November CPI inflation was predictably ugly, perhaps a bit less ugly than feared. Inflation over the past year has accelerated across most everything, but the biggest culprits have been surging cost of gasoline, home heating and vehicles.

But November will be the peak in inflation. Gasoline and home heating costs have fallen sharply in recent weeks, and with supply chains settling, vehicle production is off bottom, and prices should roll over early next year.

At root, the higher inflation is due to the supply-side disruptions caused by the pandemic, especially the Delta wave of the pandemic. As the pandemic recedes – each wave is less disruptive than the previous one – inflation will moderate.

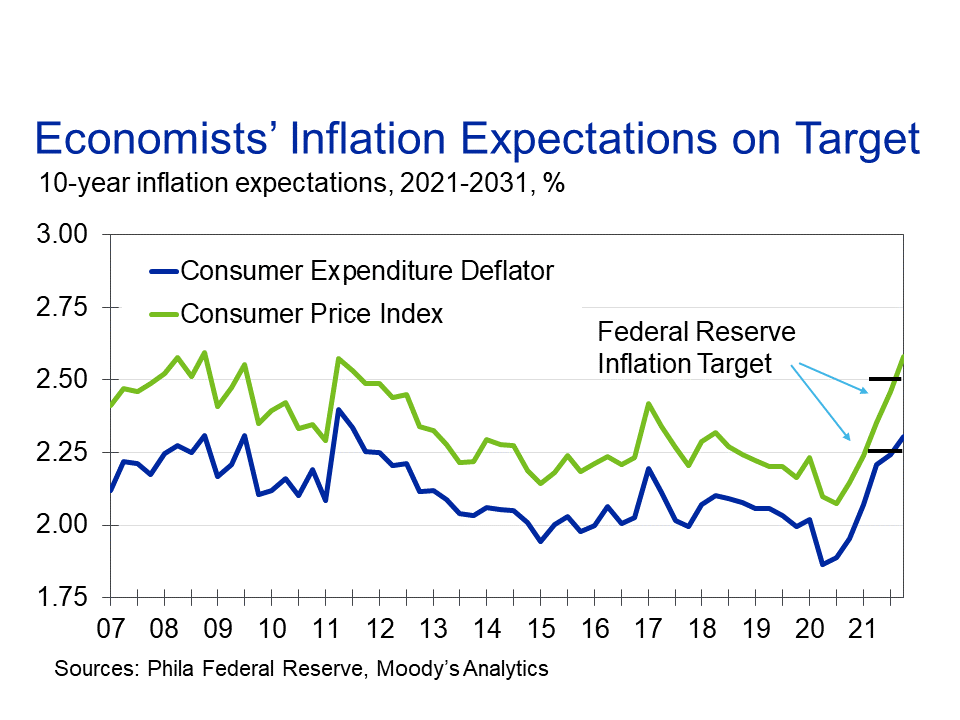

Inflation by this time next year will be within spitting distance of the Federal Reserve’s inflation target.

• • •

Missing some Tweet in this thread? You can try to

force a refresh