Why 🎵 music labels is unique business model ?

@NeilBahal

Watch the video !

Link :

1. High Entry Barriers

It's not easy to create catalogue of 1 Lk songs in short time. Each movie will have 4-5 songs and in a year about 100 movies might be released,

@NeilBahal

Watch the video !

Link :

1. High Entry Barriers

It's not easy to create catalogue of 1 Lk songs in short time. Each movie will have 4-5 songs and in a year about 100 movies might be released,

so about 500 songs will be produced in a year. To create catalogue of 25000 songs it will need 50 years. Industry will keep consolidating, as bigger players will acquire the smaller music labels.

2. Get the acquisition costs recovered in 3-5 years and keep the content with you for lifetime without any incremental costs.

Keyword : Without incremental costs

Keyword : Without incremental costs

3. Value migration from ad-based music to paid music

Ad-based music listeners are about 7x of paid premium music listeners while revenues from them are 22x more compared to ad-based revenues. This is the data of international market. In India opportunity size much higher !

Ad-based music listeners are about 7x of paid premium music listeners while revenues from them are 22x more compared to ad-based revenues. This is the data of international market. In India opportunity size much higher !

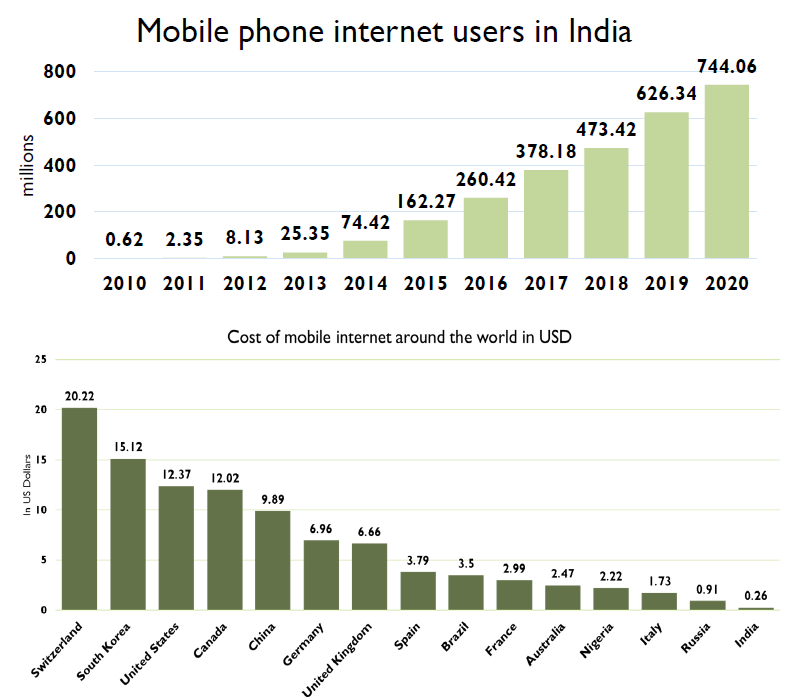

4. Mobile phone users in India & Cost of 1 GB Data in world in $

6. Porter 5 forces - Best Industry Structure

7. ROCE of core music business

• • •

Missing some Tweet in this thread? You can try to

force a refresh