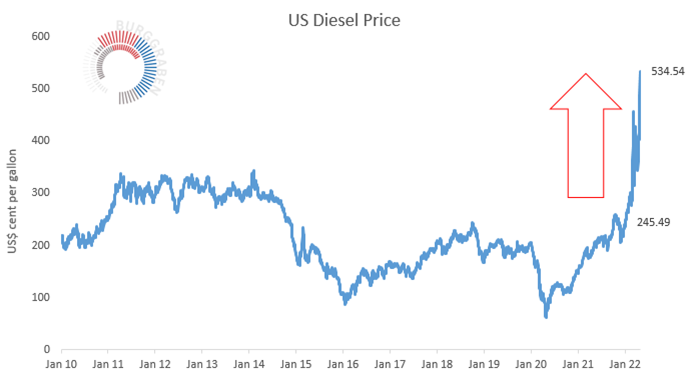

Can the European Union ban Russian gas imports?

Answer: Faster than you might expect, but it comes down to great leadership & setting the right priorities!

Let's go - Part 3 (total of 13 tweets) with a focus on the UK.

1/n 🧵

#UkraineRussiaWar #EuropeanUnion

Answer: Faster than you might expect, but it comes down to great leadership & setting the right priorities!

Let's go - Part 3 (total of 13 tweets) with a focus on the UK.

1/n 🧵

#UkraineRussiaWar #EuropeanUnion

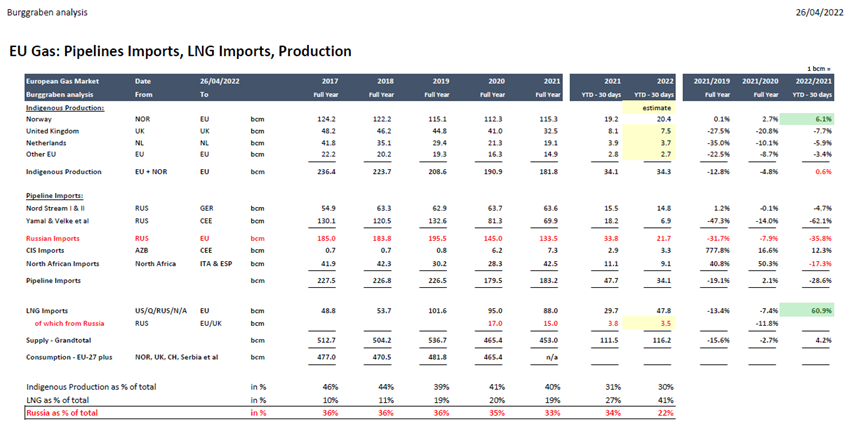

In part 1 we explained EU LNG and the importance of its optimial use.

2/n

2/n

https://twitter.com/BurggrabenH/status/1519135040868962305?s=20&t=uQTCMhhHdzPlcq5f-BFr9w

In part 2 we explained the potential of more local production & illustrated the need for policy corrections such as building German LNG regasification terminals.

3/n

3/n

https://twitter.com/BurggrabenH/status/1519174995741712385?s=20&t=uQTCMhhHdzPlcq5f-BFr9w

It seems Minister Habeck studied our thread.

Today, he annouced the start of the construction of 2 regasification terminals for a total capacity of 10bcm, completed within 10 months - a most remarkable outcome if achieved by @BMWK.

4/n

Today, he annouced the start of the construction of 2 regasification terminals for a total capacity of 10bcm, completed within 10 months - a most remarkable outcome if achieved by @BMWK.

4/n

https://twitter.com/BurggrabenH/status/1522220280697036800?s=20&t=uQTCMhhHdzPlcq5f-BFr9w

Many imbalances remain for the gas to go where it is needed within the EU pipe system.

This is best illustrated with the current divergence of TTF (Netherland Price Hub) versus NBP (UK Price).

At the time of this writing the 2 prices had a $11/MMBtu ($66/boe) difference!

5/n

This is best illustrated with the current divergence of TTF (Netherland Price Hub) versus NBP (UK Price).

At the time of this writing the 2 prices had a $11/MMBtu ($66/boe) difference!

5/n

Looking at the Futures curve of both, the price divergence seems to point towards a "temporary indigestion" of logistical issues as prices converge again in July.

But for some weeks NBP signals that it cannot take on more LNG while gas cannot be exported into EU storages.

6/n

But for some weeks NBP signals that it cannot take on more LNG while gas cannot be exported into EU storages.

6/n

So why can gas not be delivered into the EU?

To explain that, let us first attach the relevant pipeline map of the UK and its interconnectors with the continent and Norwegian gas fields.

Today, mainly the "Interconnector" from Bacton to Zeebrugge in Belgium matters.

7/n

To explain that, let us first attach the relevant pipeline map of the UK and its interconnectors with the continent and Norwegian gas fields.

Today, mainly the "Interconnector" from Bacton to Zeebrugge in Belgium matters.

7/n

Let's now check UK gas flow balances.

In April the UK exported 2bcm (great) to Zeebrugge but in reality had export capacity for 3.6bcm.

It imported 3.6bcm LNG, 2bcm from Norway & produced 3.2bcm against 4.7bcm demand.

8/n Thx Alex, amazing info for free!

In April the UK exported 2bcm (great) to Zeebrugge but in reality had export capacity for 3.6bcm.

It imported 3.6bcm LNG, 2bcm from Norway & produced 3.2bcm against 4.7bcm demand.

8/n Thx Alex, amazing info for free!

So what is the problem?

The problem is that EU logistics (Belgium, Netherlands or Germany) likely couldn't take in enough gas b/c of some "filter problem".

That led to a temp backlog throughout the system while the UK barely has any storage capacity left!

9/n

The problem is that EU logistics (Belgium, Netherlands or Germany) likely couldn't take in enough gas b/c of some "filter problem".

That led to a temp backlog throughout the system while the UK barely has any storage capacity left!

9/n

In fact, much gas the UK needs in the winter is stored in Germany's massive salt cavities and according to Wood MacKenzie, a consultant.

Most remarkable!

10/n

Most remarkable!

10/n

Russian gas independence aside, the UK is a major gas consumer. Saving on gas storage (yes, it is bad business) is penny wise, pound foolish!

Take March 1st 2018 when the beast of the east (a cold wind) caused NBP to spike to 350p/th as more demand could not be delivered.

11/n

Take March 1st 2018 when the beast of the east (a cold wind) caused NBP to spike to 350p/th as more demand could not be delivered.

11/n

There are storage projects.

But they need to be FID'd or - perhaps - Government sponsored if they cannot meet return requirements the industry needs to justify the upfront investment.

12/n @BorisJohnson

But they need to be FID'd or - perhaps - Government sponsored if they cannot meet return requirements the industry needs to justify the upfront investment.

12/n @BorisJohnson

More UK storage will avoid winter price spikes for British consumers (especially once the EU gas crisis is over) and will allow for an even higher capacity utilisation of its local LNG infrastructure. Straightforward!

#UkraineRussiaWar

13/n End of thread. Thx!

#UkraineRussiaWar

13/n End of thread. Thx!

• • •

Missing some Tweet in this thread? You can try to

force a refresh