things didn't make sense."

"The more I looked the more things didn't make sense."

Financial Times August 2001: narrative is about the broadband business; transparency is becoming an issue.

Skilling resigns two weeks later with a great Freudian slip: if there was ever a good time to leave the organization, this was it.

“4,000 off-balance sheet partnerships"

"They seemed to be selling parts of themselves to themselves”

"They seemed to be selling parts of themselves to themselves”

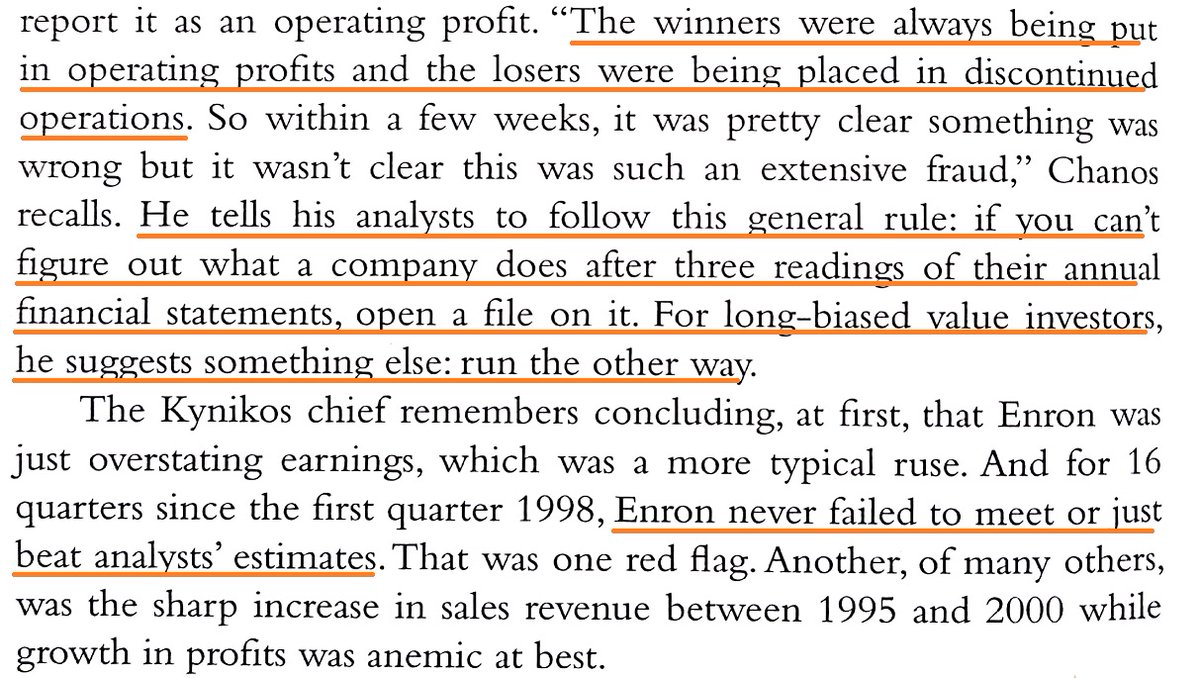

“If you can’t figure out what a company does after three readings of their financial statements, open a file”

If you're a long-biased investor: "run the other way"

If you're a long-biased investor: "run the other way"

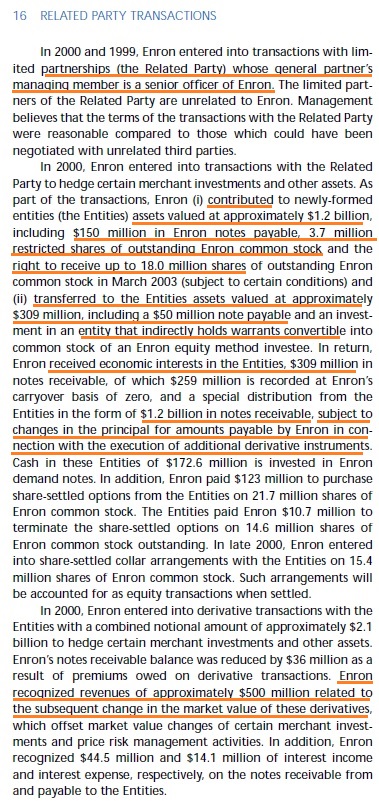

Related party transactions

Things moved so quickly.

Price leads narrative.

Remember your values.

• • •

Missing some Tweet in this thread? You can try to

force a refresh