New NYT piece out today comparing inflation trends across countries: A key observation is that we in the US got somewhat more heat, but also more growth, jobs resulting in a significantly faster recovery.

nytimes.com/2022/01/22/bus…

nytimes.com/2022/01/22/bus…

Also, inflation up strongly in most countries suggests common pressure: COVID/supply chain snarls.

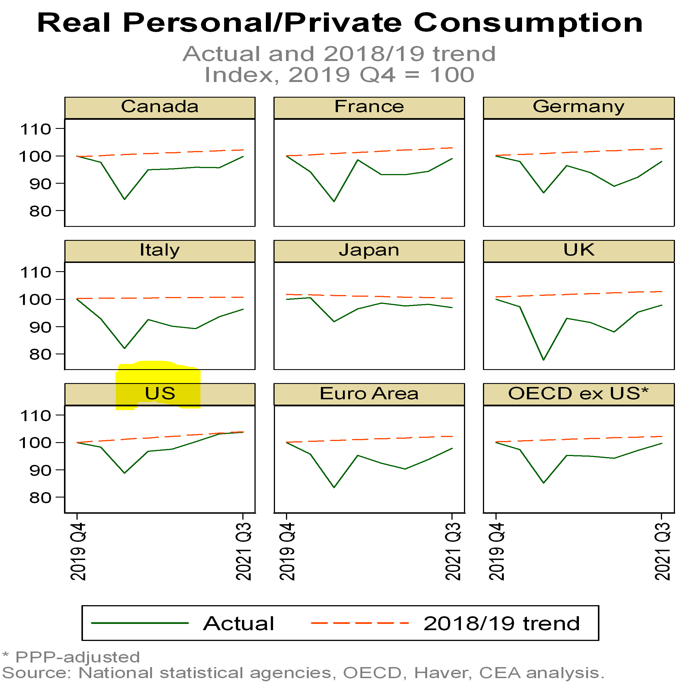

Here’s real GDP and real consumer spending indexed to 2019q4 (cool new figure alert!). As you see, we’re above the pack. Our income supports—go ARP!—have been particularly important in supporting consumer spending (70% of US GDP). We’re the only country back on trend!

That strong US recovery has created price heat. But as NYT noted, a lot of that is the unique US auto situation. Check out this figure on core CPI but without autos.

Why omit cars? Not at all to diminish the challenge these prices engender on families buying new or used vehicle (and @jasonfurman makes fair point). But because auto's price spike clearly function of global chip shortage.

Next, true that euro area has seen less heat than the U.S. over last 2 yrs. But shorter time horizons also instructive, both in understanding the impact of 2021 ARP & in understanding latest trends. Headline inflation similar in the U.S. and Europe, 2nd half this yr.

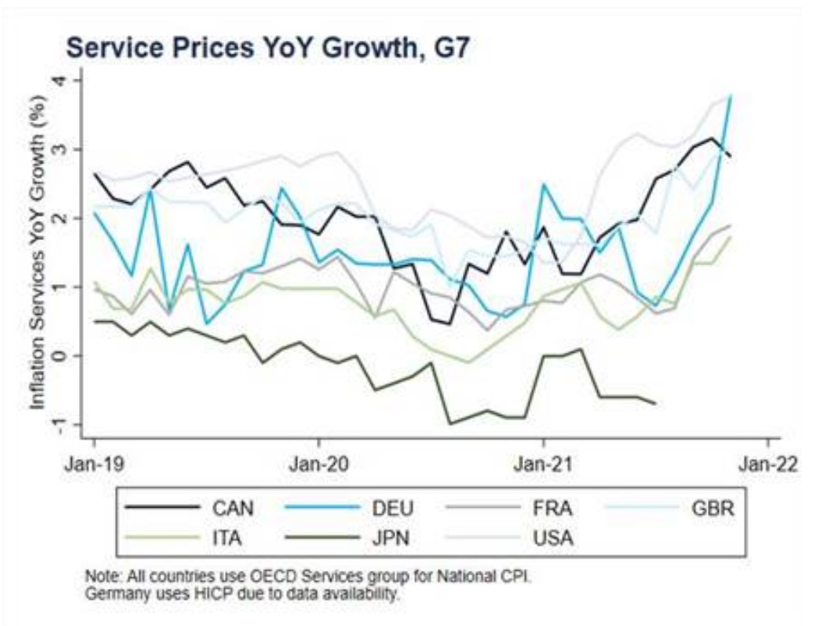

Next, services, unlike cars, are more insulated from global forces, and their price growth is similar across countries. Since policy was different in each country, this too highlights that other factors are important drivers of price pressures.

Bottom line, along w uniquely strong US demand, pandemic-induced supply snarls are juicing price growth in most advanced countries, few of which have seen a recovery as strong as ours. By some measures, US price growth is faster, but we got stronger growth for that extra heat!

• • •

Missing some Tweet in this thread? You can try to

force a refresh