$TTD @TheTradeDesk

🧵

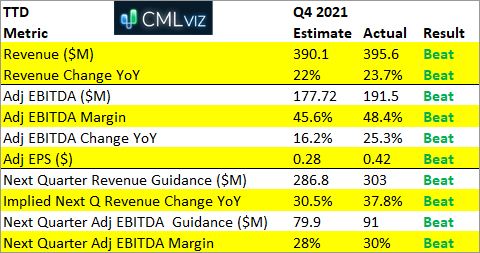

The company beat on every metric we follow from Q4 revenue, revenue growth, and profitability metrics and margins to next quarter's guidance for the same.

/1

🧵

The company beat on every metric we follow from Q4 revenue, revenue growth, and profitability metrics and margins to next quarter's guidance for the same.

/1

There are three questions for all companies facing these comps:

1. Can companies beat the estimates for the quarter, even if the grow itself will look less than before?

/2

1. Can companies beat the estimates for the quarter, even if the grow itself will look less than before?

/2

2. Will guidance out of the quarter exceed estimates, implying that the COVID year wasn’t just a “pull forward,” but rather simply a new, higher base on which to continue growth?

/3

/3

3. Can profitability improve in Q4 2021, even as growth slows for the comparable period a year before?

The answers to these questions for TTD are yes, yes, and yes.

Let's see them...

/4

The answers to these questions for TTD are yes, yes, and yes.

Let's see them...

/4

• $TTD delivered 24% growth for Q4 2021 compared to Q4 2020 versus estimates of 22%.

• $TTD guided to 38% growth for Q1 2022 compared to Q1 2021 versus estimates of 30.5%. This is a substantial beat.

/5

• $TTD guided to 38% growth for Q1 2022 compared to Q1 2021 versus estimates of 30.5%. This is a substantial beat.

/5

• $TTD delivered a 25% rise in adjusted EBITDA compared to Q1 2021, outpacing revenue growth (23%) versus estimates of 16% growth. Further, TTD delivered a mind blowing 48.4% EBITDA margin versus estimates of 45.6%.

/6

/6

Everything is working for $TTD, and any selling pressure in the near-term off of these results is due not to financial performance, but simply a reflection of an elevated valuation.

/7

/7

As for $GOOGL impact on $TTD and OpenPath:

"A very small per cent of our business runs through Google’s Ad Exchange, we are not dependent on Google for our business. The market will always ultimately gravitate to transparency and competition over time."

/8

"A very small per cent of our business runs through Google’s Ad Exchange, we are not dependent on Google for our business. The market will always ultimately gravitate to transparency and competition over time."

/8

An investment in @TheTradeDesk is simply and investment in the non-walled garden advertising world; the "rest of the Internet."

Either that’s your cup of tea or it isn’t.

/9

Either that’s your cup of tea or it isn’t.

/9

$TTD $ROKU

Finally, we got feedback from the current Senior Director, Global Head of Platform at Roku who was a former Regional VP, Business Development – West at The Trade Desk.

That and our next CFO one-on-one, is for members.

Get CML Pro

bit.ly/CMLPro

10/10

Finally, we got feedback from the current Senior Director, Global Head of Platform at Roku who was a former Regional VP, Business Development – West at The Trade Desk.

That and our next CFO one-on-one, is for members.

Get CML Pro

bit.ly/CMLPro

10/10

• • •

Missing some Tweet in this thread? You can try to

force a refresh