0/ This time last week we were finally seeing some upside volatility in crypto and specifically #BTC. Now it seems as if all of that momentum may have switched over to #Gold ?

Let’s take a deeper look under the hood of crypto markets 🧵👇

Let’s take a deeper look under the hood of crypto markets 🧵👇

1/ After touching 45500 resistance again BTC has quickly faded back in line with risk assets that remain heavy as Ukraine conflict intensifies. Key level to hold is now 36500, a break of which open door towards 29k.

2/ Spike in BTC-RUB volumes showed that some citizens are seeing the benefits of digital assets in times of crisis, a more medium bullish dynamic. Ukraine also managed to raise 10s of millions in donations and BTC being used as a medium of exchange on the ground.

3/ My takeaway from @glassnode this week was that there is still more pain to be taken before we can say a major bottom is in. That pain will likely be taken in a re-test of 29/30k should it happen. I'm keeping dry powder.

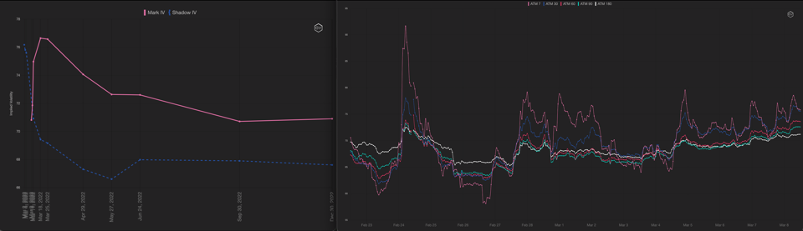

4/ Realised vol drifted back a bit last week to be more in line with implieds as markets sold off in an orderly fashion (more so than stocks). Implied still at a slight discount which is unusual when so much macro risk is out there.

5/ Term structure remained inverted all week as gamma paid and buyers came in for mid/late March expiries to capture FOMC. Weeklies still saw DOV selling flows but less impact than normal as vol is good value here.

6/ Main block flows were 18Mar 34000/42000 strangle buyer, Jun22 45000/60000 call spread buyer and ETH 18Mar 2200 put buyer that helped give ST put skew a bid.

7/ NFT volumes down 72% from peak, explains why no love for ETH and why the ETH/BTC spread is languishing near bottom of range.

https://twitter.com/Delphi_Digital/status/1500997280526127108?s=20&t=-U-VX5THBmosjJ0q49wL1g

8/ As Gold breaks higher, BTC trades heavy. The negative correlation is back last few days, suggests switching happening.

9/ Try out our community by joining our FREE Discord group chat (discord.gg/Dee5gFay) to join the conversation and get info like this & more in real-time.

• • •

Missing some Tweet in this thread? You can try to

force a refresh